Home > Comparison > Consumer Defensive > CL vs ELF

The strategic rivalry between Colgate-Palmolive Company and e.l.f. Beauty, Inc. shapes the competitive landscape of the Household & Personal Products sector. Colgate-Palmolive operates as a capital-intensive multinational with diversified oral, personal care, and pet nutrition products, while e.l.f. Beauty focuses on high-growth cosmetics and skincare with a direct-to-consumer edge. This analysis will clarify which business model delivers superior risk-adjusted returns for a diversified portfolio in 2026.

Table of contents

Companies Overview

Colgate-Palmolive and e.l.f. Beauty represent two distinct forces shaping the Household & Personal Products sector.

Colgate-Palmolive Company: Legacy Consumer Goods Powerhouse

Colgate-Palmolive dominates with a diversified product portfolio spanning oral care, personal hygiene, and pet nutrition. Its core revenue derives from trusted brands like Colgate toothpaste and Hill’s pet food. In 2026, it emphasizes expanding eCommerce channels and innovation in health-focused products to sustain its global market leadership.

e.l.f. Beauty, Inc.: Digital-Native Beauty Innovator

e.l.f. Beauty centers on affordable cosmetics and skincare with a strong direct-to-consumer digital model. Revenue flows primarily from online sales and retail partnerships under brands like e.l.f. Cosmetics and Well People. The company’s 2026 strategy targets international expansion and strengthening its eCommerce presence to capture younger demographics.

Strategic Collision: Similarities & Divergences

Both firms compete in personal care but differ sharply in philosophy: Colgate-Palmolive leverages a broad, trusted brand ecosystem; e.l.f. pursues agile, digitally native growth. Their primary battlefield is the shifting consumer preference towards online shopping. This contrast defines their distinct investment profiles—stable legacy dominance versus dynamic growth potential.

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

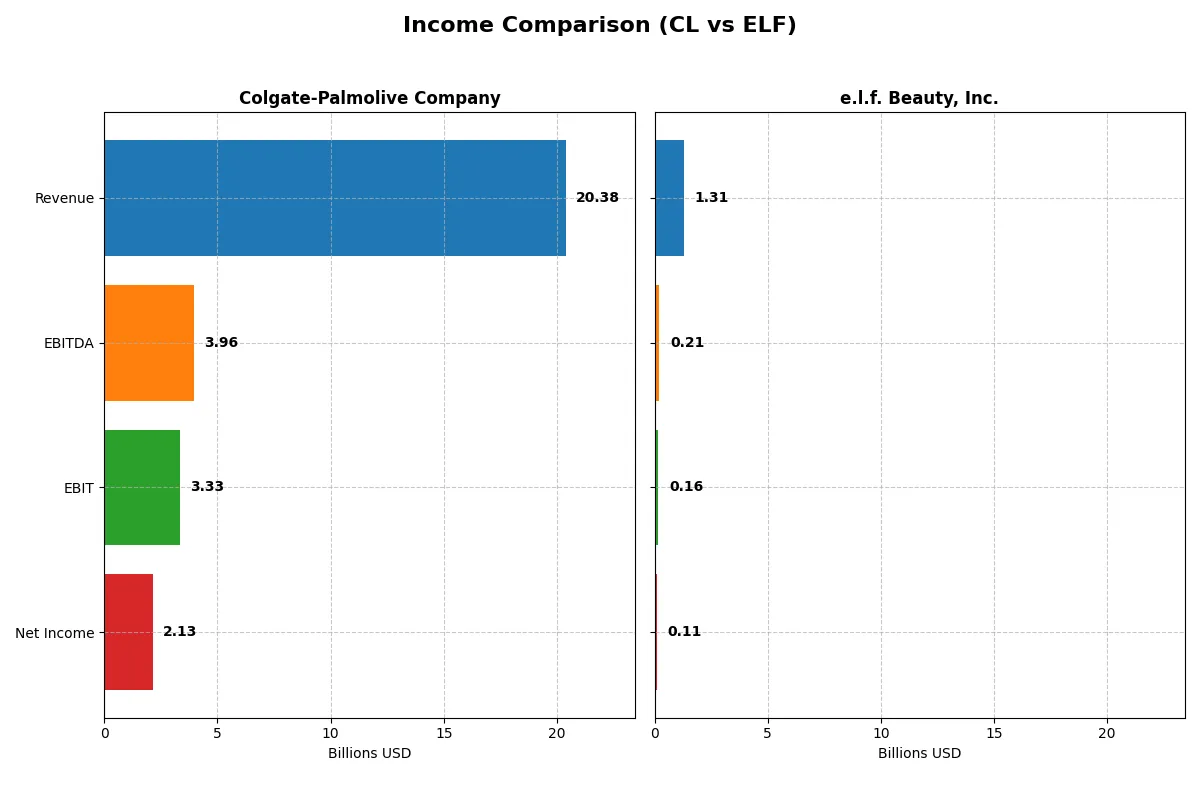

| Metric | Colgate-Palmolive Company (CL) | e.l.f. Beauty, Inc. (ELF) |

|---|---|---|

| Revenue | 20.38B | 1.31B |

| Cost of Revenue | 8.13B | 378M |

| Operating Expenses | 7.90B | 778M |

| Gross Profit | 12.25B | 936M |

| EBITDA | 3.96B | 206M |

| EBIT | 3.33B | 162M |

| Interest Expense | 267M | 17M |

| Net Income | 2.13B | 112M |

| EPS | 2.64 | 1.99 |

| Fiscal Year | 2025 | 2025 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals which company converts revenue into profit more efficiently and sustains margin strength over time.

Colgate-Palmolive Company Analysis

Colgate-Palmolive’s revenue grew steadily, reaching 20.4B in 2025, but net income declined to 2.13B, reflecting margin pressure. Its gross margin remains strong at 60.1%, yet net margin slipped to 10.5%. The latest year shows weakening EBIT by 21.7%, signaling deteriorating operational efficiency despite scale.

e.l.f. Beauty, Inc. Analysis

e.l.f. Beauty surged revenue 28% to 1.31B in fiscal 2025, with net income at 112M. Gross margin impresses at 71.2%, but net margin trails at 8.5%. EBIT rose 6.4%, showing operational momentum, though net margin contraction of 31.6% reveals cost growth outpacing profit gains amid rapid expansion.

Margin Resilience vs. Growth Velocity

Colgate-Palmolive delivers superior margin stability but faces shrinking profitability in 2025. e.l.f. Beauty outpaces in revenue and net income growth with robust gross margins yet struggles with net margin compression. Investors seeking steady margin power may favor Colgate, while those prioritizing high growth momentum might lean toward e.l.f. Beauty’s dynamic profile.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies analyzed:

| Ratios | Colgate-Palmolive Company (CL) | e.l.f. Beauty, Inc. (ELF) |

|---|---|---|

| ROE | 13.63% | 14.73% |

| ROIC | 30.56% | 11.21% |

| P/E | 25.73 | 31.49 |

| P/B | 350.65 | 4.64 |

| Current Ratio | 0.92 | 3.05 |

| Quick Ratio | 0.58 | 2.00 |

| D/E (Debt-to-Equity) | 40.15 | 0.41 |

| Debt-to-Assets | 53.05% | 25.08% |

| Interest Coverage | 15.01 | 9.20 |

| Asset Turnover | 1.25 | 1.05 |

| Fixed Asset Turnover | 4.55 | 45.63 |

| Payout ratio | 61.92% | 0% |

| Dividend yield | 2.41% | 0% |

| Fiscal Year | 2024 | 2025 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios act as a company’s DNA, exposing hidden risks and revealing operational strengths beneath the surface.

Colgate-Palmolive Company

Colgate posts a strong 13.6% ROE and a robust 14.4% net margin, signaling efficient profitability. However, its P/E of 25.7 and P/B of 350.7 mark the stock as stretched relative to traditional benchmarks. The firm rewards shareholders with a 2.41% dividend yield, balancing income with stable capital allocation.

e.l.f. Beauty, Inc.

e.l.f. Beauty shows a modest 14.7% ROE and an 8.5% net margin, reflecting moderate profitability. The P/E ratio at 31.5 suggests an expensive valuation, while the absence of dividends indicates reinvestment focused on growth. Its strong quick ratio and low debt highlight financial flexibility despite valuation concerns.

Valuation Stretch vs. Operational Efficiency

Colgate delivers superior returns and income but trades at a stretched valuation with some liquidity concerns. e.l.f. Beauty offers growth potential with solid financial health but at a higher P/E and no dividend. Investors seeking stable income may prefer Colgate, while growth-oriented profiles might lean toward e.l.f. Beauty.

Which one offers the Superior Shareholder Reward?

Colgate-Palmolive (CL) delivers steady shareholder returns with a 2.4% dividend yield and a 62% payout ratio, supported by robust free cash flow coverage (1.75x). Its consistent buybacks enhance total returns. e.l.f. Beauty (ELF) pays no dividend, focusing entirely on reinvestment and growth, with moderate buyback activity. CL’s balanced dividend and buyback model offers more sustainable, attractive total returns for 2026 investors.

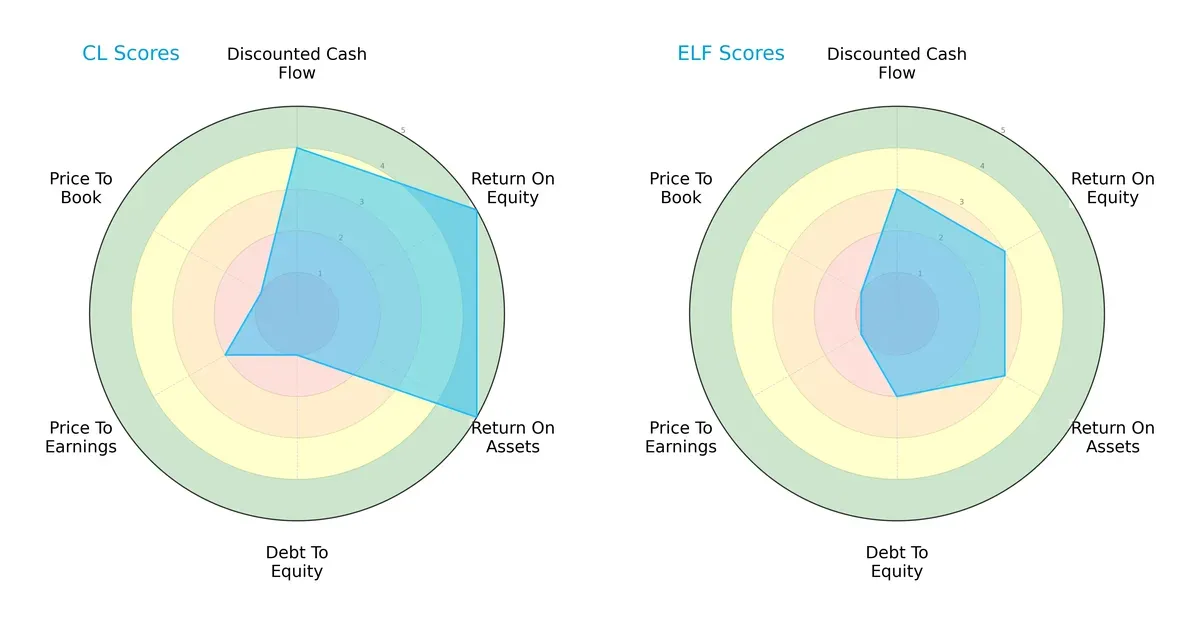

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of both firms, highlighting their financial strengths and valuation nuances:

Colgate-Palmolive dominates in profitability with top ROE and ROA scores (5 each), signaling efficient capital use. However, its debt-to-equity score of 1 exposes a heavy leverage risk. e.l.f. Beauty shows a more moderate but balanced profile, avoiding extreme leverage with a debt-to-equity score of 2. Valuation metrics favor neither, with both companies scoring poorly on price-to-book. Colgate relies on operational excellence but carries financial risk; e.l.f. offers steadier, if less spectacular, fundamentals.

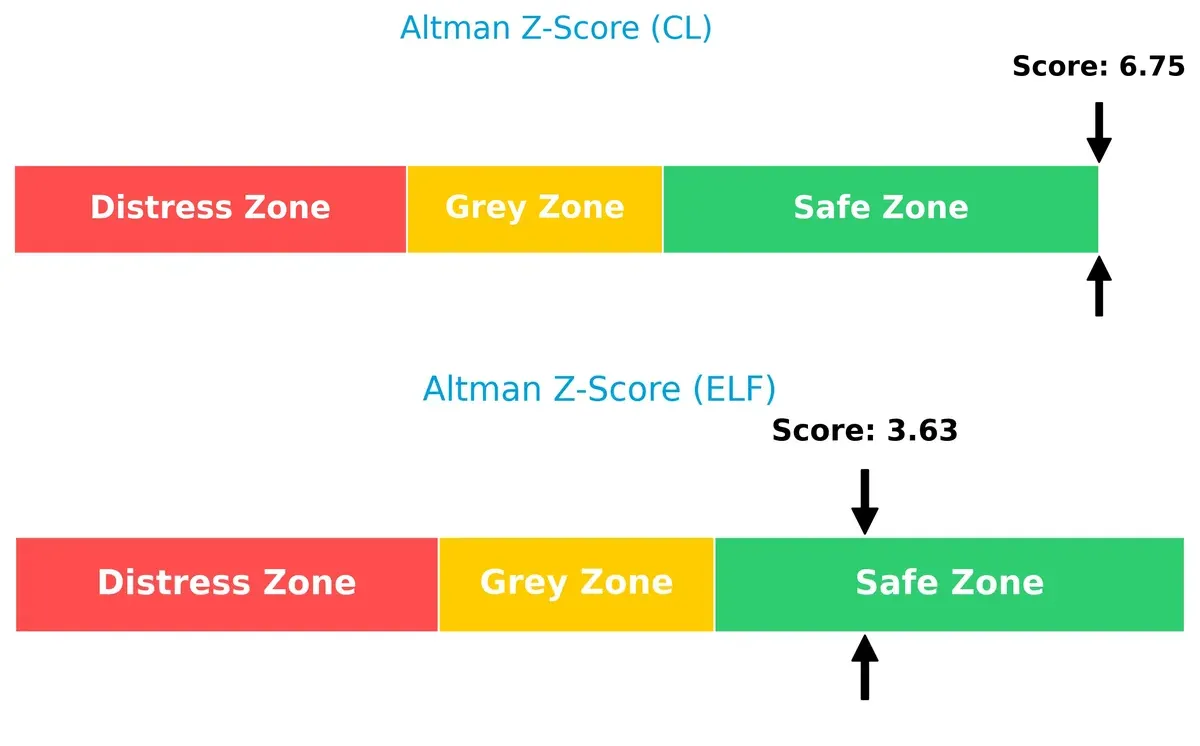

Bankruptcy Risk: Solvency Showdown

Colgate’s Altman Z-Score of 6.75 far exceeds e.l.f. Beauty’s 3.63, placing both safely above distress thresholds but showing a clear margin of solvency superiority for Colgate:

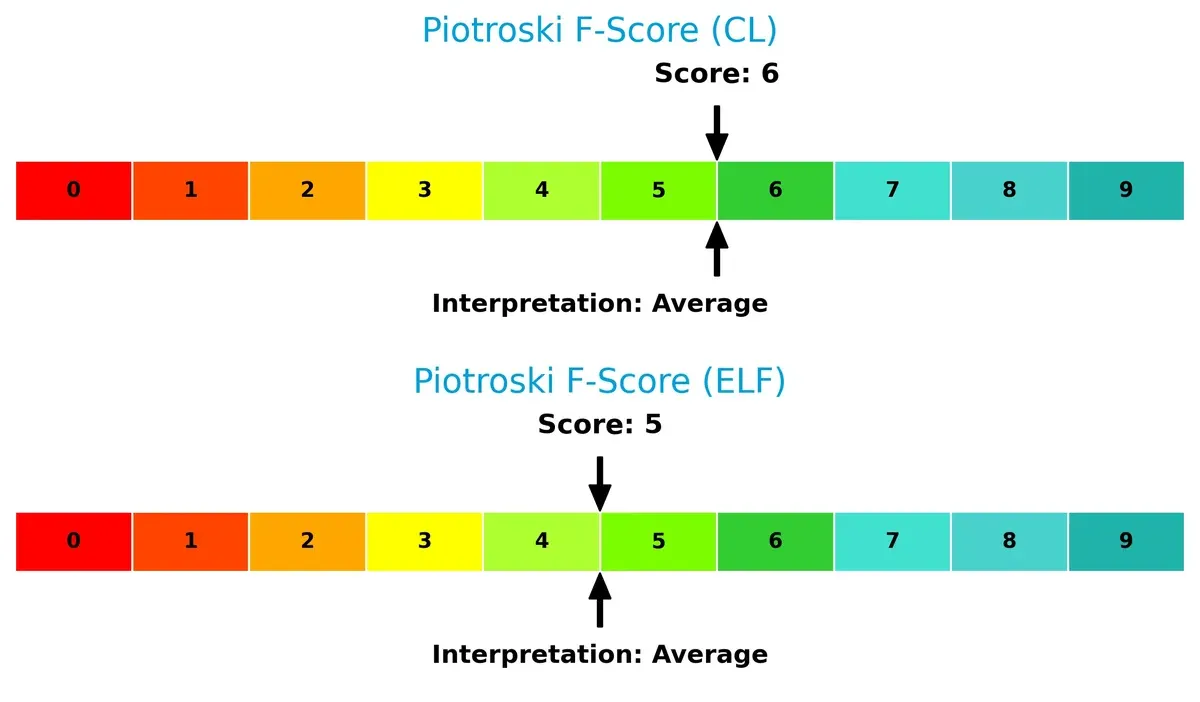

Financial Health: Quality of Operations

Colgate scores a 6 on the Piotroski scale, slightly edging out e.l.f. Beauty’s 5. Both sit in the average range, but Colgate’s higher score suggests more robust internal financial controls and operational quality:

How are the two companies positioned?

This section dissects the operational DNA of CL and ELF by comparing their revenue distribution and internal dynamics—strengths and weaknesses. The goal is to confront their economic moats to identify which model offers the most resilient, sustainable advantage today.

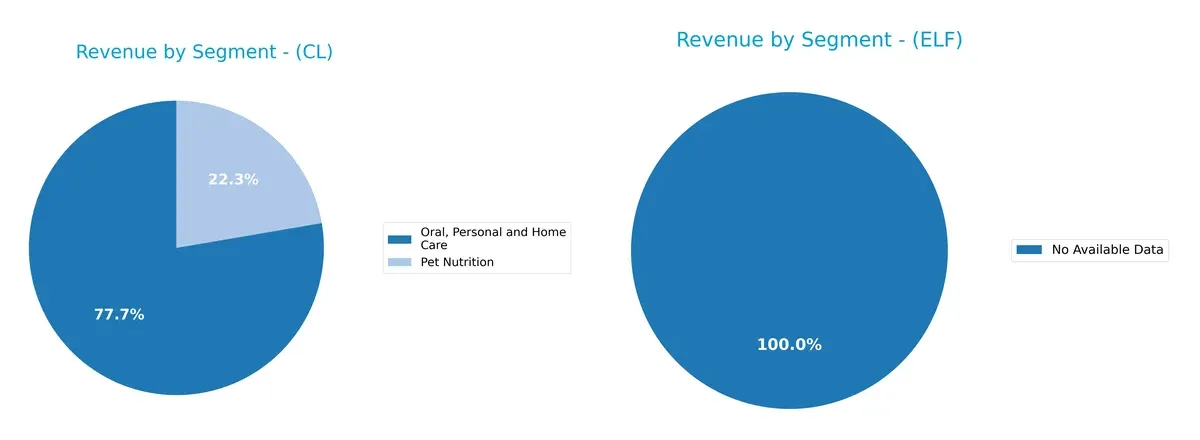

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how both firms diversify their income streams and where their primary sector bets lie:

Colgate-Palmolive anchors its revenue in Oral, Personal and Home Care with $15.6B in 2024, complemented by $4.5B from Pet Nutrition. e.l.f. Beauty, Inc. lacks available segment data for comparison. Colgate’s focused yet dual-segment approach balances stable consumer staples with growth in pet nutrition, reducing concentration risk and leveraging ecosystem lock-in. Without e.l.f.’s data, Colgate stands alone in this analysis.

Strengths and Weaknesses Comparison

This table compares the strengths and weaknesses of Colgate-Palmolive Company (CL) and e.l.f. Beauty, Inc. (ELF):

CL Strengths

- Diversified revenue streams across Oral Care and Pet Nutrition

- High net margin at 14.37%

- Very strong ROE at 1362.74%

- Favorable ROIC at 30.56% above WACC

- Solid interest coverage ratio at 12.46

- Consistent asset turnover supporting efficiency

- Dividend yield of 2.41%

ELF Strengths

- Favorable quick ratio at 2.0 indicates liquidity

- Low debt-to-equity at 0.41 reduces financial risk

- Favorable fixed asset turnover at 45.63 shows asset efficiency

- Positive interest coverage at 9.44

- Growing US and international revenue presence

- Asset turnover at 1.05 indicates operational efficiency

CL Weaknesses

- Low current ratio at 0.92 signals liquidity risks

- High debt-to-assets at 53.05% raises leverage concerns

- Unfavorable PE at 25.73 and PB at 350.65 suggest valuation issues

- Quick ratio low at 0.58

- Debt-to-equity at 40.15 signals increased leverage

- No geographic revenue breakdown to confirm diversification

ELF Weaknesses

- Neutral net margin at 8.53% below CL’s

- ROIC at 11.21% below WACC at 11.5% indicates value destruction

- Unfavorable PE at 31.49 and PB at 4.64

- Current ratio high at 3.05 may suggest underutilized assets

- Zero dividend yield limits income appeal

- Global ratios opinion neutral, reflecting mixed financial health

Colgate’s strength lies in robust profitability and diversified product segments but faces liquidity and leverage risks. e.l.f. shows operational efficiency and lower leverage but struggles with profitability and value creation. Both companies’ financial profiles suggest distinct strategic challenges and opportunities.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only true barrier protecting a company’s long-term profits from relentless competitive erosion:

Colgate-Palmolive Company: Enduring Brand and Scale Advantage

Colgate’s moat centers on powerful brand loyalty and vast distribution scale. It sustains high ROIC (26%) well above WACC, reflecting efficient capital use. In 2026, new product lines and pet nutrition expansion could deepen this durable moat.

e.l.f. Beauty, Inc.: Rapid Growth with Emerging Innovation

e.l.f. leverages innovation and e-commerce agility as its moat, contrasting Colgate’s legacy brands. Despite ROIC below WACC, e.l.f.’s soaring revenue growth (28% last year) signals expanding market traction and potential for future profitability gains.

Brand Legacy vs. Growth Innovation: Who Defends Better?

Colgate’s wider moat delivers consistent value creation and margin stability. e.l.f. shows a narrower moat but accelerating profitability trends. Colgate remains better equipped to defend its market share amid economic cycles.

Which stock offers better returns?

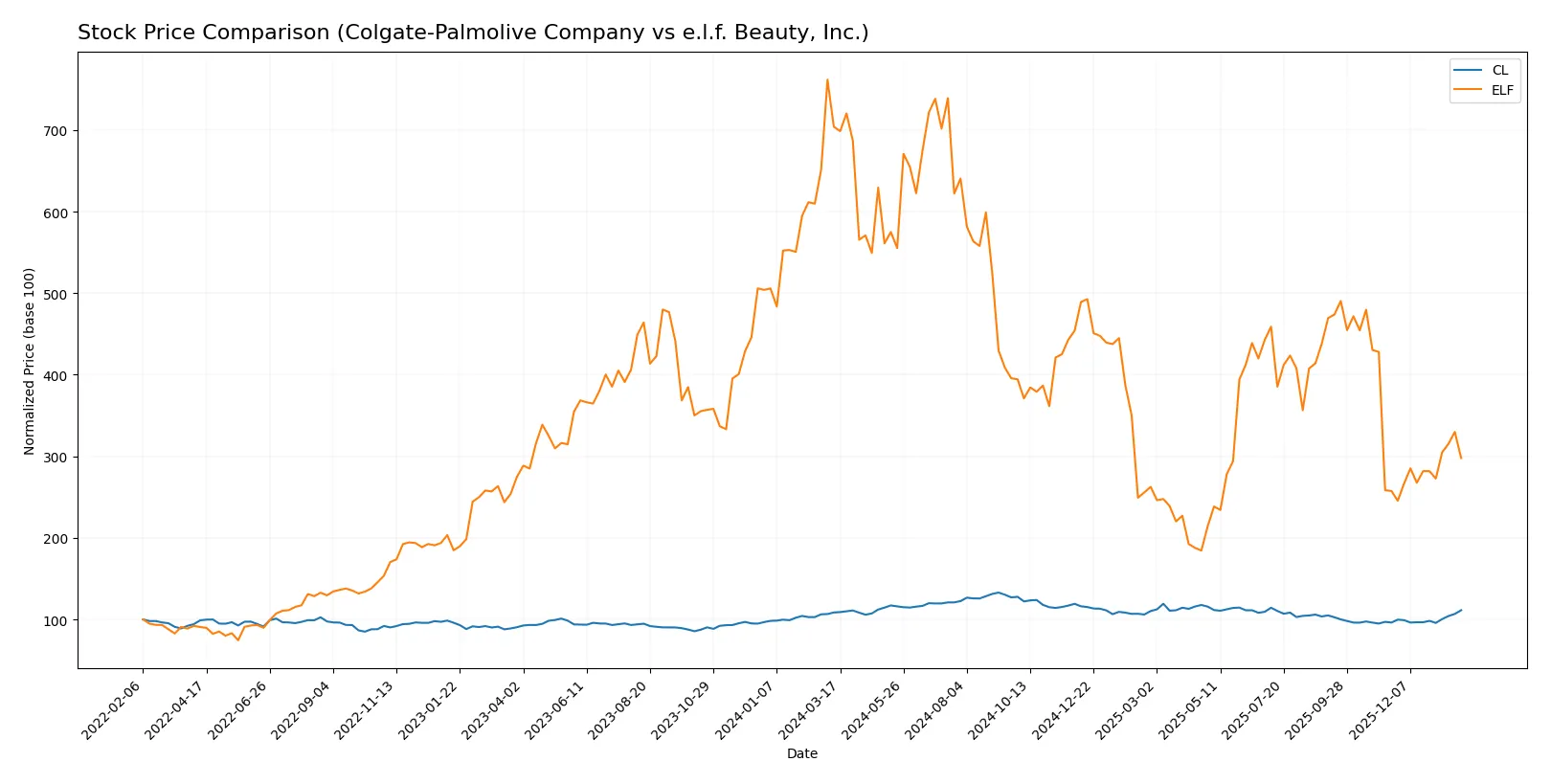

Stock price movements over the past year reveal a clear divergence: Colgate-Palmolive Company shows modest gains with accelerating momentum, while e.l.f. Beauty, Inc. suffers a steep decline despite recent short-term recovery.

Trend Comparison

Colgate-Palmolive’s stock gained 2.52% over the past year, marking a bullish trend with acceleration and moderate volatility (7.34 std deviation). It ranged between $77.05 and $107.86.

e.l.f. Beauty’s stock fell sharply by 57.7%, signaling a bearish trend despite recent acceleration. Volatility was high at 41.79 std deviation, with prices fluctuating between $52.65 and $210.9.

Comparing both, Colgate-Palmolive delivered superior market performance over twelve months, while e.l.f. Beauty experienced significant depreciation despite a recent positive price slope.

Target Prices

Analysts present a broad but constructive target price range for both Colgate-Palmolive Company and e.l.f. Beauty, Inc.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Colgate-Palmolive Company | 83 | 96 | 89.2 |

| e.l.f. Beauty, Inc. | 85 | 165 | 111.83 |

The consensus target for Colgate-Palmolive slightly undercuts its current price of 90.29, suggesting limited upside. e.l.f. Beauty’s consensus target exceeds its current 84.99 price, signaling potential growth opportunities.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Colgate-Palmolive Company Grades

The following table shows recent grades from respected financial institutions for Colgate-Palmolive:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| JP Morgan | Maintain | Overweight | 2026-01-16 |

| UBS | Maintain | Buy | 2026-01-14 |

| Wells Fargo | Upgrade | Equal Weight | 2026-01-13 |

| TD Cowen | Maintain | Buy | 2026-01-08 |

| Piper Sandler | Upgrade | Overweight | 2026-01-07 |

e.l.f. Beauty, Inc. Grades

Here are the latest institutional grades for e.l.f. Beauty from leading grading companies:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| TD Cowen | Maintain | Buy | 2026-01-21 |

| UBS | Maintain | Neutral | 2026-01-14 |

| Piper Sandler | Maintain | Neutral | 2025-12-22 |

| JP Morgan | Maintain | Overweight | 2025-12-18 |

| Goldman Sachs | Maintain | Buy | 2025-11-07 |

Which company has the best grades?

Colgate-Palmolive generally receives stronger grades, including multiple Buy and Overweight ratings with recent upgrades. e.l.f. Beauty’s grades cluster around Neutral and Buy, indicating more cautious optimism. Investors may view Colgate’s higher grades as a signal of greater institutional confidence and stability.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

Colgate-Palmolive Company

- Established global presence in household products with diversified segments. Faces mature market saturation.

e.l.f. Beauty, Inc.

- Smaller, niche player in cosmetics with rapid innovation but intense competition and brand volatility.

2. Capital Structure & Debt

Colgate-Palmolive Company

- High debt-to-equity ratio (40.15) and debt-to-assets (53.05%) signal considerable leverage risk.

e.l.f. Beauty, Inc.

- Low debt levels (DE 0.41, debt-to-assets 25.08%) indicate conservative capital structure and lower financial risk.

3. Stock Volatility

Colgate-Palmolive Company

- Low beta (0.28) points to stability and defensive stock behavior amid market shifts.

e.l.f. Beauty, Inc.

- High beta (1.72) reflects strong sensitivity to market swings and higher price volatility.

4. Regulatory & Legal

Colgate-Palmolive Company

- Global operations expose it to multifaceted regulatory compliance, especially in health and safety standards.

e.l.f. Beauty, Inc.

- Primarily U.S.-centric but expanding internationally, facing evolving cosmetic regulations and trade compliance risks.

5. Supply Chain & Operations

Colgate-Palmolive Company

- Complex global supply chain susceptible to raw material cost inflation and geopolitical disruptions.

e.l.f. Beauty, Inc.

- Leaner supply chain enables agility but risks dependency on fewer suppliers and scale limitations.

6. ESG & Climate Transition

Colgate-Palmolive Company

- Significant pressure to reduce carbon footprint and improve sustainability across broad product lines.

e.l.f. Beauty, Inc.

- Emerging focus on ESG, but smaller scale may limit resources for large-scale climate initiatives.

7. Geopolitical Exposure

Colgate-Palmolive Company

- Extensive international footprint exposes it to currency risk, trade tariffs, and political instability.

e.l.f. Beauty, Inc.

- Limited global presence reduces geopolitical risks but may hinder growth opportunities abroad.

Which company shows a better risk-adjusted profile?

Colgate-Palmolive faces greater leverage and global operational risks but benefits from stable stock volatility and strong profitability. e.l.f. Beauty shows lower financial leverage and higher operational agility but suffers from elevated market volatility and valuation risks. I see Colgate’s risk-adjusted profile as more favorable due to its defensive market position and robust financial health despite capital structure concerns. e.l.f.’s high beta and stretched valuation multiples heighten its risk profile amid a volatile cosmetics sector.

Final Verdict: Which stock to choose?

Colgate-Palmolive’s superpower lies in its durable competitive advantage and exceptional capital efficiency. It generates strong returns well above its cost of capital, signaling consistent value creation. Its point of vigilance is a stretched balance sheet, which could pressure liquidity in volatile cycles. It fits well within conservative, income-focused portfolios seeking stable growth.

e.l.f. Beauty leverages a strategic moat rooted in rapid revenue expansion and brand momentum. Its lighter debt profile offers relative safety compared to Colgate, despite lower capital efficiency. However, valuation multiples remain elevated, reflecting growth expectations. This stock appeals to growth-at-a-reasonable-price (GARP) investors willing to embrace higher volatility for potential outsized returns.

If you prioritize steady value creation and capital preservation, Colgate outshines with its proven moat and stable dividends. However, if you seek aggressive growth fueled by rising market share and can tolerate valuation risk, e.l.f. Beauty offers superior growth prospects. Both present distinct analytical scenarios aligned with differing investor risk profiles.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Colgate-Palmolive Company and e.l.f. Beauty, Inc. to enhance your investment decisions: