Home > Comparison > Technology > SNDK vs COHR

The strategic rivalry between Sandisk Corporation and Coherent, Inc. shapes the technology hardware sector’s evolution. Sandisk excels as a specialist in NAND flash storage solutions, focusing on solid-state drives and embedded products. In contrast, Coherent operates as a diversified laser technology provider, servicing industrial and scientific applications. This analysis probes their contrasting models to identify which offers superior risk-adjusted returns, guiding portfolio decisions amid ongoing technological advances and market dynamics.

Table of contents

Companies Overview

Sandisk Corporation and Coherent, Inc. stand as pivotal players in the technology hardware sector, shaping distinct niches within the industry.

Sandisk Corporation: Leader in Flash Storage Solutions

Sandisk dominates the NAND flash storage market, generating revenue primarily through solid state drives, embedded products, and removable cards. In 2026, its strategic focus remains on expanding high-performance storage solutions, leveraging its strong market position and technological expertise to meet growing digital storage demands worldwide.

Coherent, Inc.: Pioneer in Laser Technology

Coherent excels in laser-based systems and precision optics, selling through OEM and industrial laser segments. Its latest strategy centers on integrating advanced laser technologies across microelectronics and scientific applications, aiming to enhance product innovation and global sales reach as a subsidiary of II-VI Incorporated.

Strategic Collision: Similarities & Divergences

Both companies operate in hardware but diverge sharply; Sandisk emphasizes digital storage, while Coherent focuses on laser precision and optics. Their primary battleground lies in tech innovation—storage versus laser solutions. Investors face distinct profiles: Sandisk offers exposure to memory tech growth; Coherent provides a play on advanced laser systems and industrial applications.

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Sandisk Corporation (SNDK) | Coherent, Inc. (COHR) |

|---|---|---|

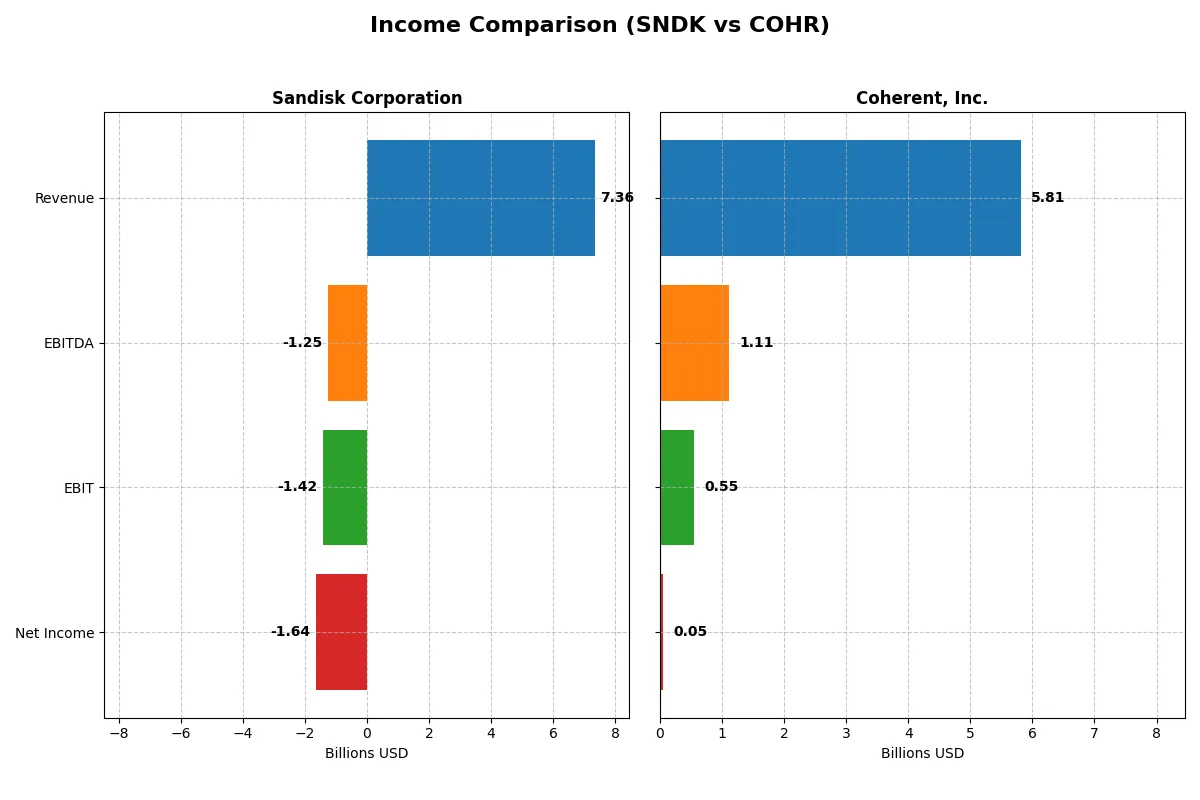

| Revenue | 7.36B | 5.81B |

| Cost of Revenue | 5.14B | 3.75B |

| Operating Expenses | 3.59B | 1.51B |

| Gross Profit | 2.21B | 2.06B |

| EBITDA | -1.25B | 1.11B |

| EBIT | -1.42B | 552M |

| Interest Expense | 63M | 243M |

| Net Income | -1.64B | 49M |

| EPS | -11.32 | -0.52 |

| Fiscal Year | 2025 | 2025 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals which company runs a more efficient and profitable core business engine through recent fiscal years.

Sandisk Corporation Analysis

Sandisk’s revenue declined overall from 9.75B in 2022 to 7.35B in 2025, with a recent 10.4% growth in 2025. Despite a favorable 30.1% gross margin in 2025, net income plunged deeply negative to -1.64B, reflecting steep losses and a -22.3% net margin. Operating inefficiencies and high expenses weighed heavily on the bottom line.

Coherent, Inc. Analysis

Coherent’s revenue expanded strongly from 3.32B in 2022 to 5.81B in 2025, a 23.4% jump in the latest year. Its 35.4% gross margin outperforms Sandisk’s, while its EBIT margin improved to 9.5%, supporting a near-breakeven net margin of 0.85%. The company shows momentum with expanding profitability and operational control.

Verdict: Margin Resilience vs. Revenue Recovery

Coherent displays superior margin health and operational momentum, turning revenue growth into positive net income near breakeven. Sandisk’s revenue growth in 2025 fails to offset deep structural losses and negative margins. For investors, Coherent’s profile offers a clearer path to sustainable profitability and risk-managed growth.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | Sandisk Corporation (SNDK) | Coherent, Inc. (COHR) |

|---|---|---|

| ROE | -17.81% | 0.61% |

| ROIC | -11.89% | 1.31% |

| P/E | -4.17 | 279.75 |

| P/B | 0.74 | 1.70 |

| Current Ratio | 3.56 | 2.19 |

| Quick Ratio | 2.11 | 1.39 |

| D/E | 0.22 | 0.48 |

| Debt-to-Assets | 15.73% | 26.11% |

| Interest Coverage | -21.86 | 2.26 |

| Asset Turnover | 0.57 | 0.39 |

| Fixed Asset Turnover | 11.88 | 3.09 |

| Payout ratio | 0 | 23.17% |

| Dividend yield | 0% | 0.08% |

| Fiscal Year | 2025 | 2025 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios act as the company’s DNA, exposing hidden risks while spotlighting operational efficiency and value precision.

Sandisk Corporation

Sandisk shows weak profitability with a negative ROE of -17.81% and net margin at -22.31%, signaling operational challenges. Its valuation appears reasonable, with a P/E of -4.17 and P/B of 0.74, suggesting undervaluation. Sandisk pays no dividend, instead channeling capital into R&D, evident from a 15.4% R&D-to-revenue ratio, aiming for growth.

Coherent, Inc.

Coherent’s profitability is marginally positive but weak, with ROE of 0.61% and net margin below 1%. The stock trades at a stretched P/E of 280, reflecting high growth expectations. Despite minimal dividend yield (0.08%), Coherent invests around 10% of revenue in R&D, prioritizing innovation amid modest operational returns.

Valuation Discipline vs. Growth Ambition

Sandisk offers a more attractive valuation and stronger capital allocation towards R&D, despite current losses. Coherent’s elevated multiples imply riskier growth bets with weak profitability. Investors seeking value and operational improvement might prefer Sandisk’s profile, while those focused on long-term growth could consider Coherent’s high-expectation stance.

Which one offers the Superior Shareholder Reward?

I observe that Sandisk Corporation (SNDK) pays no dividends and posts negative free cash flow, reflecting a reinvestment focus amid recent losses. Coherent, Inc. (COHR) yields a modest 0.08% dividend with a 23% payout ratio, supported by positive free cash flow of 1.25/share in 2025. COHR also maintains steady buybacks, enhancing shareholder returns. SNDK’s lack of distributions and negative earnings cast doubt on near-term rewards. COHR’s balanced dividend and buyback approach offers a more sustainable, attractive total return profile for 2026 investors.

Comparative Score Analysis: The Strategic Profile

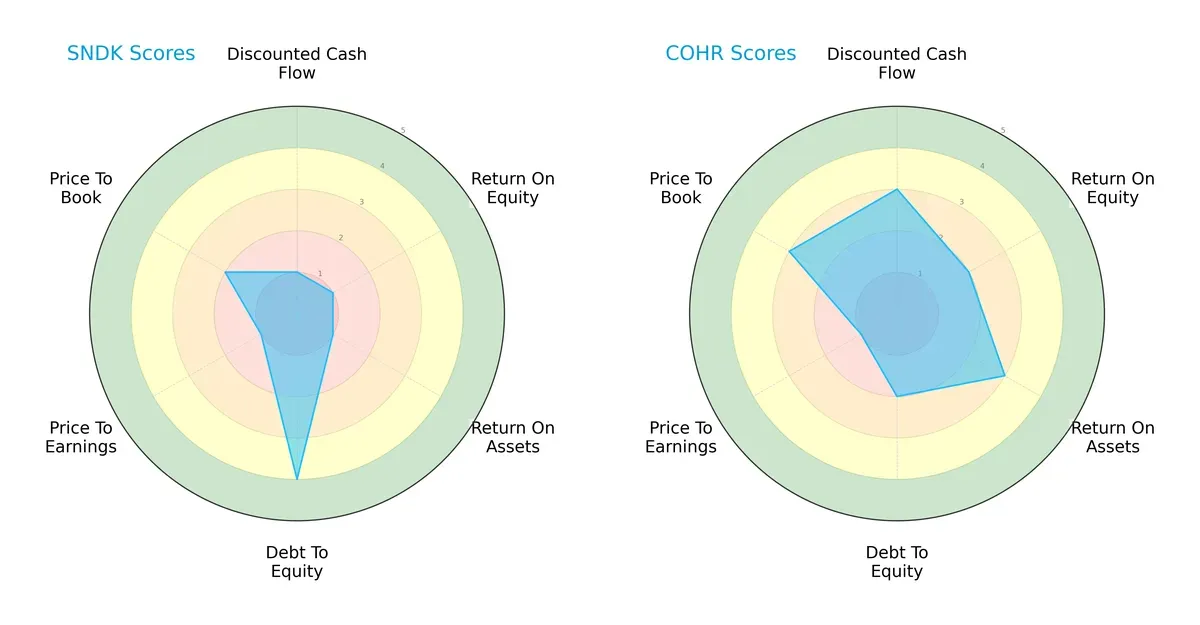

The radar chart reveals the fundamental DNA and trade-offs of Sandisk Corporation and Coherent, Inc., highlighting their financial strengths and weaknesses:

Coherent shows superior scores in discounted cash flow (3 vs. 1), ROE (2 vs. 1), and ROA (3 vs. 1), indicating more efficient asset use and profitability. Sandisk’s standout strength lies in debt management (4 vs. 2), signaling a conservative leverage profile. However, both struggle with price-to-earnings valuation (1 each), reflecting market skepticism. Coherent presents a more balanced profile, while Sandisk relies heavily on low leverage to offset weaker operational returns.

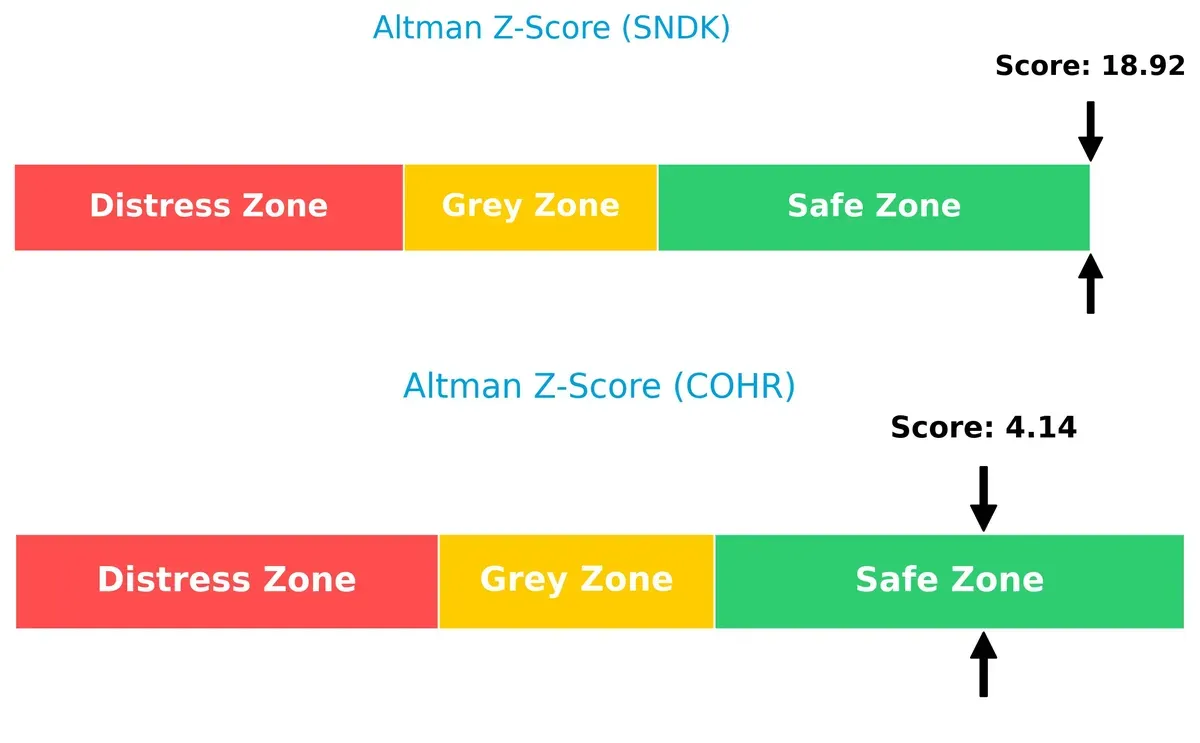

Bankruptcy Risk: Solvency Showdown

The Altman Z-Score gap favors Sandisk (18.9 vs. 4.1), signaling its superior long-term solvency and low bankruptcy risk in this economic cycle:

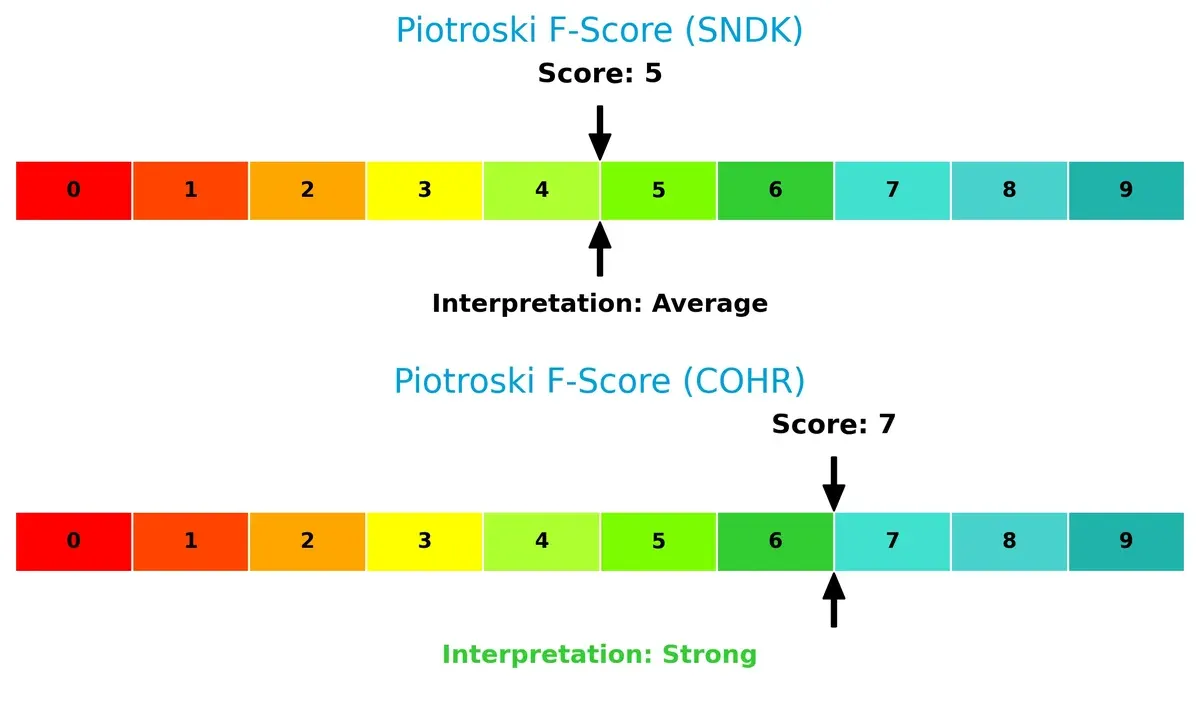

Financial Health: Quality of Operations

Coherent’s Piotroski F-Score of 7 surpasses Sandisk’s 5, indicating stronger internal financial health and operational quality. Sandisk’s average score raises caution about potential red flags in profitability or efficiency:

How are the two companies positioned?

This section dissects Sandisk and Coherent’s operational DNA by comparing their revenue segmentation and internal dynamics. The goal is to confront their economic moats and identify which model offers a more resilient, sustainable competitive advantage today.

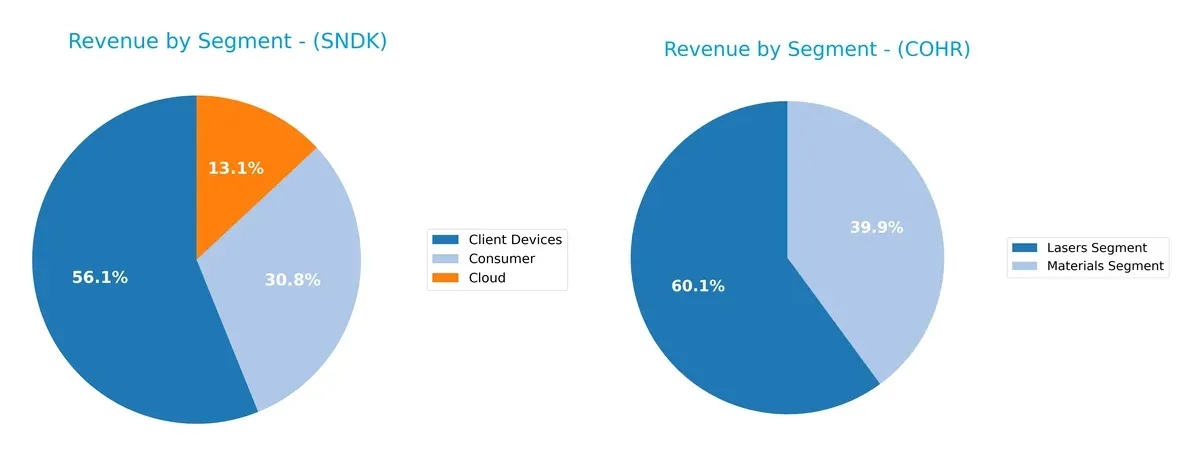

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how Sandisk Corporation and Coherent, Inc. diversify their income streams and highlights their primary sector bets:

Sandisk anchors its revenue with $4.13B from Client Devices, supported by $2.27B Consumer and $960M Cloud segments, showing moderate diversification. Coherent pivots mainly on its Lasers Segment with $1.43B, while Materials contribute $954M, revealing a more balanced two-segment split. Sandisk’s concentration in Client Devices hints at ecosystem lock-in risk, whereas Coherent’s segmentation suggests infrastructure dominance with less exposure to a single market.

Strengths and Weaknesses Comparison

This table compares the Strengths and Weaknesses of Sandisk Corporation and Coherent, Inc.:

Sandisk Corporation Strengths

- Strong diversification with Client Devices, Cloud, and Consumer segments

- Solid global presence including China, US, EMEA, and Asia

- Favorable quick ratio and low debt-to-assets ratio

- Efficient fixed asset turnover ratio

Coherent, Inc. Strengths

- Diversified revenue from Lasers and Materials segments

- Strong presence in North America and Europe

- Favorable current and quick ratios with manageable debt levels

- Positive interest coverage ratio and favorable fixed asset turnover

Sandisk Corporation Weaknesses

- Negative profitability metrics with net margin, ROE, and ROIC all unfavorable

- High WACC exceeding ROIC, indicating value destruction

- Unfavorable interest coverage and no dividend yield

- Slightly unfavorable global ratios overall

Coherent, Inc. Weaknesses

- Low profitability with net margin, ROE, and ROIC near zero and unfavorable

- High price-to-earnings ratio suggesting overvaluation

- Unfavorable asset turnover and low dividend yield

- Slightly unfavorable global ratios overall

Both companies show diversified revenue streams and solid geographic footprints. However, profitability challenges and financial efficiency are key weaknesses that may impact their strategic options.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only shield that protects long-term profits from relentless competitive erosion. Let’s dissect the moats of two industry players:

Sandisk Corporation: Cost Advantage in NAND Flash Storage

Sandisk’s moat stems from its cost leadership in NAND flash technology, reflected in solid gross margins near 30%. However, its declining ROIC signals weakening efficient capital use in 2026, threatening margin stability.

Coherent, Inc.: Technological Intangibles in Laser Systems

Coherent’s moat is built on proprietary laser technologies and precision optics, delivering higher gross margins above 35%. Despite a shrinking ROIC, its revenue and EBIT growth exhibit resilient positioning and expansion potential in industrial applications.

Verdict: Cost Advantage vs. Technological Intangibles

Both firms face declining ROICs, signaling value destruction. Yet, Coherent’s stronger margin profile and operational growth hint at a deeper moat. I see Coherent better equipped to defend market share amid competitive pressures in 2026.

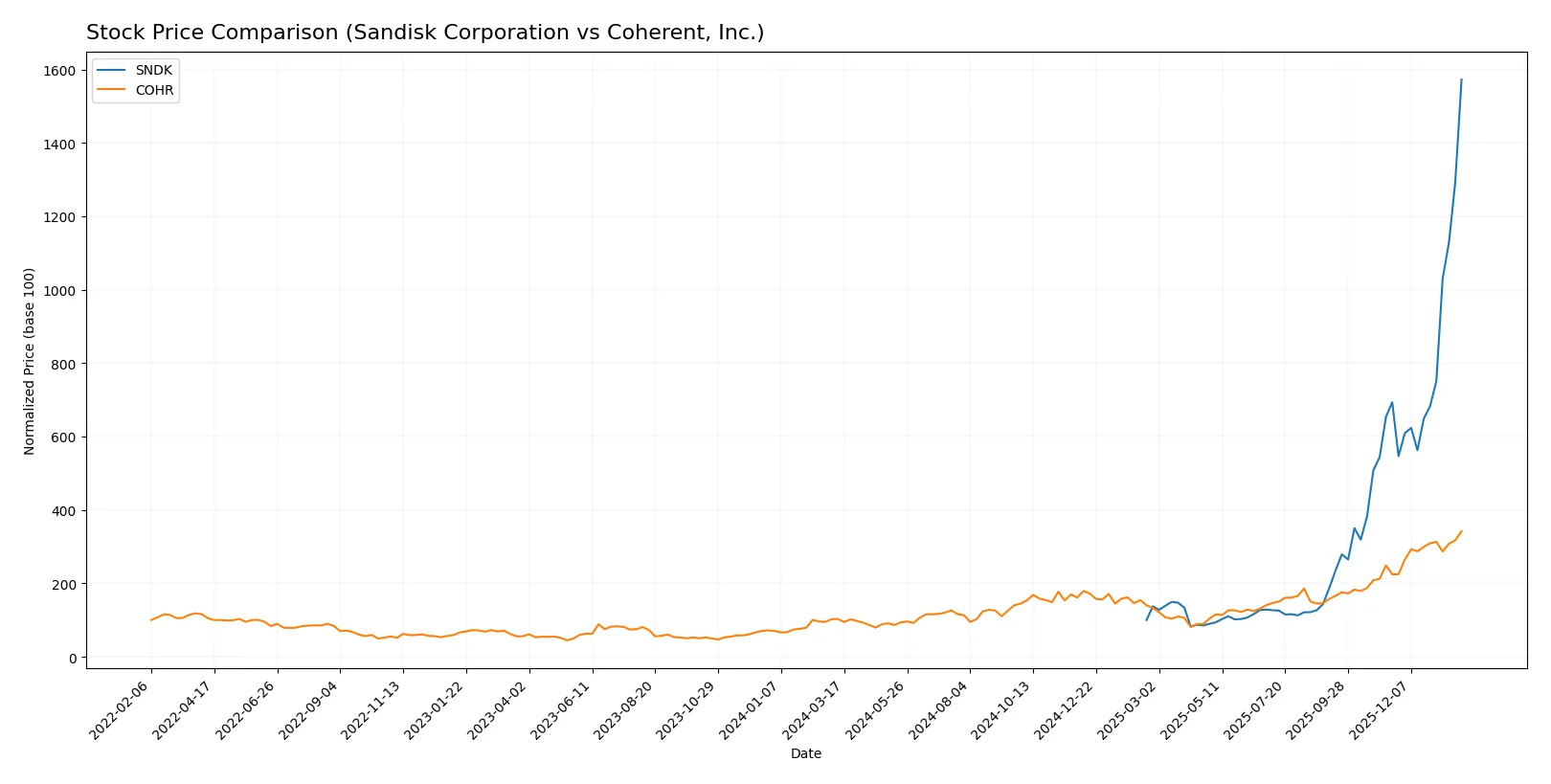

Which stock offers better returns?

The past year shows strong bullish momentum for both stocks, with Sandisk Corporation exhibiting a notably sharper price surge and pronounced buyer dominance compared to Coherent, Inc.

Trend Comparison

Sandisk Corporation’s stock soared 1472.31% over the past 12 months, showing acceleration and high volatility with a peak at 576.25 and a low near 30.11. Recent months confirm sustained bullish momentum.

Coherent, Inc. gained 232.26% over the same period, also accelerating but with lower volatility and a high of 212.18 against a low of 49.26. Recent trend remains positive but less steep than Sandisk’s.

Sandisk’s stock outperformed Coherent’s significantly, delivering superior market returns and stronger buyer dominance throughout the analyzed period.

Target Prices

Analysts present a mixed but generally optimistic target consensus for Sandisk Corporation and Coherent, Inc.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Sandisk Corporation | 220 | 1000 | 614.62 |

| Coherent, Inc. | 190 | 235 | 210 |

Sandisk’s consensus target of 615 exceeds its current price of 576, indicating moderate upside. Coherent’s target aligns closely with its 212 price, suggesting a balanced risk-reward outlook.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

The following tables summarize recent institutional grades for Sandisk Corporation and Coherent, Inc.:

Sandisk Corporation Grades

This table shows the latest grades from major financial institutions for Sandisk Corporation.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Jefferies | maintain | Buy | 2026-01-30 |

| RBC Capital | maintain | Sector Perform | 2026-01-30 |

| Goldman Sachs | maintain | Buy | 2026-01-30 |

| Morgan Stanley | maintain | Overweight | 2026-01-30 |

| Cantor Fitzgerald | maintain | Overweight | 2026-01-30 |

| Wedbush | maintain | Outperform | 2026-01-30 |

| Citigroup | maintain | Buy | 2026-01-20 |

| Wells Fargo | maintain | Equal Weight | 2026-01-15 |

| Benchmark | maintain | Buy | 2026-01-15 |

| Bernstein | maintain | Outperform | 2026-01-14 |

Coherent, Inc. Grades

This table shows the latest grades from major financial institutions for Coherent, Inc.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Morgan Stanley | maintain | Equal Weight | 2026-01-30 |

| Citigroup | maintain | Buy | 2026-01-26 |

| Susquehanna | maintain | Positive | 2026-01-22 |

| Stifel | maintain | Buy | 2026-01-22 |

| Barclays | maintain | Overweight | 2026-01-15 |

| Morgan Stanley | maintain | Equal Weight | 2025-12-17 |

| JP Morgan | maintain | Overweight | 2025-12-05 |

| Barclays | maintain | Overweight | 2025-11-07 |

| Needham | maintain | Buy | 2025-11-06 |

| Morgan Stanley | maintain | Equal Weight | 2025-11-06 |

Which company has the best grades?

Sandisk Corporation has consistently received stronger grades, including multiple “Buy” and “Outperform” ratings. Coherent, Inc. shows more “Equal Weight” and “Overweight” ratings with fewer “Buy” grades. This suggests Sandisk is viewed more favorably, potentially indicating higher confidence from analysts.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

Sandisk Corporation

- Faces fierce competition in NAND flash storage, pressuring margins and innovation cycles.

Coherent, Inc.

- Operates in niche laser tech markets but competes with diversified OEM suppliers and emerging tech startups.

2. Capital Structure & Debt

Sandisk Corporation

- Low debt-to-equity (0.22) supports financial flexibility; however, negative interest coverage signals distress servicing debt.

Coherent, Inc.

- Higher leverage (0.48 DE ratio) but maintains positive interest coverage, reflecting manageable debt risk.

3. Stock Volatility

Sandisk Corporation

- Extremely high beta (4.89) indicates significant stock price swings, increasing investor risk exposure.

Coherent, Inc.

- More moderate beta (1.83) suggests relatively stable stock price movements amid market fluctuations.

4. Regulatory & Legal

Sandisk Corporation

- Subject to technology export controls and IP litigation risks in semiconductor space.

Coherent, Inc.

- Faces regulatory scrutiny in optics and laser exports; potential liability from complex product certifications.

5. Supply Chain & Operations

Sandisk Corporation

- Sensitive to raw material shortages and global semiconductor supply chain disruptions.

Coherent, Inc.

- Dependent on specialty components with exposure to supply bottlenecks in precision optics manufacturing.

6. ESG & Climate Transition

Sandisk Corporation

- Pressure to reduce energy intensity in manufacturing NAND flash; emerging regulatory ESG demands.

Coherent, Inc.

- Faces challenges reducing carbon footprint in laser production; adapting to stricter environmental regulations is ongoing.

7. Geopolitical Exposure

Sandisk Corporation

- Vulnerable to US-China tech tensions impacting supply chains and market access.

Coherent, Inc.

- Exposure to global trade tensions but diversified international sales partly mitigate geopolitical risks.

Which company shows a better risk-adjusted profile?

Sandisk’s biggest risk is its volatile stock price, which amplifies market uncertainty. Coherent’s chief concern lies in its moderate leverage and profitability struggles. Despite Sandisk’s higher beta, Coherent’s weaker profitability and elevated valuation multiples limit its margin of safety. I see Coherent as having a slightly better risk-adjusted profile, bolstered by a stronger Altman Z-score and Piotroski score, reflecting more financial resilience despite operational challenges.

Final Verdict: Which stock to choose?

Sandisk Corporation’s superpower lies in its robust liquidity and ability to maintain operational efficiency despite profitability challenges. Its key point of vigilance is declining returns on invested capital, signaling value destruction risks. Sandisk might suit investors with an appetite for aggressive growth and turnaround potential.

Coherent, Inc. leverages a strategic moat in its specialized technology niche, benefiting from steady recurring revenues and solid cash flow management. It offers a comparatively safer profile with stronger profitability trends and healthier financial scores. Coherent could align well with GARP investors seeking growth tempered by reasonable valuation.

If you prioritize aggressive growth with a tolerance for operational volatility, Sandisk’s liquidity strength and market momentum make it a compelling scenario. However, if you seek stability and a proven strategic moat, Coherent offers better financial health and sustainability, though it commands a premium valuation. Both present distinct risk-reward profiles requiring careful alignment with your investment strategy.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Sandisk Corporation and Coherent, Inc. to enhance your investment decisions: