Home > Comparison > Consumer Defensive > CL vs NUS

The competitive dynamic between Colgate-Palmolive Company and Nu Skin Enterprises shapes the Consumer Defensive sector’s evolution. Colgate-Palmolive operates as a diversified household and personal products giant with broad global reach. Nu Skin focuses on innovative beauty and wellness solutions with a direct sales model. This analysis explores their contrasting strategies to identify which business model offers superior risk-adjusted returns for a balanced investment portfolio.

Table of contents

Companies Overview

Colgate-Palmolive and Nu Skin Enterprises hold prominent roles in the global personal care market.

Colgate-Palmolive Company: Global Consumer Products Leader

Colgate-Palmolive dominates the household and personal care sector with a diverse product portfolio. It generates revenue primarily through oral, personal, and home care products and pet nutrition. Its 2026 strategy emphasizes broad market reach across traditional retailers and eCommerce, leveraging strong brands like Colgate and Hill’s Science Diet.

Nu Skin Enterprises, Inc.: Innovative Beauty and Wellness Provider

Nu Skin Enterprises focuses on beauty and wellness products, selling skin care systems and nutritional supplements. It drives revenue via direct sales, distributors, and online channels. In 2026, Nu Skin prioritizes product innovation and global retail expansion, particularly in Mainland China, under brands like ageLOC and Pharmanex.

Strategic Collision: Similarities & Divergences

Both companies operate in personal care but differ fundamentally: Colgate-Palmolive follows a broad, multi-brand distribution model, while Nu Skin pursues a direct-to-consumer, innovation-led approach. They compete primarily in skin and personal care markets. Their distinct business models create divergent investment profiles—Colgate offers stability and scale, Nu Skin targets growth through niche innovation.

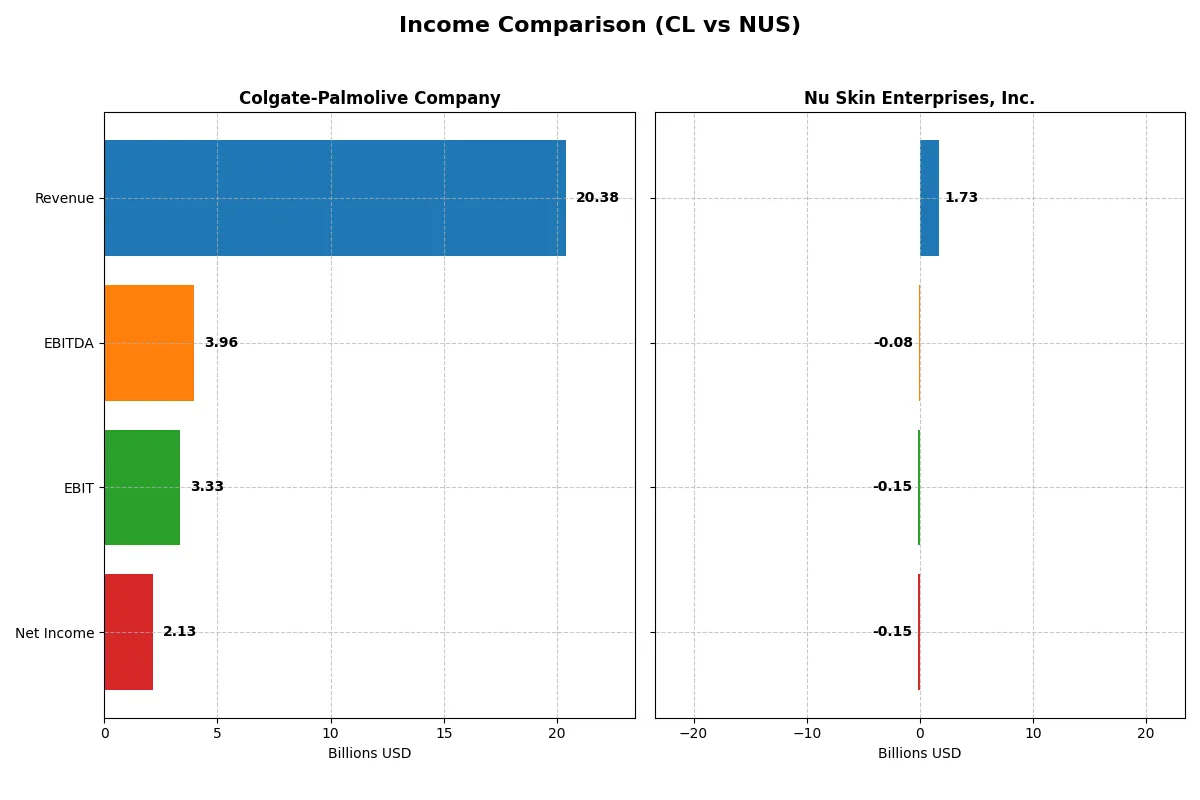

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Colgate-Palmolive Company (CL) | Nu Skin Enterprises, Inc. (NUS) |

|---|---|---|

| Revenue | 20.4B | 1.7B |

| Cost of Revenue | 8.1B | 550M |

| Operating Expenses | 7.9B | 1.3B |

| Gross Profit | 12.3B | 1.2B |

| EBITDA | 4.0B | -79M |

| EBIT | 3.3B | -149M |

| Interest Expense | 267M | 26M |

| Net Income | 2.1B | -147M |

| EPS | 2.64 | -2.95 |

| Fiscal Year | 2025 | 2024 |

Income Statement Analysis: The Bottom-Line Duel

The income statement comparison reveals which company runs a more efficient and profitable corporate engine over recent years.

Colgate-Palmolive Company Analysis

Colgate shows steady revenue growth, reaching $20.4B in 2025, but net income slid to $2.13B, down 25% from 2024. Gross margin remains robust at 60%, supporting a solid 10.5% net margin, though profitability momentum weakened last year with a 21.7% EBIT decline. Operating efficiency faces headwinds despite a strong margin base.

Nu Skin Enterprises, Inc. Analysis

Nu Skin’s revenue dropped 12% to $1.73B in 2024, accompanied by a steep net loss of $147M, reversing a modest profit in 2023. While gross margin is impressive at 68%, the company struggles with negative EBIT and net margins near -8.5%. The sharp profitability deterioration signals operational challenges and margin pressure.

Stable Margins vs. Deepening Losses

Colgate’s income statement reflects resilient margin control despite recent profit erosion, whereas Nu Skin’s figures reveal deepening losses amid declining sales. Colgate remains the fundamental winner with positive net income and strong margins. Investors seeking stability should favor Colgate’s proven profitability over Nu Skin’s ongoing turnaround risks.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | Colgate-Palmolive Company (CL) | Nu Skin Enterprises, Inc. (NUS) |

|---|---|---|

| ROE | 13.63% | -22.50% |

| ROIC | 30.56% | -10.40% |

| P/E | 25.73 | -2.33 |

| P/B | 350.65 | 0.53 |

| Current Ratio | 0.92 | 1.82 |

| Quick Ratio | 0.58 | 1.17 |

| D/E (Debt to Equity) | 40.15 | 0.73 |

| Debt-to-Assets | 53.05% | 32.56% |

| Interest Coverage | 15.01 | -5.74 |

| Asset Turnover | 1.25 | 1.18 |

| Fixed Asset Turnover | 4.55 | 3.71 |

| Payout Ratio | 61.92% | -8.14% |

| Dividend Yield | 2.41% | 3.49% |

| Fiscal Year | 2024 | 2024 |

Efficiency & Valuation Duel: The Vital Signs

Ratios act as a company’s financial DNA, uncovering hidden risks and revealing operational excellence vital for investment decisions.

Colgate-Palmolive Company

Colgate shows strong profitability with a 13.63% ROE and solid 14.37% net margin, signaling efficient core operations. Its P/E ratio of 25.73 appears stretched compared to sector averages. The 2.41% dividend yield offers steady shareholder returns, complemented by prudent reinvestment in R&D at 1.77% of revenue.

Nu Skin Enterprises, Inc.

Nu Skin reports negative profitability metrics, including a -22.5% ROE and -8.46% net margin, highlighting operational challenges. However, its valuation is attractive with a low P/B of 0.53 and a favorable dividend yield of 3.49%. The company balances shareholder returns with ongoing reinvestment, though profitability remains a concern.

Valuation Stretch vs. Profitability Concern

Colgate offers robust profitability but trades at a premium with stretched valuation metrics. Nu Skin presents a cheaper valuation and higher dividend yield but suffers from weak profitability. Investors seeking operational strength may prefer Colgate, while those focused on valuation bargains might consider Nu Skin’s riskier profile.

Which one offers the Superior Shareholder Reward?

I compare Colgate-Palmolive (CL) and Nu Skin Enterprises (NUS) on shareholder distributions. CL yields ~2.4% with a 62% payout, supported by strong FCF coverage and steady dividends. It pairs this with moderate buybacks, balancing payouts and reinvestment sustainably. NUS offers a higher dividend yield (~3.5-8%) but with volatile earnings and inconsistent buybacks. NUS’s payout is riskier due to negative or low net margins in recent years. I see CL’s disciplined dividend and buyback mix as more sustainable. Thus, CL offers a superior total return profile for 2026 investors seeking steady, dependable rewards.

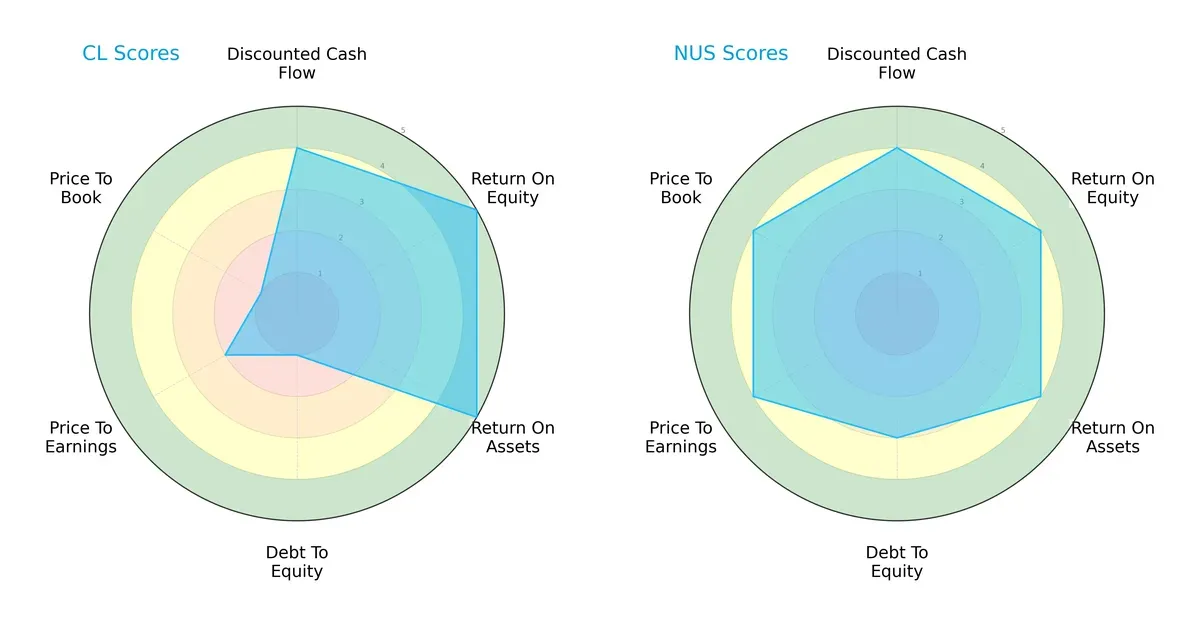

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Colgate-Palmolive and Nu Skin, highlighting their core financial strengths and valuation nuances:

Colgate-Palmolive excels in profitability with top-tier ROE and ROA scores (5 each), but it carries significant financial risk indicated by a very unfavorable debt-to-equity score (1). Nu Skin offers a more balanced profile, maintaining favorable scores across profitability, leverage, and valuation metrics. Nu Skin’s stronger valuation scores (P/E and P/B at 4) suggest better market pricing relative to fundamentals, while Colgate leans heavily on operational efficiency but struggles with balance sheet risk. Nu Skin’s diversified edge may appeal more in this cycle.

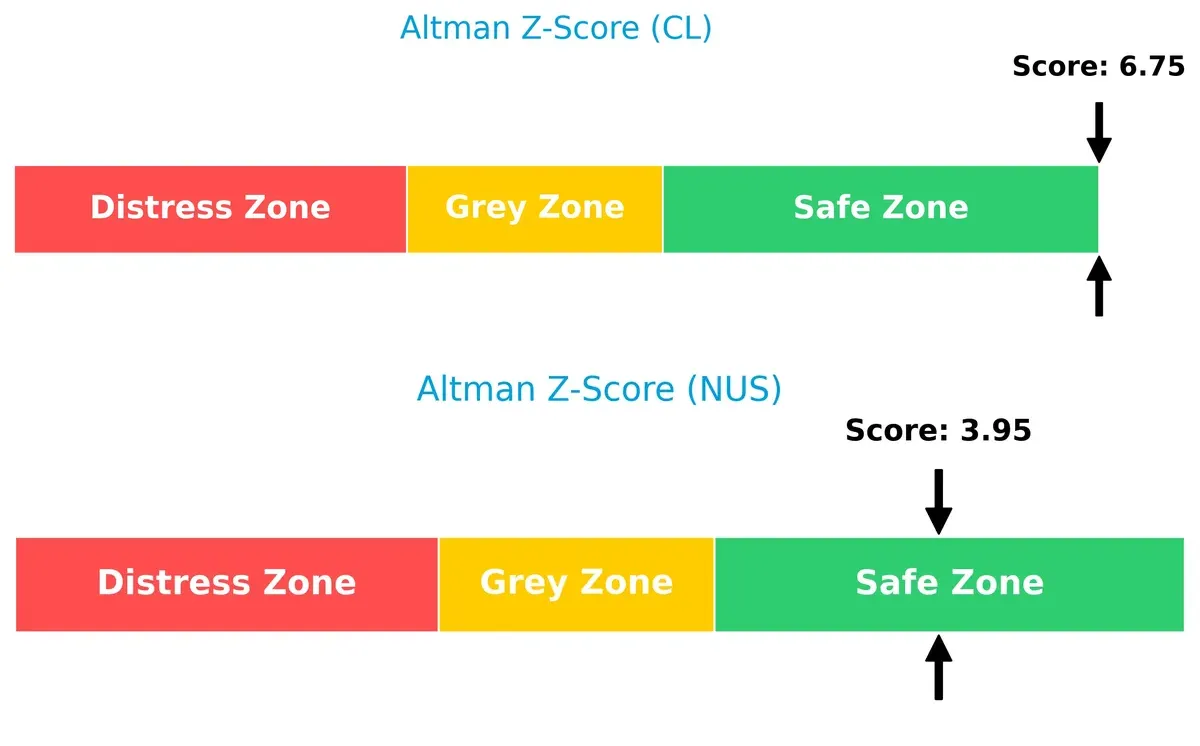

Bankruptcy Risk: Solvency Showdown

Colgate’s Altman Z-Score of 6.75 far surpasses Nu Skin’s 3.95, firmly placing both in the safe zone but clearly indicating Colgate’s superior long-term solvency and resilience in downturns:

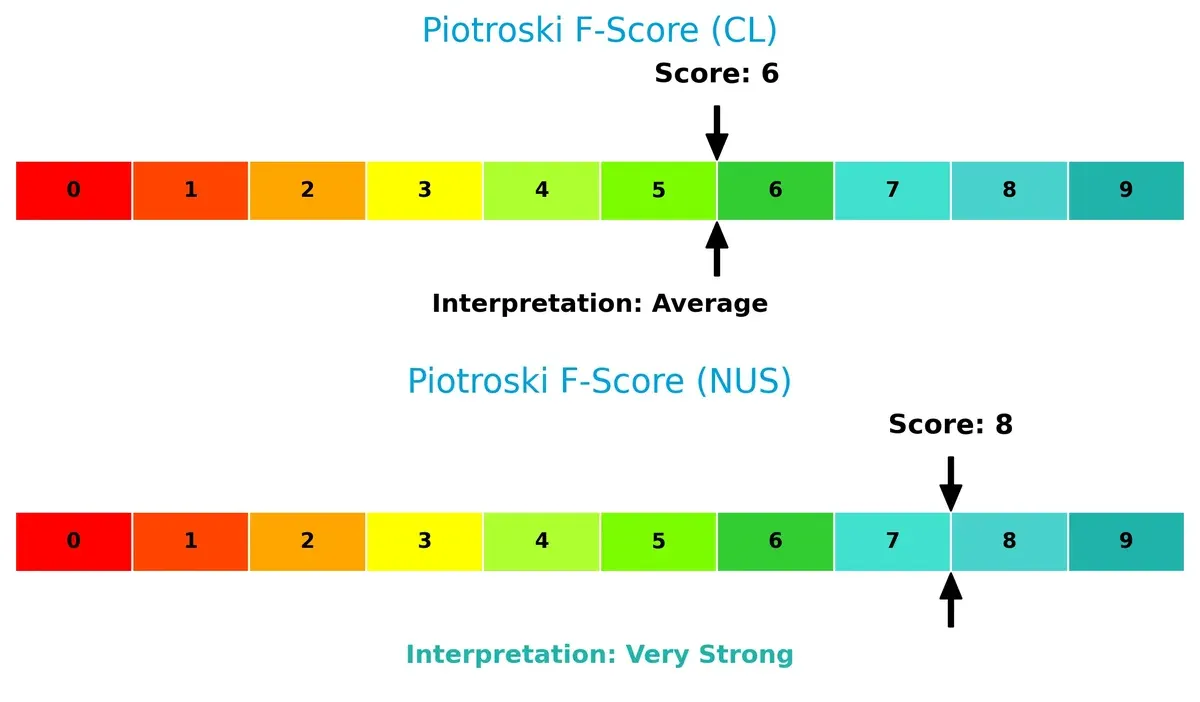

Financial Health: Quality of Operations

Nu Skin’s Piotroski F-Score of 8 signals very strong internal financial health, outperforming Colgate’s average score of 6. This suggests Nu Skin manages profitability, liquidity, and efficiency more effectively, while Colgate shows some red flags in operational consistency:

How are the two companies positioned?

This section dissects Colgate-Palmolive and Nu Skin’s operational DNA by comparing their revenue distribution and internal strengths and weaknesses. The goal is to confront their economic moats to reveal which business model delivers the most resilient and sustainable competitive advantage today.

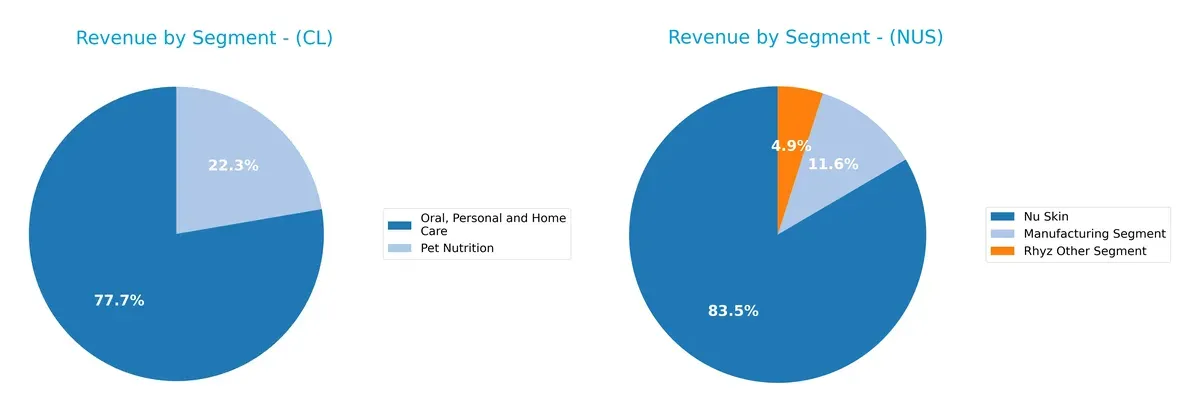

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how Colgate-Palmolive and Nu Skin diversify their income streams and where their primary sector bets lie:

Colgate-Palmolive anchors revenue in Oral, Personal and Home Care with $15.6B in 2024, complemented by $4.5B from Pet Nutrition, showing moderate diversification. Nu Skin, by contrast, pivots heavily on its Nu Skin segment with $1.45B, while smaller segments like Manufacturing ($201M) and Rhyz ($85M) contribute less. Colgate’s broader product ecosystem reduces concentration risk, while Nu Skin’s reliance on its flagship unit increases exposure but may deepen customer lock-in.

Strengths and Weaknesses Comparison

This table compares the strengths and weaknesses of Colgate-Palmolive Company and Nu Skin Enterprises, Inc.:

Colgate-Palmolive Company Strengths

- Strong profitability with net margin 14.37% and ROIC 30.56%

- Favorable interest coverage at 12.46

- Solid asset turnover metrics

- Consistent dividend yield of 2.41%

Nu Skin Enterprises, Inc. Strengths

- Favorable valuation ratios with P/E negative but considered as a strength

- Strong liquidity ratios: current ratio 1.82 and quick ratio 1.17

- Diverse geographic presence across Americas, Asia, and Europe

- Dividend yield higher at 3.49%

Colgate-Palmolive Company Weaknesses

- Weak liquidity with current ratio 0.92 and quick ratio 0.58

- High debt-to-assets ratio at 53.05%

- Elevated price-to-book ratio at 350.65

- Unfavorable debt-to-equity ratio at 40.15

- P/E ratio considered unfavorable at 25.73

Nu Skin Enterprises, Inc. Weaknesses

- Negative profitability metrics: net margin -8.46%, ROE -22.5%, ROIC -10.4%

- Negative interest coverage ratio at -5.63

- Debt ratios neutral but not strong

- Reliance on Nu Skin segment for majority revenue limits diversification

Colgate-Palmolive’s strengths lie in robust profitability and operational efficiency but face liquidity and leverage challenges. Nu Skin shows solid liquidity and valuation metrics but struggles with profitability and interest coverage. These contrasts imply differing strategic priorities on financial stability versus growth and market reach.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only shield protecting long-term profits from relentless competitive erosion. Let’s dissect the moats of two industry players:

Colgate-Palmolive Company: Enduring Brand & Cost Advantage

Colgate’s moat stems from powerful brand loyalty and cost efficiency. It sustains a high ROIC at 26%, well above WACC, reflecting consistent value creation. New product lines and global pet nutrition expansion could fortify this moat in 2026.

Nu Skin Enterprises, Inc.: Innovation-Driven but Vulnerable

Nu Skin relies on product innovation and direct selling. However, its ROIC is negative and declining steeply, signaling value destruction. Revenue setbacks and volatile margins threaten its moat, though expansion in Asia-Pacific markets offers some upside.

Moat Strength Showdown: Brand Loyalty vs. Innovation Risks

Colgate’s wide, growing moat outmatches Nu Skin’s shrinking and loss-making position. I see Colgate better equipped to protect and expand its market share in the shifting consumer goods landscape.

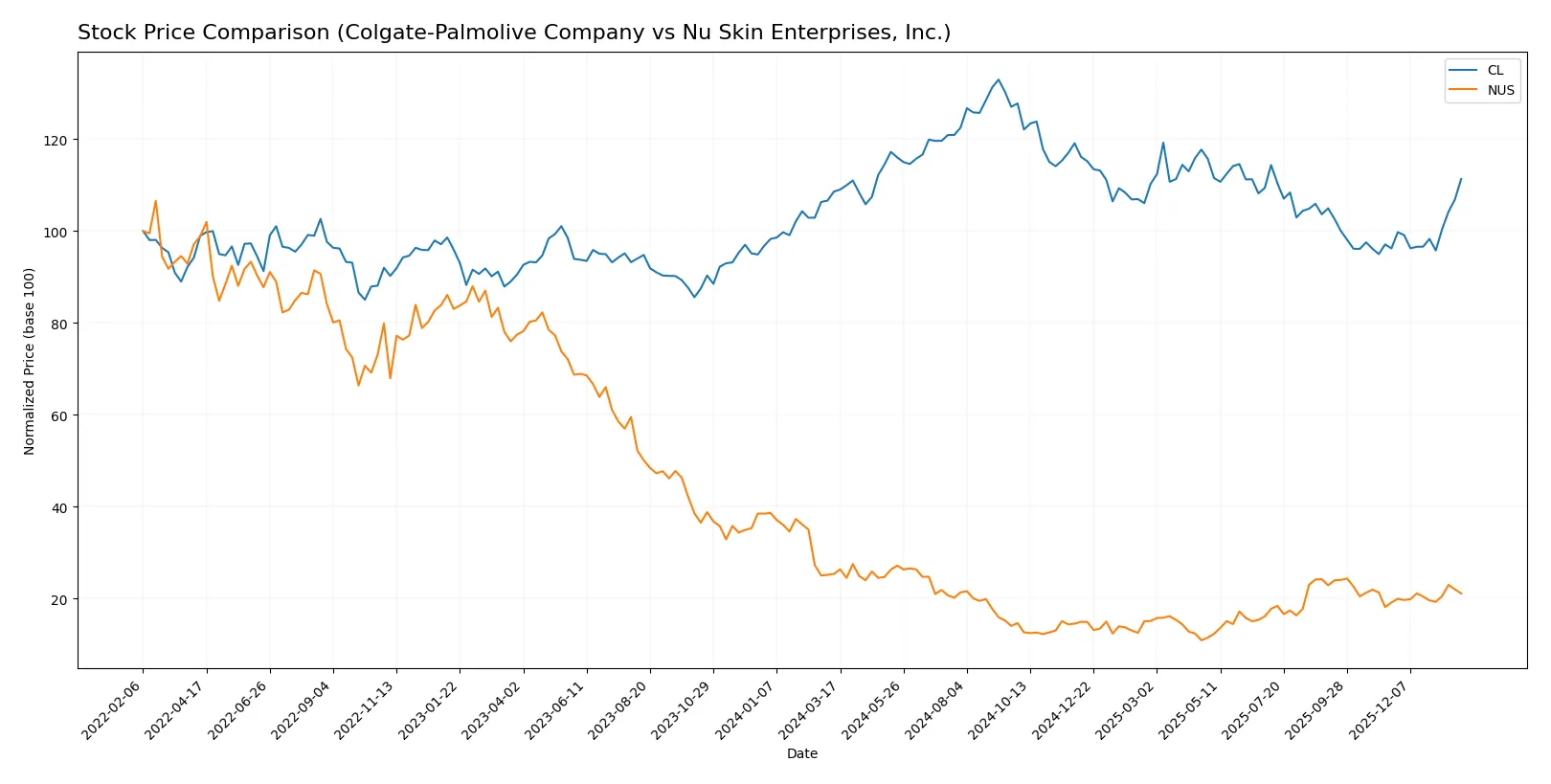

Which stock offers better returns?

The past year shows divergent price dynamics: Colgate-Palmolive posts a 2.52% gain with accelerating momentum, while Nu Skin Enterprises suffers a 16.72% decline despite recent moderate recovery.

Trend Comparison

Colgate-Palmolive exhibits a bullish trend over 12 months with a 2.52% gain and accelerating price increase. The stock ranges between 77.05 and 107.86, showing notable volatility (7.34 std dev).

Nu Skin Enterprises faces a bearish trend with a 16.72% loss over the year despite a recent 10.29% price rebound. Volatility remains low at 2.31 std dev, and the trend accelerates downward.

Colgate-Palmolive outperforms Nu Skin Enterprises, delivering positive returns and stronger buyer volume, while Nu Skin struggles with a significant overall decline.

Target Prices

Analysts show moderate upside potential for Colgate-Palmolive and a stable outlook for Nu Skin Enterprises.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Colgate-Palmolive Company | 83 | 96 | 89.2 |

| Nu Skin Enterprises, Inc. | 11 | 11 | 11 |

Colgate-Palmolive’s consensus target of 89.2 suggests a slight discount to its current 90.29 price, indicating cautious optimism. Nu Skin’s target matches its current price near 10.61, implying limited expected price movement.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Colgate-Palmolive Company Grades

Here are the recent institutional grades for Colgate-Palmolive Company:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| JP Morgan | Maintain | Overweight | 2026-01-16 |

| UBS | Maintain | Buy | 2026-01-14 |

| Wells Fargo | Upgrade | Equal Weight | 2026-01-13 |

| TD Cowen | Maintain | Buy | 2026-01-08 |

| Piper Sandler | Upgrade | Overweight | 2026-01-07 |

| JP Morgan | Maintain | Overweight | 2025-12-18 |

| Argus Research | Downgrade | Hold | 2025-12-11 |

| RBC Capital | Upgrade | Outperform | 2025-12-09 |

| Barclays | Maintain | Equal Weight | 2025-11-04 |

| Citigroup | Maintain | Buy | 2025-11-03 |

Nu Skin Enterprises, Inc. Grades

Here are the recent institutional grades for Nu Skin Enterprises, Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| DA Davidson | Maintain | Neutral | 2024-12-20 |

| Citigroup | Maintain | Neutral | 2024-10-22 |

| DA Davidson | Maintain | Neutral | 2024-08-12 |

| Citigroup | Maintain | Neutral | 2024-08-09 |

| DA Davidson | Maintain | Neutral | 2024-05-09 |

| DA Davidson | Maintain | Neutral | 2024-01-05 |

| Stifel | Maintain | Hold | 2023-10-16 |

| Stifel | Maintain | Hold | 2023-10-15 |

| Citigroup | Maintain | Neutral | 2023-09-29 |

| Citigroup | Maintain | Neutral | 2023-09-28 |

Which company has the best grades?

Colgate-Palmolive consistently receives higher grades such as Buy, Overweight, and Outperform from multiple reputable firms. Nu Skin’s grades remain Neutral or Hold, suggesting less bullish institutional sentiment. This difference may influence investor confidence and portfolio attractiveness.

Risks specific to each company

The following categories identify critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

Colgate-Palmolive Company

- Dominates mature consumer staples sector with strong brand portfolio and stable demand.

Nu Skin Enterprises, Inc.

- Faces intense competition in beauty and wellness; niche market but vulnerable to trends and distributor reliance.

2. Capital Structure & Debt

Colgate-Palmolive Company

- High debt-to-assets ratio (53%) signals leverage risk despite solid interest coverage.

Nu Skin Enterprises, Inc.

- Moderate leverage with 33% debt-to-assets and manageable debt/equity; interest coverage negative, showing risk in earnings to cover debt.

3. Stock Volatility

Colgate-Palmolive Company

- Low beta (0.28) suggests defensive stock with modest price swings.

Nu Skin Enterprises, Inc.

- Beta near 1 (0.98) indicates market-like volatility, higher risk for investors.

4. Regulatory & Legal

Colgate-Palmolive Company

- Exposure to global consumer product regulations but with established compliance frameworks.

Nu Skin Enterprises, Inc.

- Faces scrutiny over multi-level marketing practices; regulatory risks in international markets, especially China.

5. Supply Chain & Operations

Colgate-Palmolive Company

- Global supply chain benefits from scale but vulnerable to raw material inflation and logistics disruptions.

Nu Skin Enterprises, Inc.

- More concentrated supply base; operational risks heightened by direct selling model and international stores.

6. ESG & Climate Transition

Colgate-Palmolive Company

- Strong ESG commitments supporting sustainable sourcing and emissions reduction; reputational asset.

Nu Skin Enterprises, Inc.

- Emerging ESG initiatives but lags larger peers; climate transition risks less addressed.

7. Geopolitical Exposure

Colgate-Palmolive Company

- Diversified global footprint mitigates geopolitical shocks but remains exposed to trade tensions.

Nu Skin Enterprises, Inc.

- High exposure to Asia-Pacific markets, especially China, increases geopolitical and regulatory risk.

Which company shows a better risk-adjusted profile?

Colgate-Palmolive’s main risk lies in its elevated leverage despite strong profitability and stable cash flows. Nu Skin’s critical risk is poor earnings and negative interest coverage, compounded by regulatory and geopolitical vulnerabilities. I see Colgate-Palmolive offering a better risk-adjusted profile due to its defensive market position and superior financial health. Nu Skin’s volatility and operational risks, highlighted by its negative margins and regulatory scrutiny, present more caution for investors.

Final Verdict: Which stock to choose?

Colgate-Palmolive stands out as a cash machine with a durable competitive advantage. Its ability to generate returns well above its cost of capital underscores operational excellence. A point of vigilance remains its stretched liquidity ratios, which merit close monitoring. This stock suits investors aiming for steady, long-term value in a defensive portfolio.

Nu Skin’s strategic moat lies in its lean balance sheet and attractive valuation multiples. Its higher liquidity and lower debt levels offer relative safety compared to Colgate. However, persistent profitability challenges and declining returns signal caution. Nu Skin could fit portfolios focused on turnaround potential with a tolerance for volatility.

If you prioritize resilient cash flow and proven capital efficiency, Colgate outshines with durable profitability and stable returns. However, if you seek a contrarian play with favorable valuation and healthier liquidity, Nu Skin offers better stability amid operational headwinds. Each stock appeals to distinct investor profiles balancing growth and risk.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Colgate-Palmolive Company and Nu Skin Enterprises, Inc. to enhance your investment decisions: