Marvell Technology, Inc. and Cirrus Logic, Inc. are two prominent players in the semiconductor industry, each driving innovation in mixed-signal and digital processing solutions. While Marvell focuses on Ethernet and storage products, Cirrus Logic specializes in audio and power management ICs. Their market overlap and distinct innovation strategies make this comparison compelling. Join me as we explore which company presents the most attractive investment opportunity in 2026.

Table of contents

Companies Overview

I will begin the comparison between Marvell Technology and Cirrus Logic by providing an overview of these two companies and their main differences.

Marvell Technology Overview

Marvell Technology, Inc. designs, develops, and sells a broad portfolio of semiconductor solutions including Ethernet controllers, network adapters, ASICs, and storage controllers for HDDs and SSDs. Founded in 1995 and headquartered in Wilmington, Delaware, Marvell operates globally with over 7K employees. The company plays a significant role in the semiconductor industry, offering products that support advanced data storage and networking technologies.

Cirrus Logic Overview

Cirrus Logic, Inc. is a fabless semiconductor company specializing in low-power, high-precision mixed-signal processing solutions, particularly audio codecs and digital signal processors. Established in 1984 and based in Austin, Texas, Cirrus Logic serves diverse markets such as smartphones, AR/VR, automotive, and industrial applications with around 1.6K employees. Its audio-focused product portfolio enhances user experience with features like noise cancellation and high-fidelity sound.

Key similarities and differences

Both companies operate in the semiconductor industry and serve global markets with advanced technology solutions. Marvell focuses on a wider range of networking and storage semiconductors, while Cirrus Logic specializes in mixed-signal audio and industrial ICs. Marvell’s workforce and market capitalization are substantially larger, reflecting its broader product scope, whereas Cirrus Logic has a more niche focus on audio and precision processing.

Income Statement Comparison

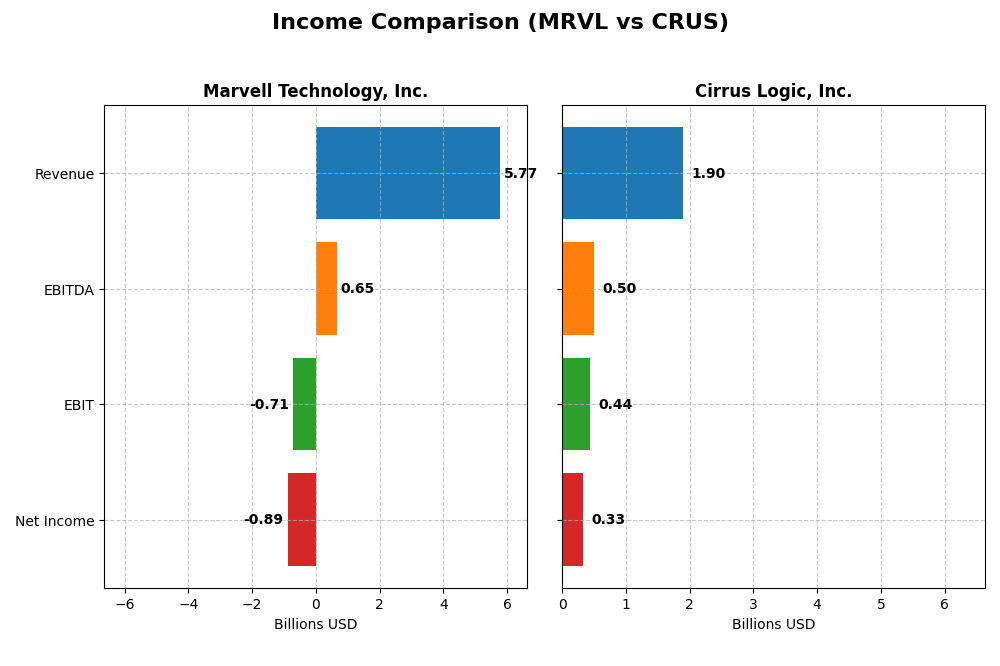

The table below compares the key income statement metrics for Marvell Technology, Inc. and Cirrus Logic, Inc. for the fiscal year 2025.

| Metric | Marvell Technology, Inc. | Cirrus Logic, Inc. |

|---|---|---|

| Market Cap | 69.3B | 6.3B |

| Revenue | 5.77B | 1.90B |

| EBITDA | 652M | 497M |

| EBIT | -705M | 445M |

| Net Income | -885M | 332M |

| EPS | -1.02 | 6.24 |

| Fiscal Year | 2025 | 2025 |

Income Statement Interpretations

Marvell Technology, Inc.

Marvell Technology’s revenue nearly doubled from 2021 to 2025, reaching $5.77B in the latest fiscal year. However, net income trends show persistent losses, totaling -$885M in 2025. Gross margin remained relatively strong at 41.31%, but operating and net margins continue to be negative. The most recent year saw modest revenue growth of 4.7%, yet EBIT fell sharply by 29%, reflecting profitability challenges.

Cirrus Logic, Inc.

Cirrus Logic reported steady revenue growth over 2021-2025, with $1.9B in 2025, alongside consistent net income increases, reaching $331M. Margins improved notably, with a gross margin of 52.53% and positive EBIT and net margins of 23.46% and 17.48%, respectively. The latest year showed solid growth in revenue (6%) and net income (14%), indicating strengthening profitability and operational efficiency.

Which one has the stronger fundamentals?

Cirrus Logic exhibits stronger fundamentals with favorable margins across gross, EBIT, and net income, supported by consistent profit growth and efficient expense management. Marvell Technology’s revenue growth is robust but overshadowed by ongoing net losses and negative operating margins, signaling more risk and weaker profitability compared to Cirrus Logic’s stable and profitable performance.

Financial Ratios Comparison

The table below presents the most recent available financial ratios for Marvell Technology, Inc. and Cirrus Logic, Inc., illustrating key performance and financial health metrics for fiscal year 2025.

| Ratios | Marvell Technology, Inc. (MRVL) | Cirrus Logic, Inc. (CRUS) |

|---|---|---|

| ROE | -6.59% | 17.01% |

| ROIC | -3.88% | 14.20% |

| P/E | -110.4 | 15.95 |

| P/B | 7.27 | 2.71 |

| Current Ratio | 1.54 | 6.35 |

| Quick Ratio | 1.03 | 4.82 |

| D/E (Debt-to-Equity) | 0.32 | 0.07 |

| Debt-to-Assets | 21.5% | 6.18% |

| Interest Coverage | -3.80 | 457.0 |

| Asset Turnover | 0.29 | 0.81 |

| Fixed Asset Turnover | 5.56 | 6.62 |

| Payout Ratio | -23.4% | 0% |

| Dividend Yield | 0.21% | 0% |

Interpretation of the Ratios

Marvell Technology, Inc.

Marvell Technology shows a mixed ratio profile with more unfavorable than favorable signals. Key concerns include negative net margin (-15.35%), negative returns on equity (-6.59%) and capital (-3.88%), and poor interest coverage (-3.72). However, liquidity ratios like current (1.54) and quick ratio (1.03) are favorable. Dividend yield is low at 0.21%, indicating modest shareholder returns with possible risk due to weak profitability.

Cirrus Logic, Inc.

Cirrus Logic presents generally strong financial ratios with favorable net margin (17.48%), ROE (17.01%), and ROIC (14.2%). The company exhibits excellent interest coverage (495.45) and a low debt-to-equity ratio (0.07). Current ratio is high (6.35) but considered unfavorable, possibly reflecting excess liquidity. Cirrus Logic does not pay dividends, consistent with a reinvestment or growth strategy prioritizing operational strength.

Which one has the best ratios?

Comparing both, Cirrus Logic holds a more favorable overall ratio profile with 57.14% favorable ratios against Marvell’s 42.86%. Cirrus demonstrates stronger profitability, capital efficiency, and solvency metrics. Marvell’s higher proportion of unfavorable ratios and negative profitability metrics suggest more financial challenges relative to Cirrus Logic’s predominantly positive indicators.

Strategic Positioning

This section compares the strategic positioning of Marvell Technology, Inc. and Cirrus Logic, Inc., focusing on Market position, Key segments, and exposure to technological disruption:

Marvell Technology, Inc.

- Large market cap at $69.3B, facing high beta and competitive pressure in semiconductors.

- Diversified segments: Data Center ($4.16B), Enterprise Networking, Carrier Infrastructure, Automotive, Consumer.

- Exposure through mixed-signal, Ethernet, storage, and application processors; broad semiconductor tech base.

Cirrus Logic, Inc.

- Smaller market cap of $6.3B, with lower beta and moderate competitive pressures.

- Concentrated on Portable Audio ($1.14B) and High-Performance Mixed Signal Products ($759M).

- Focus on low-power mixed-signal and audio processing, including advanced sound and haptic technologies.

Marvell Technology, Inc. vs Cirrus Logic, Inc. Positioning

Marvell pursues a diversified strategy across multiple semiconductor markets, offering scale advantages but facing complexity. Cirrus Logic concentrates on audio and high-precision mixed-signal niches, enabling specialization but with narrower market scope.

Which has the best competitive advantage?

Cirrus Logic shows a very favorable moat with growing ROIC above WACC, indicating durable competitive advantage. Marvell’s declining ROIC below WACC signals value destruction and a very unfavorable moat position.

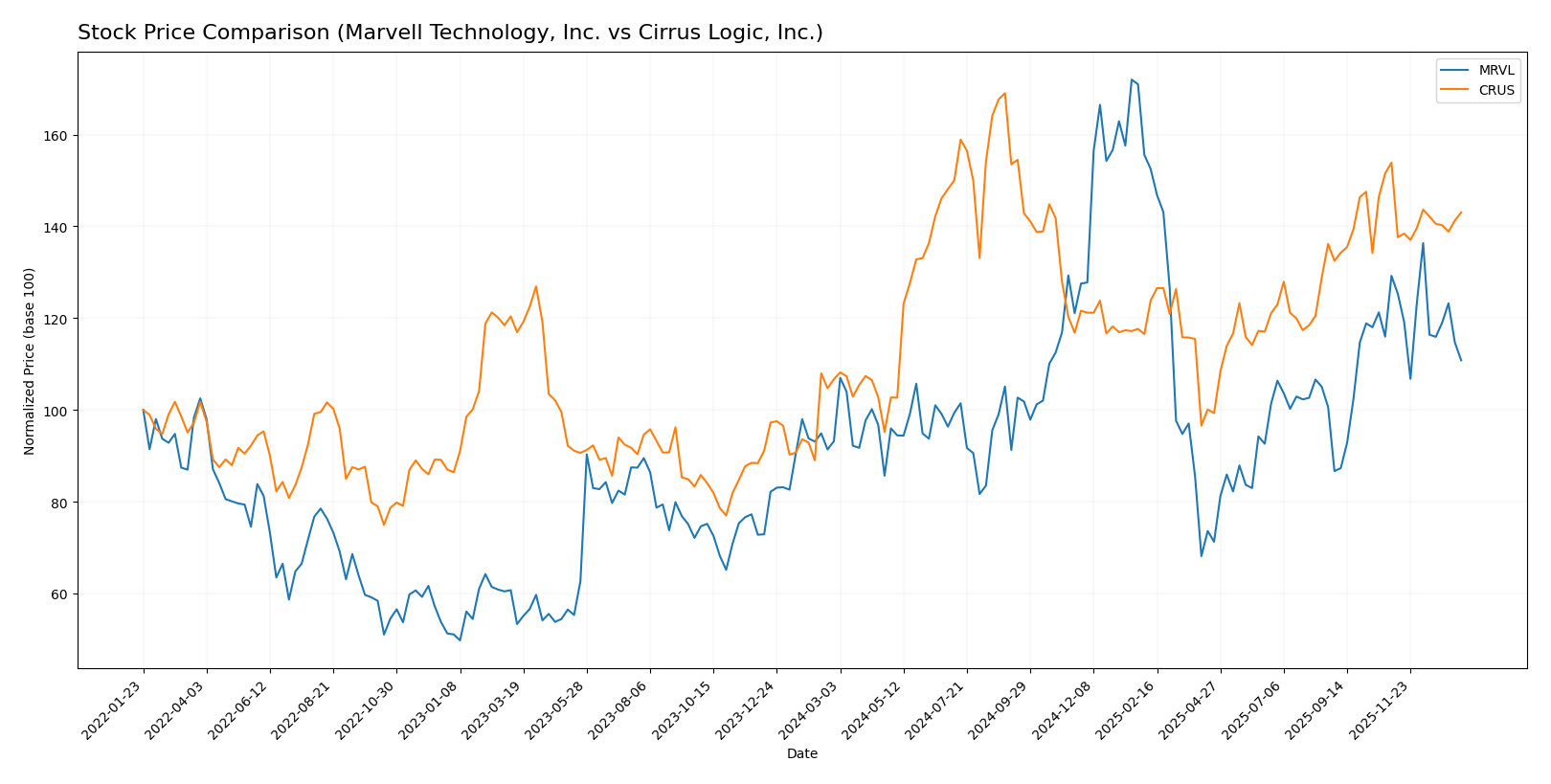

Stock Comparison

The stock price chart highlights notable bullish trends for both Marvell Technology, Inc. and Cirrus Logic, Inc. over the past 12 months, with Marvell showing a decelerating upward momentum and Cirrus Logic delivering stronger gains but also slowing growth.

Trend Analysis

Marvell Technology, Inc. experienced an 18.94% price increase over the past year, indicating a bullish trend with decelerating momentum. The stock reached a high of 124.76 and a low of 49.43, with recent months showing a short-term bearish correction of -14.25%.

Cirrus Logic, Inc. showed a 34.06% price gain over the same period, also bullish with deceleration in trend acceleration. Its price ranged between 82.02 and 145.69. Recent performance reflects a moderate decline of -7.06%, suggesting some short-term weakness.

Comparing both, Cirrus Logic outperformed Marvell Technology in overall market performance, delivering a higher percentage gain during the past year despite recent downward pressure in both stocks.

Target Prices

The current analyst consensus for target prices shows a positive outlook for both Marvell Technology, Inc. and Cirrus Logic, Inc.

| Company | Target High | Target Low | Consensus |

|---|---|---|---|

| Marvell Technology, Inc. | 156 | 80 | 117 |

| Cirrus Logic, Inc. | 155 | 100 | 138.75 |

Analysts expect Marvell’s stock to rise from its current price of $80.38 toward the consensus target of $117, while Cirrus Logic’s current price of $123.28 is below its consensus target of $138.75, suggesting potential upside for both stocks.

Analyst Opinions Comparison

This section compares analysts’ ratings and grades for Marvell Technology, Inc. and Cirrus Logic, Inc.:

Rating Comparison

Marvell Technology, Inc. Rating

- Rating: B+, classified as Very Favorable by analysts.

- Discounted Cash Flow Score: 3, indicating a Moderate status.

- ROE Score: 4, assessed as Favorable.

- ROA Score: 5, considered Very Favorable.

- Debt To Equity Score: 2, with a Moderate evaluation.

- Overall Score: 3, indicating a Moderate standing.

Cirrus Logic, Inc. Rating

- Rating: A-, also classified as Very Favorable.

- Discounted Cash Flow Score: 4, indicating a Favorable status.

- ROE Score: 4, also assessed as Favorable.

- ROA Score: 5, also considered Very Favorable.

- Debt To Equity Score: 3, also Moderate but higher.

- Overall Score: 4, indicating a Favorable standing.

Which one is the best rated?

Based on the provided data, Cirrus Logic holds higher overall and discounted cash flow scores than Marvell Technology, reflecting a generally better rating. Both have equally strong ROE and ROA scores, but Cirrus Logic’s overall evaluation is more favorable.

Scores Comparison

Here is a comparison of the financial health scores for Marvell Technology, Inc. (MRVL) and Cirrus Logic, Inc. (CRUS):

MRVL Scores

- Altman Z-Score: 6.76, indicating a safe zone status

- Piotroski Score: 7, classified as strong

CRUS Scores

- Altman Z-Score: 11.94, indicating a safe zone status

- Piotroski Score: 7, classified as strong

Which company has the best scores?

Both MRVL and CRUS have Altman Z-Scores well within the safe zone, but CRUS’s score is significantly higher. Both companies share the same Piotroski Score of 7, indicating strong financial health for each based on the provided data.

Grades Comparison

Here is a detailed comparison of recent grades for Marvell Technology, Inc. and Cirrus Logic, Inc.:

Marvell Technology, Inc. Grades

The following table lists the latest grades from notable grading companies for Marvell Technology, Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Rosenblatt | Maintain | Buy | 2026-01-07 |

| Melius Research | Upgrade | Buy | 2026-01-05 |

| Benchmark | Downgrade | Hold | 2025-12-08 |

| B. Riley Securities | Maintain | Buy | 2025-12-03 |

| JP Morgan | Maintain | Overweight | 2025-12-03 |

| Susquehanna | Maintain | Positive | 2025-12-03 |

| Benchmark | Maintain | Buy | 2025-12-03 |

| Oppenheimer | Maintain | Outperform | 2025-12-03 |

| Stifel | Maintain | Buy | 2025-12-03 |

| Rosenblatt | Maintain | Buy | 2025-12-03 |

Overall, Marvell Technology’s grades show a strong buy consensus with one recent downgrade to hold; most analysts maintain positive or buy ratings.

Cirrus Logic, Inc. Grades

The following table displays recent grades from recognized grading companies for Cirrus Logic, Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Keybanc | Maintain | Overweight | 2025-11-05 |

| Barclays | Maintain | Equal Weight | 2025-11-05 |

| Stifel | Maintain | Buy | 2025-11-05 |

| Benchmark | Maintain | Buy | 2025-11-05 |

| Susquehanna | Maintain | Positive | 2025-10-22 |

| Stifel | Maintain | Buy | 2025-10-17 |

| Stifel | Maintain | Buy | 2025-09-12 |

| Barclays | Maintain | Equal Weight | 2025-05-07 |

| Barclays | Maintain | Equal Weight | 2025-04-22 |

| Stifel | Maintain | Buy | 2025-04-17 |

Cirrus Logic’s grades are predominantly buy and equal weight, with consistent buy ratings from Stifel and other firms, indicating a stable positive outlook.

Which company has the best grades?

Marvell Technology has received more numerous and stronger buy ratings compared to Cirrus Logic, which features a mix of buys and equal weights. This difference suggests Marvell may be viewed as having a more bullish outlook by analysts, potentially influencing investor sentiment towards higher confidence in its future performance.

Strengths and Weaknesses

Below is a comparative overview of Marvell Technology, Inc. (MRVL) and Cirrus Logic, Inc. (CRUS) based on their diversification, profitability, innovation, global presence, and market share as of 2026.

| Criterion | Marvell Technology, Inc. (MRVL) | Cirrus Logic, Inc. (CRUS) |

|---|---|---|

| Diversification | Highly diversified across Data Center (4.16B), Carrier Infrastructure (338M), Enterprise Networking (626M), Automotive & Industrial, and Consumer segments | Focused on two main segments: Portable Audio (1.14B) and High-Performance Mixed Signal Products (759M) |

| Profitability | Negative net margin (-15.35%), negative ROE (-6.59%), and declining ROIC; company is destroying value | Strong profitability with net margin of 17.48%, ROE of 17.01%, and growing ROIC; company is creating value |

| Innovation | Moderate, with a stable product mix but declining returns indicating challenges in sustaining competitive edge | Demonstrates durable competitive advantage with innovation in high-performance mixed signal and audio products |

| Global presence | Significant presence in data center and networking markets globally | More niche, focused on audio and signal processing markets, less diversified geographically |

| Market Share | Strong in data center and enterprise networking sectors but facing profitability issues | Solid market share within audio and mixed-signal markets, supported by consistent revenue growth |

Key takeaways: Cirrus Logic shows a clear competitive advantage with strong profitability, innovation, and value creation. Marvell, despite its broad diversification and market presence, struggles with declining profitability and value destruction, signaling higher investment risk.

Risk Analysis

Below is a risk comparison table for Marvell Technology, Inc. (MRVL) and Cirrus Logic, Inc. (CRUS) based on the most recent data from 2025.

| Metric | Marvell Technology, Inc. (MRVL) | Cirrus Logic, Inc. (CRUS) |

|---|---|---|

| Market Risk | High (Beta 1.945, volatile range $47.09-$127.48) | Moderate (Beta 1.084, range $75.83-$136.92) |

| Debt level | Moderate (Debt-to-Equity 0.32; Debt to Assets 21.5%) | Low (Debt-to-Equity 0.07; Debt to Assets 6.18%) |

| Regulatory Risk | Moderate (global operations including China and other Asia markets) | Moderate (US-based with international sales) |

| Operational Risk | Moderate (7,042 employees, complex supply chain) | Low (1,609 employees, fabless model reduces operational costs) |

| Environmental Risk | Moderate (Manufacturing footprint in multiple countries) | Low (Fabless, less direct manufacturing impact) |

| Geopolitical Risk | High (Significant exposure to Asia, including China and Taiwan) | Moderate (US-based but global sales exposure) |

Marvell faces the most impactful risks in market volatility and geopolitical tensions due to its extensive Asian operations, especially in sensitive regions. Cirrus Logic displays lower debt and operational risks, with market risk more contained. Investors should closely monitor geopolitical developments and market fluctuations when considering Marvell.

Which Stock to Choose?

Marvell Technology, Inc. (MRVL) shows mixed income evolution with a 4.71% revenue growth but negative net margin at -15.35%, and a declining profitability trend. Its financial ratios are mostly unfavorable, though debt levels are moderate, culminating in a very favorable B+ rating.

Cirrus Logic, Inc. (CRUS) exhibits favorable income growth and profitability, including a 5.99% revenue increase and a positive net margin of 17.48%. Its financial ratios are predominantly favorable, supported by low debt, resulting in a very favorable A- rating.

For risk-averse investors prioritizing financial stability and profitability, CRUS might appear more favorable given its solid rating and consistent value creation. Conversely, growth-focused investors could interpret MRVL’s moderate revenue growth and moderate rating as a potential, albeit riskier, opportunity.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Marvell Technology, Inc. and Cirrus Logic, Inc. to enhance your investment decisions: