Home > Comparison > Technology > CRUS vs MXL

The competitive dynamic between Cirrus Logic, Inc. and MaxLinear, Inc. shapes the semiconductor industry’s evolution. Cirrus Logic focuses on low-power, high-precision mixed-signal processing, while MaxLinear specializes in RF and high-performance analog SoCs for communication systems. This analysis pits Cirrus’s audio-centric innovation against MaxLinear’s infrastructure-oriented solutions, aiming to identify which path delivers superior risk-adjusted returns for a diversified portfolio in an increasingly connected world.

Table of contents

Companies Overview

Cirrus Logic and MaxLinear shape key niches within the semiconductor industry, driving innovation in mixed-signal processing and communications.

Cirrus Logic, Inc.: Leader in Mixed-Signal Audio Solutions

Cirrus Logic dominates low-power, high-precision mixed-signal processing. It earns primarily from audio-related codecs, amplifiers, and digital signal processors powering smartphones, AR/VR, and automotive systems. In 2026, its strategy centers on expanding SoundClear technology, enhancing user experience with noise cancellation and hearing augmentation, solidifying its competitive edge in premium audio markets.

MaxLinear, Inc.: Innovator in Communications SoCs

MaxLinear specializes in high-performance RF and mixed-signal system-on-chip solutions for wired and wireless infrastructure. Its revenue stems from broadband transceivers, modems, and power management products embedded in 4G/5G networks and home networking devices. The company’s 2026 focus remains on integrating end-to-end communication platforms to support growing demand in fiber-optic and wireless connectivity.

Strategic Collision: Similarities & Divergences

Both firms excel in mixed-signal technology, yet Cirrus Logic targets consumer audio ecosystems while MaxLinear pursues network infrastructure applications. Their battleground lies in delivering integrated, power-efficient chips that balance performance and cost. Investors face distinct profiles: Cirrus Logic leans on consumer-driven innovation, whereas MaxLinear bets on industrial and communication infrastructure growth.

Income Statement Comparison

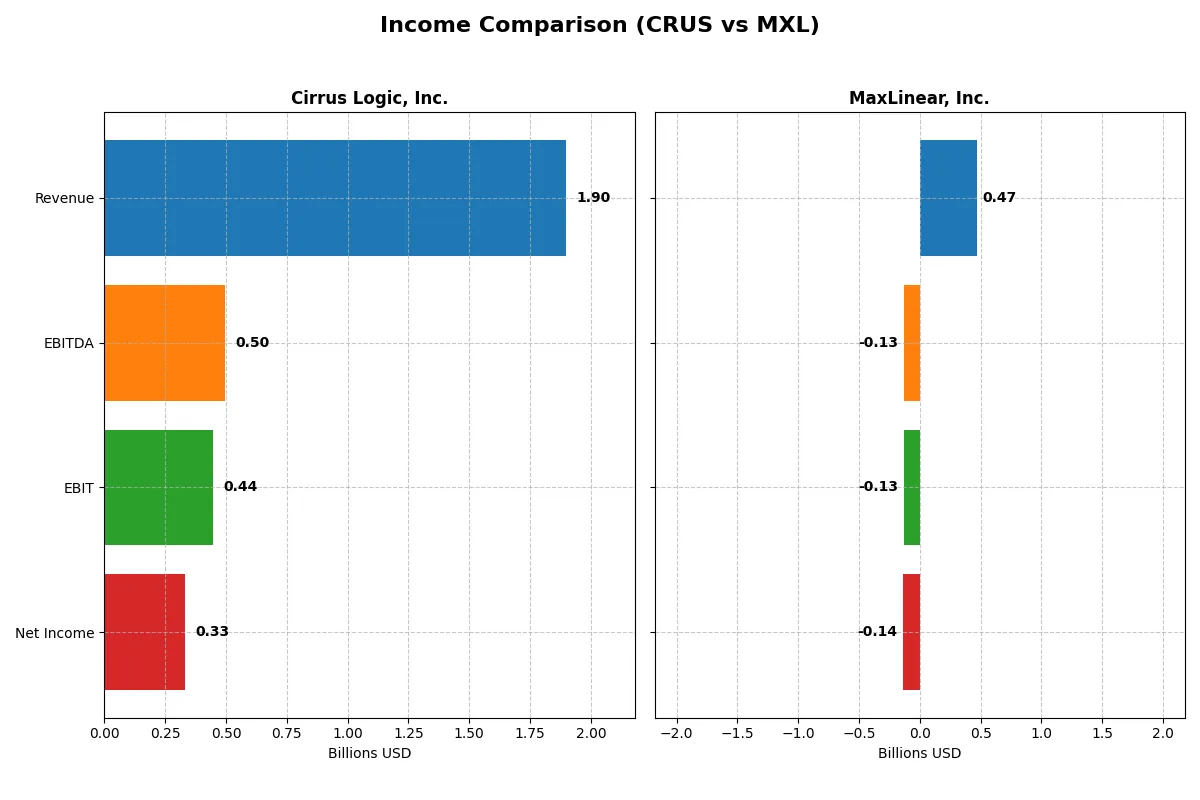

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line in fiscal 2025:

| Metric | Cirrus Logic, Inc. (CRUS) | MaxLinear, Inc. (MXL) |

|---|---|---|

| Revenue | 1.90B | 468M |

| Cost of Revenue | 900M | 202M |

| Operating Expenses | 586M | 393M |

| Gross Profit | 996M | 266M |

| EBITDA | 497M | -131M |

| EBIT | 445M | -131M |

| Interest Expense | 0.9M | 10M |

| Net Income | 332M | -137M |

| EPS | 6.24 | -1.58 |

| Fiscal Year | 2025 | 2025 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals which company converts revenue into profit most efficiently over time.

Cirrus Logic, Inc. Analysis

Cirrus Logic’s revenue climbed steadily from 1.37B in 2021 to 1.90B in 2025, with net income surging 52% overall. Its gross margin remains robust at 52.5%, while net margin improved to 17.5%, reflecting disciplined cost control. The 2025 leap in EBIT by 22% signals growing operational efficiency and momentum.

MaxLinear, Inc. Analysis

MaxLinear’s revenue peaked at 1.12B in 2022 but dropped nearly 48% over five years to 468M in 2025. Despite a strong gross margin near 57%, it posts a negative net margin of -29% due to heavy operating losses. The 2025 net loss narrowed by 57%, showing signs of recovery, yet profitability remains elusive.

Margin Power vs. Revenue Scale

Cirrus Logic outperforms with steady revenue growth and strong net profitability, while MaxLinear struggles with shrinking sales and persistent losses. Cirrus’ consistent margin expansion and positive earnings growth make it the clear fundamental winner. Investors favor companies that combine scale with sustainable profits, highlighting Cirrus’ more attractive profile.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | Cirrus Logic, Inc. (CRUS) | MaxLinear, Inc. (MXL) |

|---|---|---|

| ROE | 17.0% | -47.5% |

| ROIC | 14.2% | -24.3% |

| P/E | 15.9 | -6.7 |

| P/B | 2.71 | 3.20 |

| Current Ratio | 6.35 | 1.77 |

| Quick Ratio | 4.82 | 1.28 |

| D/E | 0.07 | 0.29 |

| Debt-to-Assets | 6.2% | 17.2% |

| Interest Coverage | 457 | -15.5 |

| Asset Turnover | 0.81 | 0.42 |

| Fixed Asset Turnover | 6.62 | 4.65 |

| Payout ratio | 0 | 0 |

| Dividend yield | 0 | 0 |

| Fiscal Year | 2025 | 2024 |

Efficiency & Valuation Duel: The Vital Signs

Ratios act as a company’s DNA, revealing hidden risks and operational excellence through key financial signals.

Cirrus Logic, Inc.

Cirrus Logic demonstrates strong profitability with a 17.01% ROE and a solid 17.48% net margin, reflecting operational efficiency. Its valuation is reasonable, with a P/E of 15.95 and P/B of 2.71, neither stretched nor undervalued. The company reinvests heavily in R&D, supporting future growth, but offers no dividend yield.

MaxLinear, Inc.

MaxLinear struggles with negative profitability metrics, including a -47.49% ROE and a -68.01% net margin, signaling operational challenges. Despite an appealing negative P/E, its valuation is stretched with a P/B of 3.2. The company retains earnings for intense R&D investment, foregoing dividends amid weak cash flow generation.

Precision in Profitability vs. Growth Risk

Cirrus Logic offers a balanced profile with favorable profitability and reasonable valuation, while MaxLinear exhibits significant operational weakness and valuation concerns. Investors prioritizing stable returns and efficiency may lean toward Cirrus, whereas those with a higher risk tolerance seeking turnaround potential might consider MaxLinear.

Which one offers the Superior Shareholder Reward?

Cirrus Logic (CRUS) and MaxLinear (MXL) both forgo dividends, focusing on reinvestment and buybacks. I observe CRUS maintains a zero dividend payout but generates strong free cash flow (7.8/share in 2025) and executes consistent buybacks. Conversely, MXL faces losses and negative free cash flow (-0.75/share in 2024), limiting buybacks. CRUS’s robust cash ratios (cash ratio ~2.76) and low debt (debt/assets ~6%) contrast with MXL’s weaker liquidity and solvency. I conclude CRUS offers superior total shareholder reward through sustainable capital allocation and buybacks, while MXL’s losses and financial strain undermine shareholder returns in 2026.

Comparative Score Analysis: The Strategic Profile

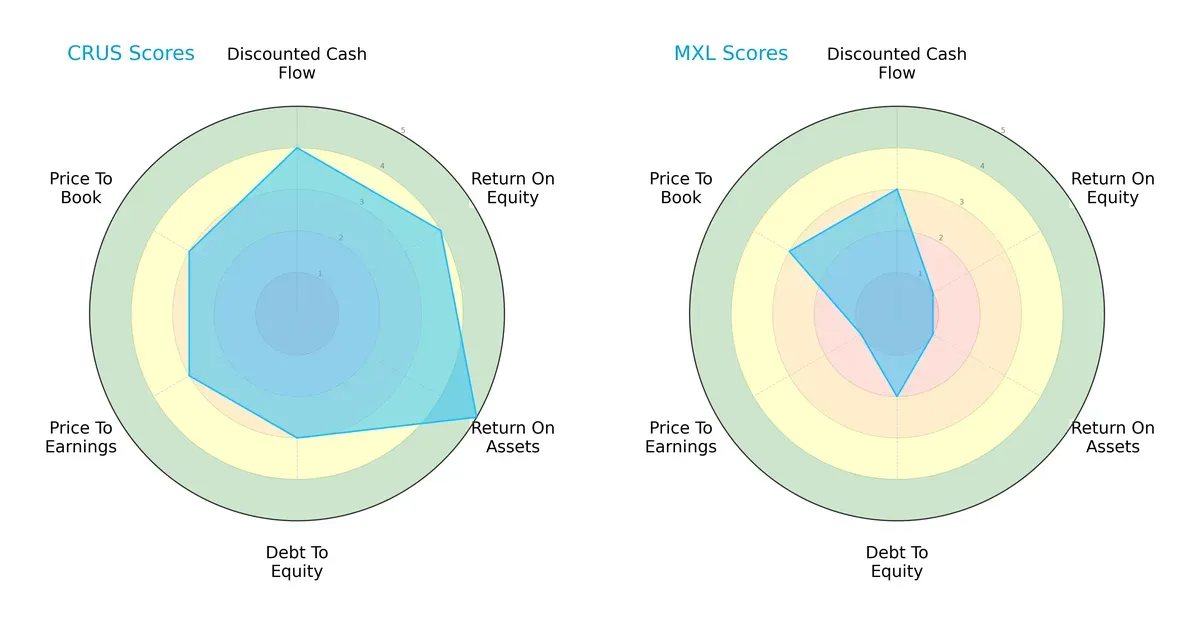

The radar chart reveals the core financial DNA and strategic trade-offs of Cirrus Logic, Inc. and MaxLinear, Inc.:

Cirrus Logic shows a well-rounded profile with strong DCF, ROE, and ROA scores, indicating efficient capital use and profitability. MaxLinear leans heavily on moderate DCF but suffers from weak ROE and ROA, reflecting operational challenges. Cirrus presents a more balanced risk profile, while MaxLinear relies on limited valuation strengths amid financial fragility.

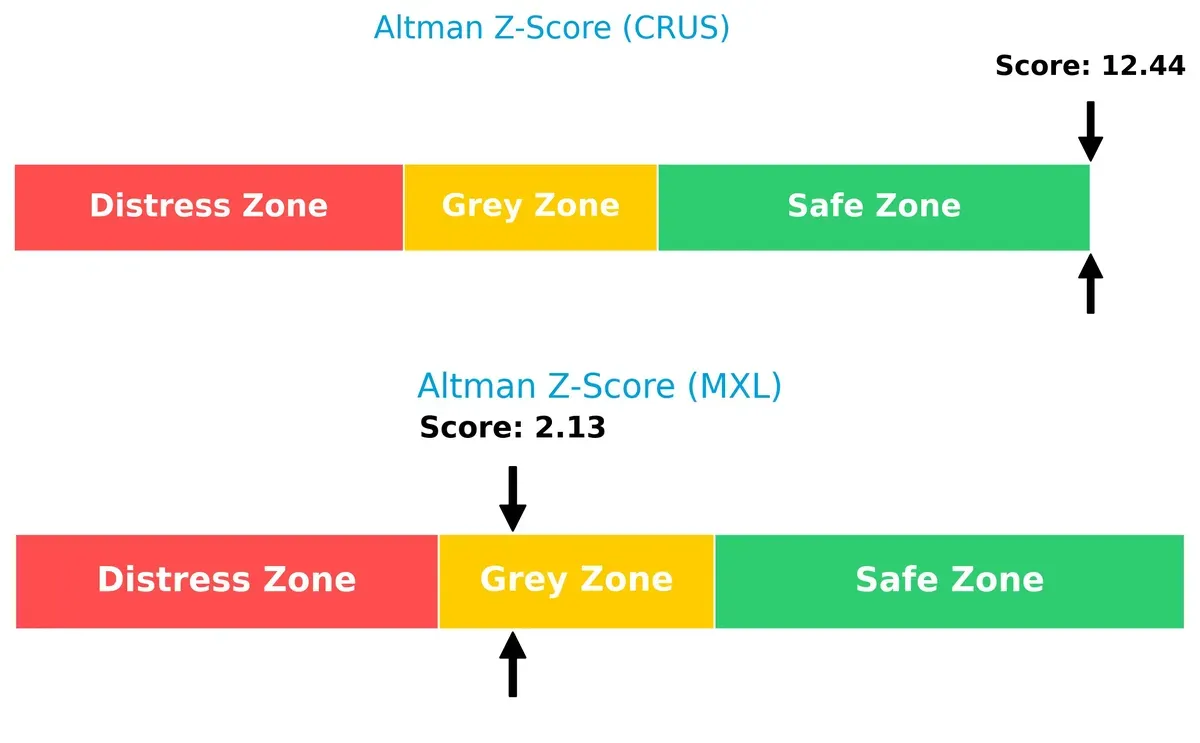

Bankruptcy Risk: Solvency Showdown

Cirrus Logic’s Altman Z-Score of 12.44 places it deep in the safe zone, signaling robust solvency and low bankruptcy risk. MaxLinear’s 2.13 score lands in the grey zone, flagging moderate financial distress risks in this cycle:

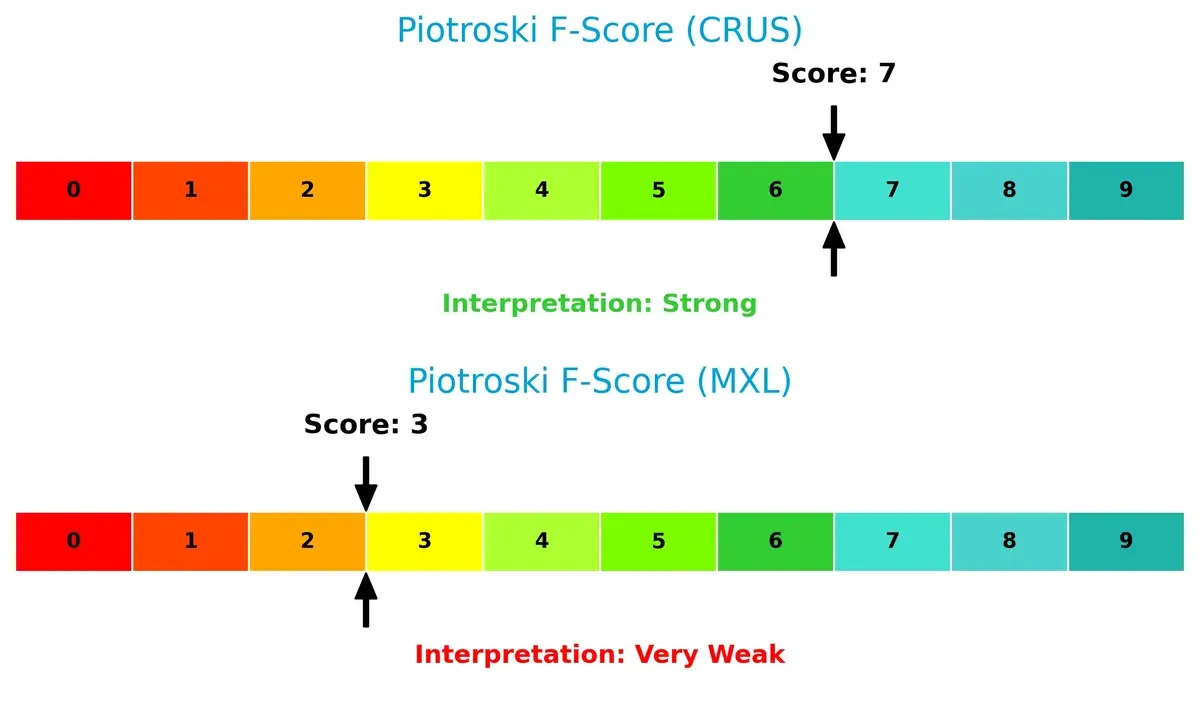

Financial Health: Quality of Operations

Cirrus Logic’s Piotroski F-Score of 7 signals strong financial health and operational quality. MaxLinear’s score of 3 raises red flags, indicating weaker internal metrics and potential financial instability:

How are the two companies positioned?

This section dissects Cirrus Logic and MaxLinear’s operational DNA by comparing their revenue distribution and internal dynamics. It culminates in confronting their economic moats to identify which model offers the most resilient competitive advantage today.

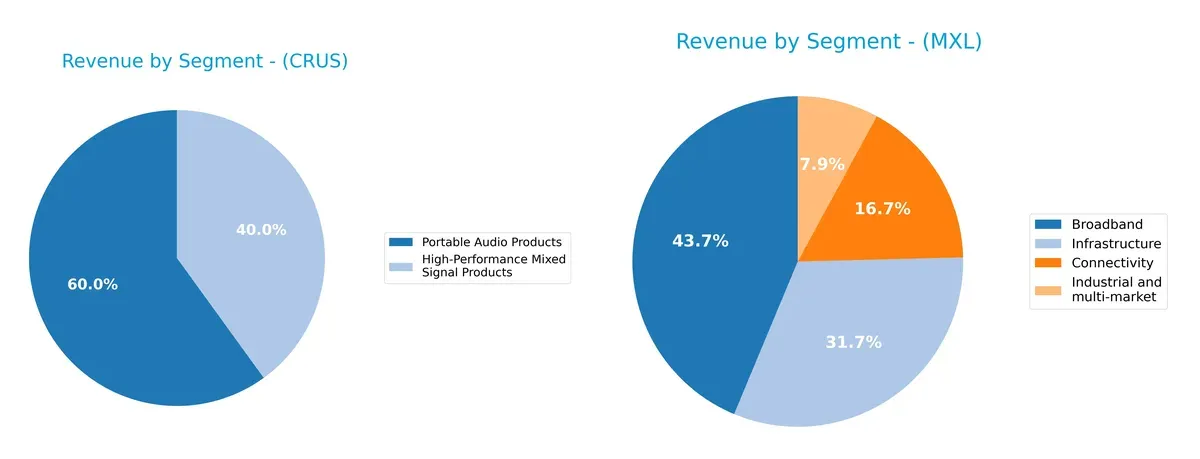

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how Cirrus Logic and MaxLinear diversify their income streams and where their primary sector bets lie:

Cirrus Logic anchors revenue heavily in Portable Audio Products at $1.14B in 2025, with High-Performance Mixed Signal Products at $759M. MaxLinear shows a more balanced portfolio with Broadband at $204M, Infrastructure $148M, Connectivity $78M, and Industrial $37M. Cirrus risks concentration in audio ecosystems, while MaxLinear leverages infrastructure and multi-market diversification to reduce sector vulnerability.

Strengths and Weaknesses Comparison

This table compares the strengths and weaknesses of Cirrus Logic, Inc. (CRUS) and MaxLinear, Inc. (MXL):

CRUS Strengths

- Strong profitability with net margin 17.48% and ROE 17.01%

- Favorable ROIC at 14.2% surpassing WACC

- Low debt levels with DE 0.07 and interest coverage 495

- High liquidity shown by quick ratio 4.82

- Diversified revenue from portable audio and mixed signal products

- Significant global presence, especially in China and Asia

MXL Strengths

- Favorable current and quick ratios indicate adequate liquidity

- Moderate debt levels with DE 0.29 and debt to assets 17.23%

- Product diversification across broadband, connectivity, industrial, infrastructure

- Market presence in Asia, Rest of World, and United States

- Reasonable fixed asset turnover at 4.65

CRUS Weaknesses

- Unfavorable current ratio at 6.35 suggests working capital inefficiency

- No dividend yield limits income returns

- Neutral valuation multiples (PE 15.95, PB 2.71) may imply moderate market enthusiasm

- Asset turnover neutral at 0.81 indicates average asset use efficiency

MXL Weaknesses

- Negative profitability with net margin -68%, ROE -47%, and ROIC -24%

- High WACC at 11.7% raises capital cost concerns

- Negative interest coverage (-13.01) signals financial distress

- Unfavorable asset turnover at 0.42 shows poor asset utilization

- No dividend yield limits shareholder income

Overall, CRUS demonstrates robust profitability, strong liquidity, and global diversification, though it faces some liquidity ratio concerns. MXL struggles with profitability and asset efficiency but maintains decent liquidity and product diversification. These factors shape each company’s strategic financial and operational priorities.

The Moat Duel: Analyzing Competitive Defensibility

Structural moats shield long-term profits from relentless competition erosion. Only durable advantages withstand market pressures and secure lasting value creation:

Cirrus Logic, Inc.: Intangible Assets and Innovation Powerhouse

Cirrus Logic’s moat stems from proprietary audio technologies and integrated mixed-signal solutions. Its strong ROIC above WACC reflects efficient capital use and margin stability. In 2026, expanding audio and haptic applications deepen this moat amid growing AR/VR demands.

MaxLinear, Inc.: Cost Advantage in Communication SoCs

MaxLinear relies on cost-efficient, high-performance communication chips, contrasting Cirrus’ innovation focus. However, its sharply declining ROIC signals value destruction. Growth opportunities in 5G infrastructure exist but require urgent profitability turnaround to sustain competitiveness.

Innovation Edge vs. Cost Efficiency: Who Holds the Moat Crown?

Cirrus Logic boasts a wider, more durable moat with consistent ROIC growth and strong margin control. MaxLinear’s weakening profitability undermines its cost advantage. Cirrus is clearly better equipped to defend and expand its market share.

Which stock offers better returns?

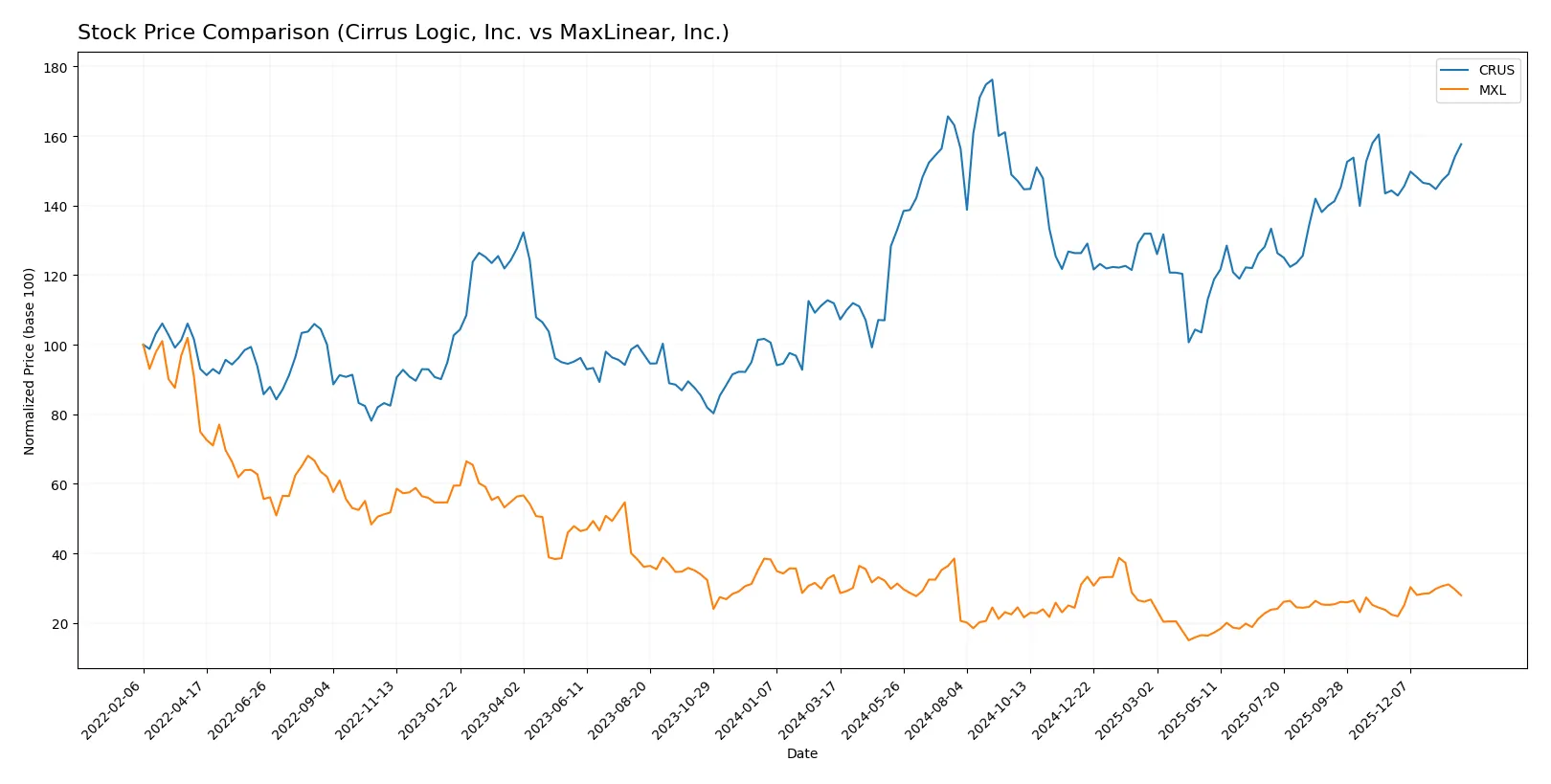

Over the past 12 months, Cirrus Logic, Inc. and MaxLinear, Inc. displayed contrasting stock price dynamics, with Cirrus Logic showing robust gains and MaxLinear facing a decline followed by recent recovery.

Trend Comparison

Cirrus Logic’s stock rose 40.89% over the past year, marking a bullish trend with accelerating momentum and significant volatility reflected by a 14.44 std deviation. The price peaked at 145.69 and bottomed at 82.02.

MaxLinear’s stock fell 17.26% over the same period, indicating a bearish trend despite acceleration in its decline. Volatility remained low with a 3.37 std deviation, with highs at 24.05 and lows at 9.31.

Comparing both, Cirrus Logic outperformed MaxLinear with a strong positive return, while MaxLinear ended the year with net losses despite recent short-term gains.

Target Prices

Analysts show a moderately bullish consensus for both Cirrus Logic and MaxLinear.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Cirrus Logic, Inc. | 100 | 155 | 138.75 |

| MaxLinear, Inc. | 15 | 25 | 21 |

The target prices for Cirrus Logic imply roughly a 6% upside from the current 130.34 price, signaling moderate optimism. MaxLinear’s consensus target suggests a 21% potential gain from 17.35, reflecting more aggressive market expectations.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Cirrus Logic, Inc. Grades

The following table summarizes recent grades assigned by reputable firms for Cirrus Logic:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Keybanc | Maintain | Overweight | 2025-11-05 |

| Barclays | Maintain | Equal Weight | 2025-11-05 |

| Benchmark | Maintain | Buy | 2025-11-05 |

| Stifel | Maintain | Buy | 2025-11-05 |

| Susquehanna | Maintain | Positive | 2025-10-22 |

| Stifel | Maintain | Buy | 2025-10-17 |

| Stifel | Maintain | Buy | 2025-09-12 |

| Barclays | Maintain | Equal Weight | 2025-05-07 |

| Barclays | Maintain | Equal Weight | 2025-04-22 |

| Stifel | Maintain | Buy | 2025-04-17 |

MaxLinear, Inc. Grades

Below are recent grades assigned by recognized grading companies for MaxLinear:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Wells Fargo | Maintain | Equal Weight | 2026-01-30 |

| Benchmark | Maintain | Buy | 2026-01-16 |

| Benchmark | Maintain | Buy | 2025-10-24 |

| Benchmark | Maintain | Buy | 2025-10-17 |

| Benchmark | Maintain | Buy | 2025-09-02 |

| Loop Capital | Maintain | Hold | 2025-08-04 |

| Wells Fargo | Maintain | Equal Weight | 2025-07-24 |

| Benchmark | Maintain | Buy | 2025-07-24 |

| Susquehanna | Maintain | Neutral | 2025-07-24 |

| Susquehanna | Maintain | Neutral | 2025-07-22 |

Which company has the best grades?

Cirrus Logic receives multiple “Buy” and “Overweight” ratings, signaling stronger institutional confidence. MaxLinear shows several “Buy” ratings but also holds “Equal Weight” and “Neutral” stances, indicating more cautious sentiment. Investors might interpret Cirrus’s grades as a more favorable outlook.

Risks specific to each company

The following categories identify critical pressure points and systemic threats facing Cirrus Logic, Inc. and MaxLinear, Inc. in the 2026 market environment:

1. Market & Competition

Cirrus Logic, Inc.

- Faces intense competition in mixed-signal processing but benefits from strong niche in audio codecs.

MaxLinear, Inc.

- Operates in highly competitive RF and communication SoC markets with pressure from larger integrated players.

2. Capital Structure & Debt

Cirrus Logic, Inc.

- Maintains a low debt-to-equity ratio (0.07), indicating conservative leverage and strong balance sheet.

MaxLinear, Inc.

- Higher debt ratio (0.29) increases financial risk, coupled with negative interest coverage signaling distress.

3. Stock Volatility

Cirrus Logic, Inc.

- Beta of 1.08 shows moderate market sensitivity, reflecting stable investor confidence.

MaxLinear, Inc.

- Beta of 1.77 indicates high volatility, exposing investors to greater market swings.

4. Regulatory & Legal

Cirrus Logic, Inc.

- Operates globally with standard semiconductor industry regulatory risks; no significant legal issues reported.

MaxLinear, Inc.

- Also subject to global regulatory scrutiny, especially in communications sectors, with potential compliance costs.

5. Supply Chain & Operations

Cirrus Logic, Inc.

- Benefits from diversified suppliers but still vulnerable to semiconductor supply disruptions.

MaxLinear, Inc.

- Faces risks from complex supply chains in RF components and system integration, potentially impacting delivery.

6. ESG & Climate Transition

Cirrus Logic, Inc.

- Increasing focus on energy-efficient products aligns with climate transition imperatives.

MaxLinear, Inc.

- ESG efforts less visible; lagging on sustainability metrics could impact investor sentiment.

7. Geopolitical Exposure

Cirrus Logic, Inc.

- Moderate exposure to US-China trade tensions affecting semiconductor supply chains.

MaxLinear, Inc.

- Similar geopolitical risks heightened by global communications infrastructure dependencies.

Which company shows a better risk-adjusted profile?

Cirrus Logic’s strongest risk is its supply chain exposure amid global semiconductor shortages. MaxLinear’s primary risk lies in capital structure and weak profitability, highlighted by negative margins and interest coverage. Cirrus Logic demonstrates a superior risk-adjusted profile, evidenced by a robust Altman Z-score of 12.44 versus MaxLinear’s 2.13 in the grey zone, underscoring MaxLinear’s financial vulnerability amid market volatility.

Final Verdict: Which stock to choose?

Cirrus Logic, Inc. (CRUS) excels as a cash-generating machine with a durable competitive advantage. Its consistent ROIC well above WACC signals value creation and operational strength. The main point of vigilance is its unusually high current ratio, which might indicate inefficient asset use. It suits an Aggressive Growth portfolio focused on quality and profitability.

MaxLinear, Inc. (MXL) offers a strategic moat through its high R&D intensity and potential for innovation. However, it currently struggles with value destruction and negative profitability metrics, reflecting higher risk. Compared to CRUS, it presents more volatility and less financial stability, fitting a High-Risk, High-Reward speculative portfolio.

If you prioritize stable value creation and efficient capital use, Cirrus Logic outshines MaxLinear with better profitability and financial health. However, if you seek speculative growth fueled by innovation and can tolerate significant risk, MaxLinear offers potential upside despite its current challenges. Both warrant careful risk assessment aligned with your investment profile.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Cirrus Logic, Inc. and MaxLinear, Inc. to enhance your investment decisions: