Home > Comparison > Technology > CTSH vs DXC

The strategic rivalry between Cognizant Technology Solutions Corporation and DXC Technology Company shapes the Information Technology Services sector’s evolution. Cognizant operates as a diversified technology and consulting powerhouse, while DXC focuses on integrated business and infrastructure services. This head-to-head highlights a contest between broad digital transformation expertise and specialized cloud infrastructure management. This analysis will identify which trajectory offers superior risk-adjusted returns for a balanced, diversified portfolio.

Table of contents

Companies Overview

Cognizant and DXC Technology command major roles in the global IT services market with distinct strategic approaches.

Cognizant Technology Solutions Corporation: Digital Transformation Leader

Cognizant dominates as a professional services firm delivering consulting and outsourcing services across Financial Services, Healthcare, Products, and Communications sectors. Its revenue stems from advanced technology solutions like robotic process automation and AI to enhance customer experience and operational efficiency. In 2026, Cognizant focuses on expanding digital health services and integrated omni-channel experiences to meet evolving client demands.

DXC Technology Company: IT Infrastructure and Analytics Provider

DXC specializes in IT services and solutions through its Global Business Services and Global Infrastructure Services segments. It generates revenue by offering analytics, consulting, cloud migration, and security solutions that accelerate digital transformation. DXC’s 2026 strategy centers on modernizing legacy systems and enhancing secure multi-cloud environments to reduce clients’ operational risks and costs.

Strategic Collision: Similarities & Divergences

Both companies emphasize digital transformation but differ in execution. Cognizant invests heavily in customer-centric, outcome-based services, while DXC prioritizes infrastructure modernization and security. They primarily compete in enterprise IT services, targeting overlapping but distinct client needs. Cognizant’s broad service scope contrasts with DXC’s infrastructure focus, shaping unique investment profiles driven by growth potential versus operational resilience.

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Cognizant Technology Solutions Corporation (CTSH) | DXC Technology Company (DXC) |

|---|---|---|

| Revenue | 21.1B | 12.9B |

| Cost of Revenue | 14.0B | 9.8B |

| Operating Expenses | 3.6B | 2.4B |

| Gross Profit | 7.1B | 3.1B |

| EBITDA | 4.2B | 2.2B |

| EBIT | 3.6B | 895M |

| Interest Expense | 37M | 265M |

| Net Income | 2.2B | 389M |

| EPS | 4.56 | 2.15 |

| Fiscal Year | 2025 | 2025 |

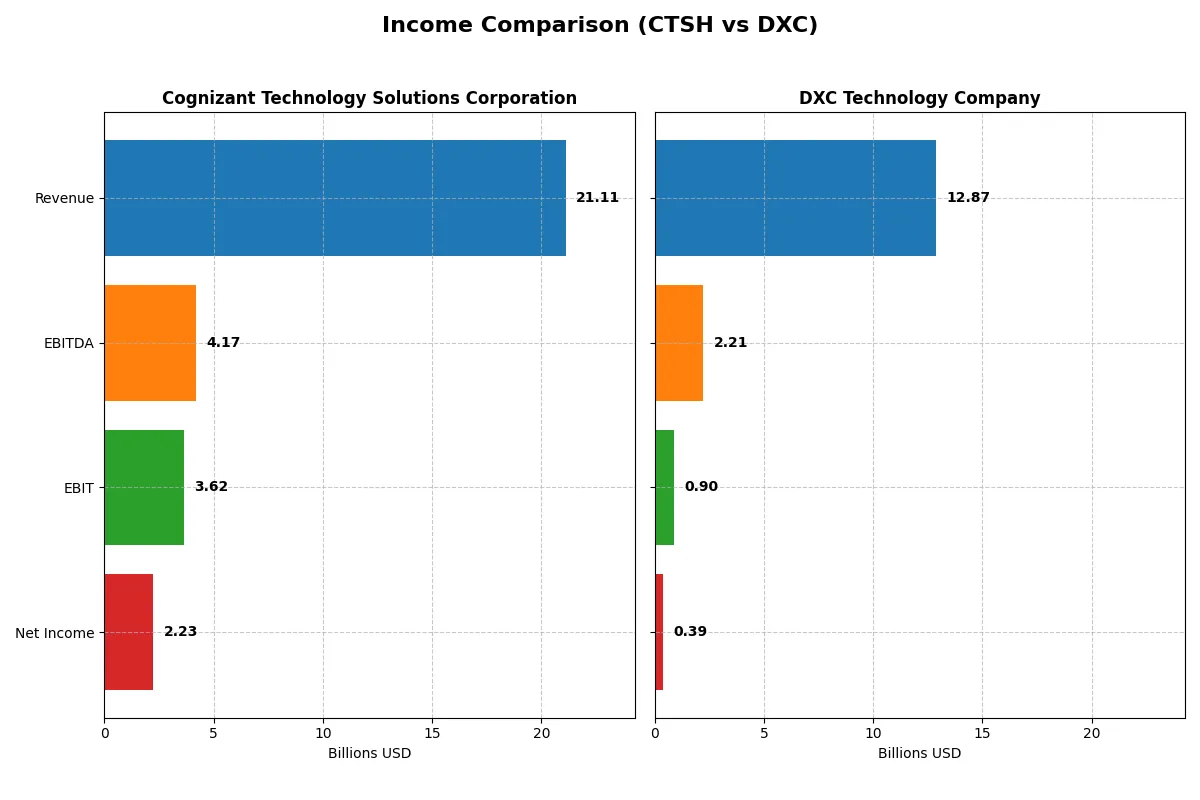

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals which company runs a more efficient and profitable business engine in today’s market environment.

Cognizant Technology Solutions Corporation Analysis

Cognizant’s revenue expanded steadily from 18.5B in 2021 to 21.1B in 2025, reflecting consistent top-line growth. Net income showed moderate improvement, reaching 2.23B in 2025 despite a slight margin contraction. Gross margin remains robust at 33.7%, and EBIT margin strengthened to 17.2%, signaling solid operational efficiency and strong cost control.

DXC Technology Company Analysis

DXC’s revenue declined from 16.3B in 2021 to 12.9B in 2025, showing top-line pressure. However, net income rebounded sharply from a loss in 2023 to 389M in 2025. Gross margin held steady near 24%, but EBIT margin only reached 7.0%, reflecting weaker profitability. The recent earnings momentum suggests a turnaround but from a much lower base.

Margin Strength vs. Recovery Momentum

Cognizant demonstrates superior margin power and consistent growth, with healthy profitability metrics well above industry benchmarks. DXC shows promising earnings recovery but struggles with shrinking revenue and lower margins. For investors, Cognizant’s profile offers a more reliable income statement foundation, while DXC presents a higher-risk turnaround story.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | Cognizant Technology Solutions Corporation (CTSH) | DXC Technology Company (DXC) |

|---|---|---|

| ROE | 14.9% | 12.0% |

| ROIC | 12.3% | 4.4% |

| P/E | 17.9 | 7.9 |

| P/B | 2.66 | 0.95 |

| Current Ratio | 2.34 | 1.22 |

| Quick Ratio | 2.34 | 1.22 |

| D/E | 0.105 | 1.41 |

| Debt-to-Assets | 7.6% | 34.4% |

| Interest Coverage | 95.4 | 2.63 |

| Asset Turnover | 1.02 | 0.97 |

| Fixed Asset Turnover | 14.0 | 6.82 |

| Payout ratio | 27.4% | 0% |

| Dividend yield | 1.53% | 0% |

| Fiscal Year | 2025 | 2025 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios serve as the company’s DNA, unveiling hidden risks and operational excellence critical for investment decisions.

Cognizant Technology Solutions Corporation

Cognizant displays solid profitability with a 14.85% ROE and a favorable 10.56% net margin, signaling operational strength. Valuation metrics like a 17.9 P/E and 2.66 P/B ratio paint a neutral picture, neither cheap nor stretched. The firm rewards shareholders with a 1.53% dividend yield, reflecting balanced capital allocation between returns and growth.

DXC Technology Company

DXC shows weaker profitability, with a 12.05% ROE and a low 3.02% net margin, indicating operational challenges. Its valuation appears attractive, with a 7.92 P/E and 0.95 P/B, suggesting the stock is undervalued. However, DXC pays no dividends and carries higher leverage, pointing to elevated financial risk and limited shareholder payouts.

Balanced Strength vs. Value Opportunity

Cognizant offers a stronger operational profile with favorable profitability and stable shareholder returns. DXC trades at a discount but carries higher risks and weaker margins. Investors seeking stability may prefer Cognizant, while those chasing value may consider DXC’s lower valuation despite its financial challenges.

Which one offers the Superior Shareholder Reward?

I observe that Cognizant Technology Solutions Corporation (CTSH) offers a consistent dividend yield around 1.5% with a sustainable payout ratio near 27%. It covers dividends well with strong free cash flow (FCF) of 5.4/share in 2025. CTSH pairs dividends with moderate buybacks, supporting total returns. In contrast, DXC Technology Company (DXC) pays no dividend, relying on reinvestment and buybacks. However, DXC’s high debt leverage (debt/equity ~1.4) and thin net margin (~3%) raise sustainability concerns. Its free cash flow per share (4.5) is solid but partly consumed by heavy capex (3.2/share). I conclude CTSH’s balanced payout and buyback combination delivers a superior, more sustainable shareholder reward in 2026.

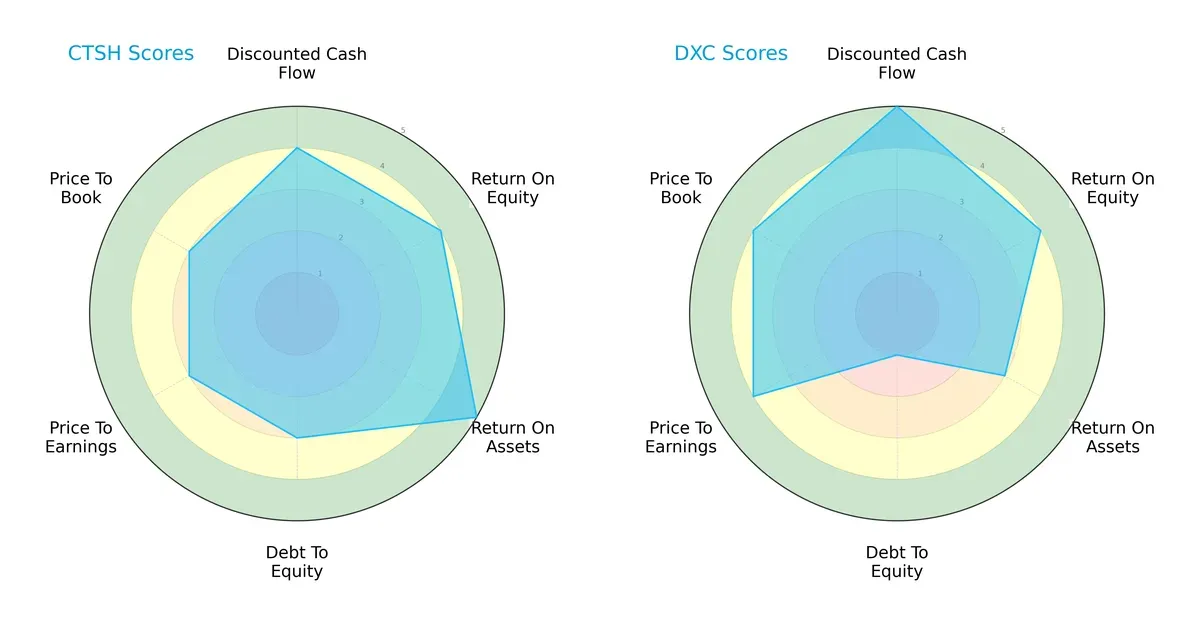

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Cognizant Technology Solutions and DXC Technology Company, highlighting their operational and financial strengths:

Cognizant shows a balanced profile with solid DCF (4), ROE (4), and an impressive ROA (5), reflecting efficient asset use. DXC leads in DCF (5) and valuation metrics (PE 4, PB 4) but suffers a severe weakness in debt-to-equity (1), signaling risky leverage. Cognizant’s moderate debt score (3) provides a more stable financial footing. Overall, Cognizant relies on operational efficiency, while DXC leverages valuation and cash flow advantages with higher financial risk.

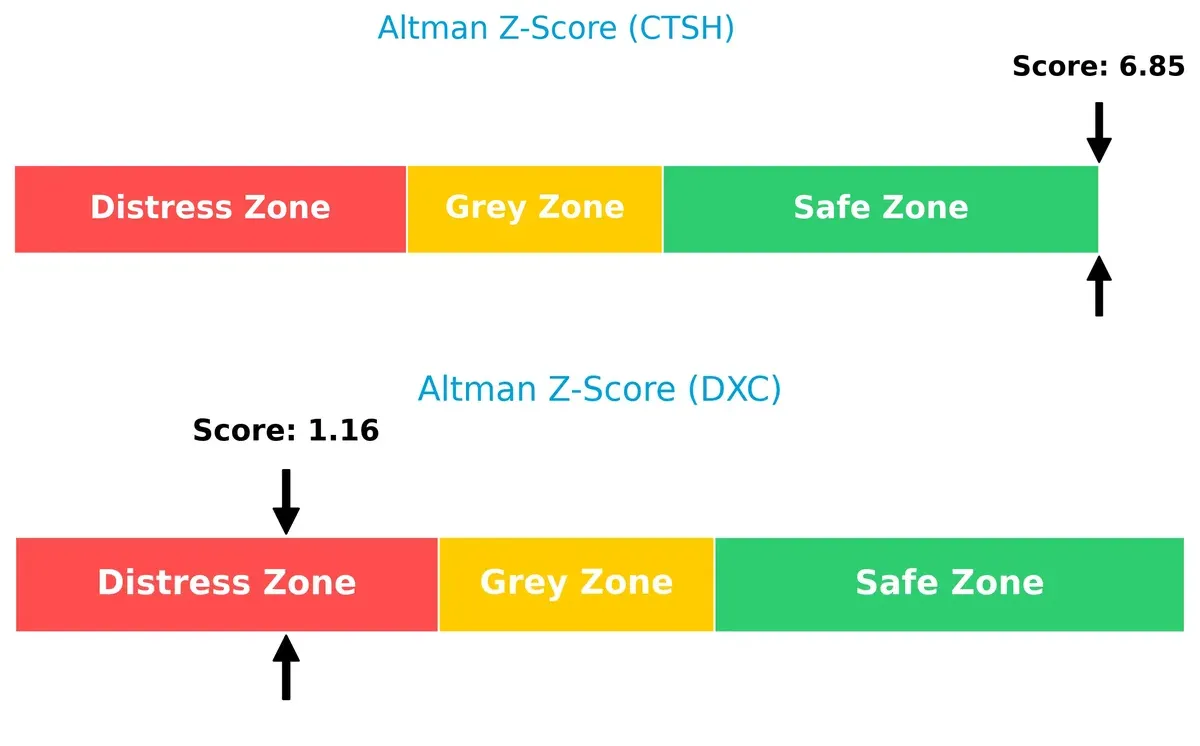

Bankruptcy Risk: Solvency Showdown

The Altman Z-Score gap sharply contrasts the firms’ bankruptcy risk in this cycle:

Cognizant’s robust Z-Score of 6.85 places it securely in the safe zone, signaling strong solvency and a low bankruptcy risk. DXC’s 1.16 falls into the distress zone, raising red flags about its long-term survival amid economic headwinds. This disparity underscores Cognizant’s superior balance sheet resilience versus DXC’s precarious financial health.

Financial Health: Quality of Operations

Both firms share a Piotroski F-Score of 7, indicating strong financial health:

A score of 7 suggests both companies maintain solid profitability, liquidity, and operational efficiency. Neither displays internal red flags, but this parity contrasts with their divergent solvency profiles, reminding investors to weigh quality alongside risk exposure.

How are the two companies positioned?

This section dissects the operational DNA of CTSH and DXC by comparing their revenue distribution by segment and internal dynamics. The goal is to confront their economic moats and identify the more resilient, sustainable competitive advantage in today’s market.

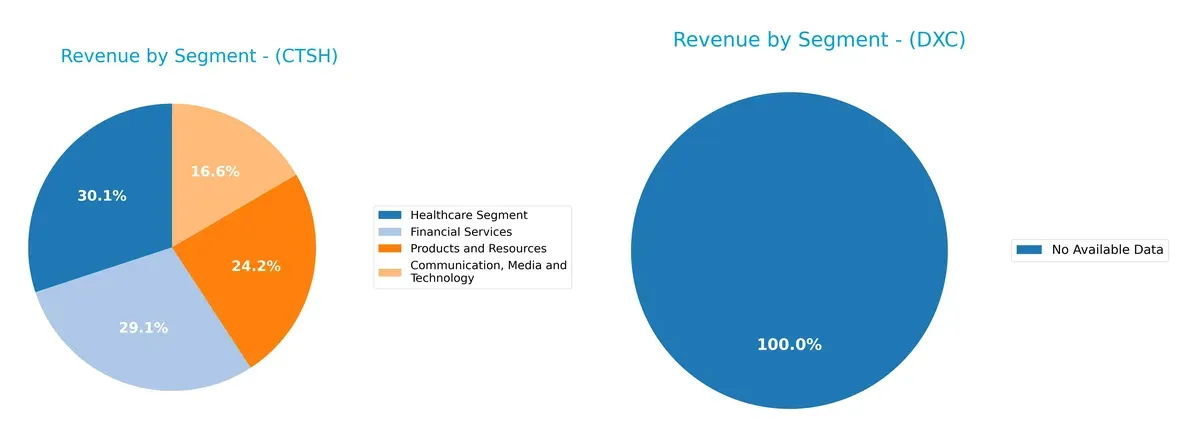

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how Cognizant Technology Solutions Corporation and DXC Technology Company diversify their income streams and where their primary sector bets lie:

Cognizant shows a well-diversified revenue base with strong contributions from Healthcare ($5.9B), Financial Services ($5.7B), Products and Resources ($4.8B), and Communication, Media and Technology ($3.3B). DXC lacks reported segment data, preventing a direct comparison. Cognizant’s broad mix reduces concentration risk and signals a strategic pivot towards ecosystem lock-in across multiple sectors. This multi-industry exposure contrasts with firms reliant on single dominant segments.

Strengths and Weaknesses Comparison

This table compares the Strengths and Weaknesses of Cognizant Technology Solutions Corporation and DXC Technology Company:

CTSH Strengths

- Diversified revenue across four key segments

- Favorable net margin at 10.56%

- Strong liquidity with current and quick ratios at 2.34

- Low debt-to-equity ratio of 0.1 indicates conservative leverage

- High asset turnover efficiency at 1.02 and fixed asset turnover at 14.02

- Global footprint with $14.7B North America and $5.7B Europe revenue

DXC Strengths

- Favorable WACC at 5.8% supports cost-effective capital

- Attractive valuation with PE at 7.92 and PB below 1

- Favorable quick ratio at 1.22 shows adequate liquidity

- Moderate fixed asset turnover at 6.82 indicates operational use of assets

- Neutral interest coverage of 3.38 maintains debt service ability

CTSH Weaknesses

- Neutral ROE at 14.85% suggests moderate shareholder returns

- Neutral PE and PB may indicate market pricing in growth

- Dividend yield neutral at 1.53% limits income appeal

- No significant weaknesses from leverage or liquidity

DXC Weaknesses

- Unfavorable net margin at 3.02% signals low profitability

- Weak ROIC at 4.43% below its WACC indicates poor capital returns

- High debt-to-equity ratio of 1.41 raises financial risk

- Zero dividend yield may deter income-seeking investors

- Neutral to unfavorable liquidity and interest coverage ratios

Both companies show distinct profiles: CTSH demonstrates stronger profitability, liquidity, and diversification, supporting its global strategy. DXC’s valuation and capital cost advantages contrast with its profitability and leverage challenges, impacting its financial flexibility.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the essential barrier that preserves long-term profits from relentless competitive pressure. Let’s dissect the moats of two IT services giants:

Cognizant Technology Solutions Corporation: Intangible Assets and Client Relationships

Cognizant’s moat primarily stems from deep client relationships and specialized consulting expertise. This manifests in stable margins (17% EBIT) and consistent ROIC above WACC, despite a recent decline. Expansion into AI and digital health should reinforce its moat in 2026.

DXC Technology Company: Cost Efficiency and Partner Ecosystem

DXC relies on cost advantages and a broad partner ecosystem to compete, contrasting with Cognizant’s relationship focus. However, DXC’s ROIC trails WACC, signaling value destruction. Its 2026 outlook hinges on cloud migration success and infrastructure services growth to regain footing.

Client Intimacy vs. Cost Leadership: The Moat Showdown

Cognizant’s intangible asset moat is deeper and more sustainable, supported by positive value creation and margin stability. DXC’s weaker, cost-driven moat struggles with declining profitability. Cognizant is better positioned to defend market share amid intensifying competition.

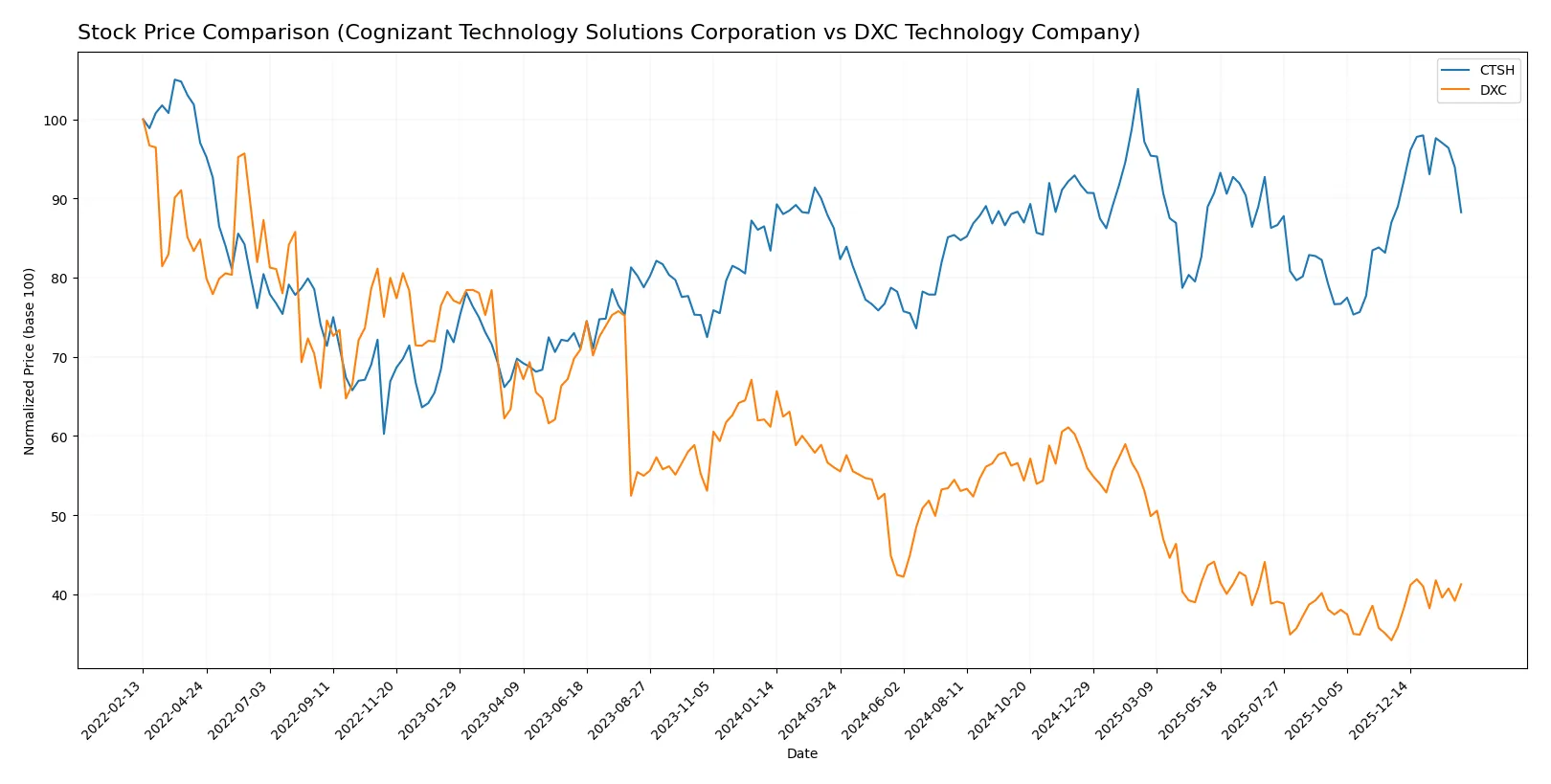

Which stock offers better returns?

The past year witnessed divergent price movements: Cognizant Technology Solutions gained 2.32% with accelerating momentum, while DXC Technology dropped 26.36% despite recent rebound signs.

Trend Comparison

Cognizant’s stock rose 2.32% over the last 12 months, marking a bullish trend with acceleration. The price ranged between 64.26 and 90.7, reflecting moderate volatility (5.77 std deviation).

DXC’s stock declined 26.36% over the same period, indicating a bearish trend with accelerating losses. Prices fluctuated from 12.59 to 22.5, with lower volatility (2.99 std deviation).

Cognizant outperformed DXC, delivering the highest market return during the year despite DXC’s recent 20.73% short-term rebound.

Target Prices

Analysts expect moderate upside for Cognizant Technology Solutions and limited gains for DXC Technology.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Cognizant Technology Solutions Corporation | 82 | 107 | 93.2 |

| DXC Technology Company | 13 | 14 | 13.5 |

Cognizant’s consensus target of $93.2 implies a 21% potential rise from the current $77.08 price. DXC’s target at $13.5 suggests a modest pullback from its $15.2 market price.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Cognizant Technology Solutions Corporation Grades

The table below summarizes recent institutional grades for Cognizant Technology Solutions Corporation:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| TD Cowen | Maintain | Hold | 2026-02-05 |

| Morgan Stanley | Maintain | Equal Weight | 2026-02-05 |

| RBC Capital | Maintain | Sector Perform | 2026-02-05 |

| Guggenheim | Maintain | Buy | 2026-01-28 |

| Citigroup | Maintain | Neutral | 2026-01-22 |

| Wells Fargo | Maintain | Overweight | 2026-01-14 |

| TD Cowen | Maintain | Hold | 2026-01-09 |

| UBS | Maintain | Neutral | 2025-12-08 |

| William Blair | Upgrade | Outperform | 2025-11-21 |

| UBS | Maintain | Neutral | 2025-10-30 |

DXC Technology Company Grades

The table below summarizes recent institutional grades for DXC Technology Company:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| BMO Capital | Maintain | Market Perform | 2026-02-03 |

| Stifel | Maintain | Hold | 2025-10-31 |

| JP Morgan | Maintain | Underweight | 2025-08-20 |

| Morgan Stanley | Maintain | Equal Weight | 2025-08-01 |

| RBC Capital | Maintain | Sector Perform | 2025-08-01 |

| JP Morgan | Maintain | Underweight | 2025-05-21 |

| RBC Capital | Maintain | Sector Perform | 2025-05-15 |

| BMO Capital | Maintain | Market Perform | 2025-05-15 |

| Morgan Stanley | Maintain | Equal Weight | 2025-05-15 |

| Guggenheim | Maintain | Neutral | 2025-05-12 |

Which company has the best grades?

Cognizant Technology Solutions holds generally stronger grades, including Buy and Outperform ratings. DXC Technology mostly receives Hold or Market Perform grades. Investors may perceive Cognizant as having more favorable analyst sentiment.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

Cognizant Technology Solutions Corporation (CTSH)

- Strong market position with diversified segments and stable margins.

DXC Technology Company (DXC)

- Smaller market cap and lower margins increase vulnerability to competitive pressures.

2. Capital Structure & Debt

CTSH

- Low debt-to-equity (0.1), strong interest coverage (97.92), signaling robust financial stability.

DXC

- High debt-to-equity (1.41) and moderate interest coverage (3.38) pose financial risk.

3. Stock Volatility

CTSH

- Beta below 1 (0.957) indicates moderate market sensitivity and lower volatility.

DXC

- Beta above 1 (1.083) implies higher stock volatility and risk exposure.

4. Regulatory & Legal

CTSH

- Operates globally with exposure to evolving data privacy and outsourcing regulations.

DXC

- Similar global exposure with additional risk in infrastructure services subject to compliance costs.

5. Supply Chain & Operations

CTSH

- Extensive global operations with strong asset turnover (1.02) and efficient fixed asset use (14.02).

DXC

- Moderate asset turnover (0.97), but high operational leverage in legacy system migrations adds complexity.

6. ESG & Climate Transition

CTSH

- Increasing focus on digital health and AI services, aligning with sustainability trends.

DXC

- Lagging dividend yield and higher debt raise concerns on capital allocation toward ESG initiatives.

7. Geopolitical Exposure

CTSH

- Broad international footprint mitigates country risk but faces geopolitical uncertainties.

DXC

- Similar global footprint with additional risks due to reliance on legacy infrastructure in sensitive regions.

Which company shows a better risk-adjusted profile?

Cognizant faces fewer financial risks with a strong balance sheet, lower leverage, and better operational efficiency. DXC’s higher debt and lower margins increase vulnerability despite favorable valuation metrics. The Altman Z-score confirms Cognizant’s safer financial position, while DXC remains in distress territory. Cognizant’s prudent capital structure and stable margins make it the safer, more risk-adjusted choice in 2026.

Final Verdict: Which stock to choose?

Cognizant Technology Solutions Corporation (CTSH) stands out for its robust capital efficiency and consistent value creation. Its superpower lies in delivering solid returns on invested capital well above its cost of capital, reflecting disciplined capital allocation. The main point of vigilance is its gradually declining ROIC trend, which could signal emerging competitive pressures. CTSH fits well in portfolios targeting steady growth with moderate risk tolerance.

DXC Technology Company (DXC) offers an intriguing value proposition through its low valuation multiples and significant free cash flow yield. Its strategic moat is weaker, reflected in negative economic value creation and high leverage, implying a higher risk profile. However, its recent operational improvements and attractive price metrics may appeal to investors seeking turnaround potential and value exposure with higher risk appetite.

If you prioritize consistent economic value creation and financial stability, CTSH outshines with its disciplined capital use despite slowing profitability. However, if you seek contrarian value plays with potential upside from restructuring, DXC offers better stability in free cash flow yield and compelling valuation metrics but commands a premium in risk tolerance. Each stock aligns with distinct investor profiles, emphasizing the importance of matching strategy to risk appetite.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Cognizant Technology Solutions Corporation and DXC Technology Company to enhance your investment decisions: