In the fast-evolving semiconductor industry, Lattice Semiconductor Corporation (LSCC) and Cirrus Logic, Inc. (CRUS) stand out as innovative players with distinct market approaches. While both companies operate in technology and serve overlapping sectors, LSCC focuses on programmable logic devices, and CRUS specializes in mixed-signal processing solutions. This comparison will help you understand which company offers a more compelling investment opportunity in 2026. Let’s explore their strengths and risks together.

Table of contents

Companies Overview

I will begin the comparison between Lattice Semiconductor Corporation and Cirrus Logic, Inc. by providing an overview of these two companies and their main differences.

Lattice Semiconductor Corporation Overview

Lattice Semiconductor Corporation develops and sells semiconductor products globally, focusing on field programmable gate arrays with four key product families. It also offers video connectivity application-specific standard products and licenses its technology portfolio through IP services. The company primarily serves original equipment manufacturers across communications, computing, consumer, industrial, and automotive markets. Founded in 1983, Lattice is headquartered in Hillsboro, Oregon, with a market cap of $11.7B.

Cirrus Logic, Inc. Overview

Cirrus Logic, Inc. is a fabless semiconductor company specializing in low-power, high-precision mixed-signal processing solutions. Its portfolio includes audio codecs, digital signal processors, and advanced SoundClear technology used in various consumer electronics and industrial applications. Founded in 1984 and based in Austin, Texas, Cirrus serves markets spanning smartphones, automotive entertainment, and energy systems, holding a market cap of $6.3B.

Key similarities and differences

Both companies operate in the semiconductor industry, serving broad technology markets with specialized products. Lattice focuses on programmable gate arrays and IP licensing, targeting OEMs in communication and computing sectors. Cirrus Logic emphasizes mixed-signal audio and power management solutions, catering to consumer electronics and industrial energy applications. While Lattice offers hardware and licensing, Cirrus is fabless, concentrating on product design and innovation.

Income Statement Comparison

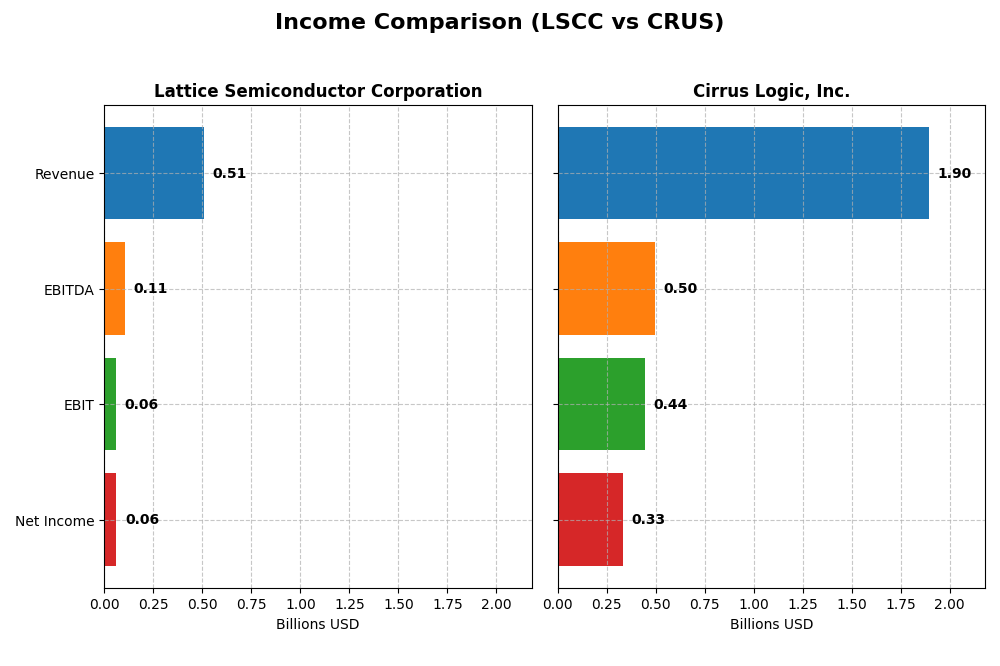

The following table presents a side-by-side comparison of key income statement metrics for Lattice Semiconductor Corporation and Cirrus Logic, Inc. for their most recent fiscal years.

| Metric | Lattice Semiconductor Corporation | Cirrus Logic, Inc. |

|---|---|---|

| Market Cap | 11.7B | 6.3B |

| Revenue | 509M | 1.9B |

| EBITDA | 107M | 497M |

| EBIT | 61M | 445M |

| Net Income | 61M | 332M |

| EPS | 0.44 | 6.24 |

| Fiscal Year | 2024 | 2025 |

Income Statement Interpretations

Lattice Semiconductor Corporation

Lattice Semiconductor showed a 25% revenue increase from 2020 to 2024 but experienced a 31% decline in revenue in the latest year. Net income grew overall by 29% during the period, yet fell sharply by 65.85% in 2024. Margins remain stable with a gross margin near 67% and a net margin around 12%, though recent margin contraction is evident. The 2024 year saw a significant slowdown in growth and earnings.

Cirrus Logic, Inc.

Cirrus Logic recorded a 38.5% revenue growth over 2021-2025, with a 6% rise in the most recent year. Net income surged 53% overall and increased by 13.9% in 2025. Margins are solid and improving, with a gross margin above 52% and net margin nearing 17.5%. The latest fiscal year reflects robust earnings growth and margin expansion, indicating strengthening profitability.

Which one has the stronger fundamentals?

Cirrus Logic demonstrates stronger fundamentals with consistent revenue and net income growth, alongside margin improvement and favorable earnings momentum. Lattice Semiconductor, while showing long-term growth, faces recent declines in revenue, earnings, and margins. Cirrus Logic’s higher proportion of favorable income statement metrics suggests a more resilient financial position in the current environment.

Financial Ratios Comparison

The table below presents a side-by-side comparison of key financial ratios for Lattice Semiconductor Corporation (LSCC) and Cirrus Logic, Inc. (CRUS) based on their most recent fiscal year data.

| Ratios | Lattice Semiconductor Corporation (LSCC) 2024 | Cirrus Logic, Inc. (CRUS) 2025 |

|---|---|---|

| ROE | 8.60% | 17.01% |

| ROIC | 4.59% | 14.20% |

| P/E | 133 | 15.95 |

| P/B | 11.41 | 2.71 |

| Current Ratio | 3.66 | 6.35 |

| Quick Ratio | 2.62 | 4.82 |

| D/E (Debt-to-Equity) | 0.02 | 0.07 |

| Debt-to-Assets | 1.81% | 6.18% |

| Interest Coverage | 130 | 457 |

| Asset Turnover | 0.60 | 0.81 |

| Fixed Asset Turnover | 7.62 | 6.62 |

| Payout ratio | 0 | 0 |

| Dividend yield | 0% | 0% |

Interpretation of the Ratios

Lattice Semiconductor Corporation

Lattice Semiconductor shows mixed financial health with a strong quick ratio and low debt levels indicating good short-term liquidity and conservative leverage. However, its high price-to-earnings and price-to-book ratios, along with unfavorable returns on equity and invested capital, signal valuation and profitability concerns. The company does not pay dividends, likely reflecting a reinvestment or growth strategy.

Cirrus Logic, Inc.

Cirrus Logic displays overall strong ratios, with favorable profitability metrics including net margin, ROE, and ROIC, and excellent interest coverage. Its current ratio is notably high but considered unfavorable, possibly indicating excess liquidity. Like Lattice, Cirrus Logic pays no dividends, which may stem from prioritizing reinvestment or growth initiatives over shareholder distributions.

Which one has the best ratios?

Cirrus Logic exhibits a more favorable overall ratio profile, with a higher proportion of positive financial metrics and stronger profitability indicators. Lattice Semiconductor’s ratios are less balanced, burdened by valuation and return concerns despite solid liquidity and low leverage, leading to a slightly unfavorable rating compared to Cirrus Logic’s favorable assessment.

Strategic Positioning

This section compares the strategic positioning of Lattice Semiconductor Corporation and Cirrus Logic, Inc., focusing on market position, key segments, and exposure to technological disruption:

Lattice Semiconductor Corporation

- Mid-sized semiconductor company with notable competitive pressure in diverse global markets.

- Key segments include FPGA product families and video connectivity; business driven by OEMs in communications, computing, industrial, and automotive sectors.

- Exposure through FPGA technology licensing and evolving semiconductor product families, facing industry disruption risks.

Cirrus Logic, Inc.

- Smaller market cap, fabless semiconductor firm with moderate competitive pressure.

- Focused on portable audio and high-performance mixed-signal products for consumer electronics and industrial applications.

- Exposure through advanced mixed-signal and audio processing technologies, including innovative SoundClear solutions.

Lattice Semiconductor Corporation vs Cirrus Logic, Inc. Positioning

Lattice Semiconductor is more diversified with FPGA and licensing businesses serving multiple end markets, while Cirrus Logic concentrates on audio and mixed-signal products. Lattice’s broader market exposure contrasts with Cirrus’s specialized product focus, each with inherent advantages and risks.

Which has the best competitive advantage?

Cirrus Logic demonstrates a very favorable moat with growing ROIC and consistent value creation, indicating a durable competitive advantage. Conversely, Lattice Semiconductor shows a very unfavorable moat with declining profitability and value destruction.

Stock Comparison

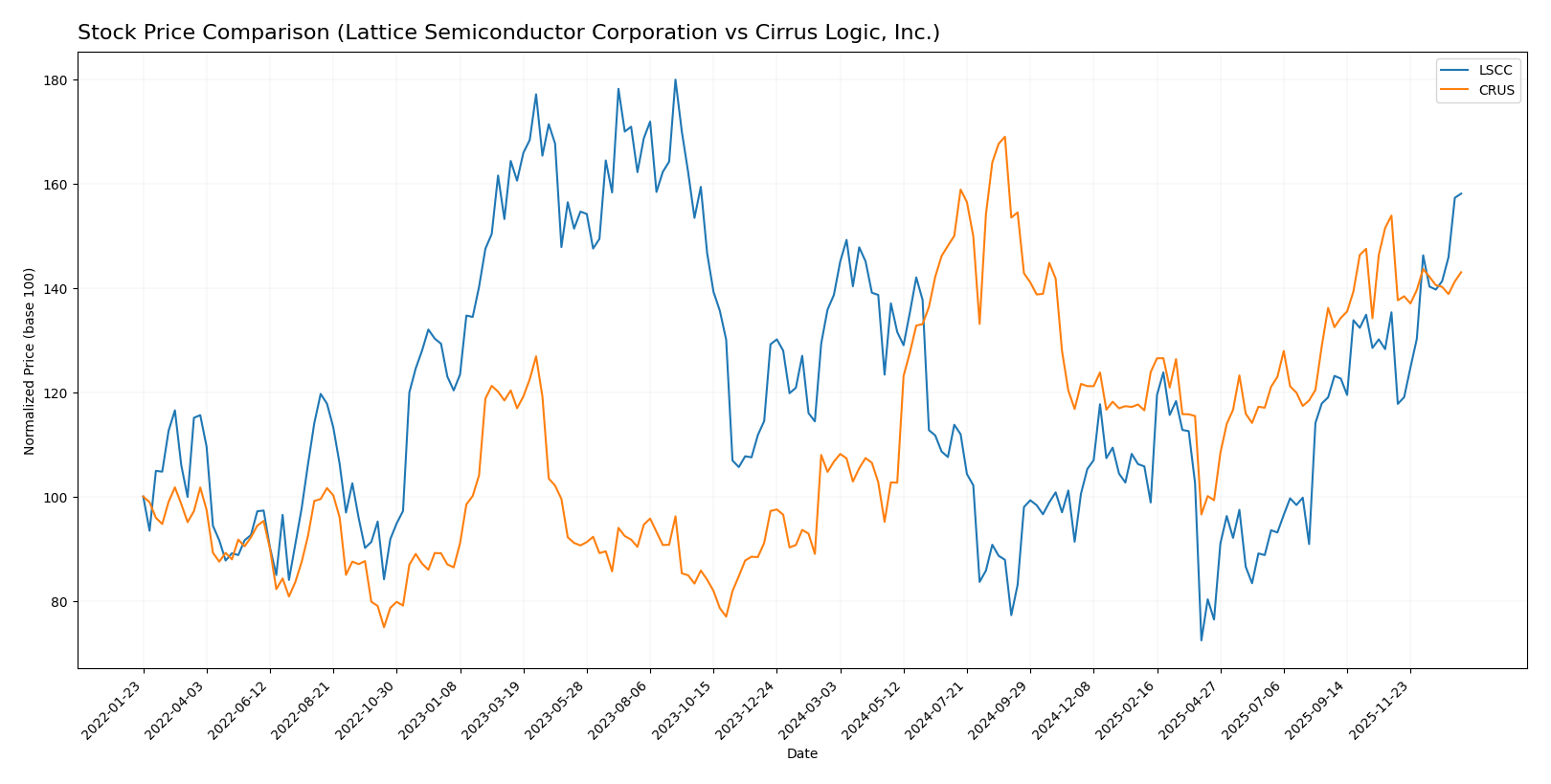

The past year saw notable bullish trends for both Lattice Semiconductor Corporation and Cirrus Logic, Inc., with LSCC accelerating upward while CRUS experienced deceleration in gains toward the end of the period.

Trend Analysis

Lattice Semiconductor Corporation (LSCC) exhibited a bullish trend over the past 12 months with a 14.02% price increase and accelerating momentum. The stock ranged between 39.03 and 85.23, showing moderate volatility with an 11.01 standard deviation.

Cirrus Logic, Inc. (CRUS) posted a stronger 34.06% gain over the same period but with decelerating momentum. The stock fluctuated between 82.02 and 145.69, reflecting higher volatility at a 14.46 standard deviation. Recently, CRUS showed a bearish trend with a -7.06% drop.

Comparing these trends, CRUS delivered the highest market performance over the 12 months despite recent declines, while LSCC maintained a steadier and accelerating upward trend.

Target Prices

Analysts present a clear target price consensus for Lattice Semiconductor Corporation and Cirrus Logic, Inc.

| Company | Target High | Target Low | Consensus |

|---|---|---|---|

| Lattice Semiconductor Corporation | 105 | 65 | 83 |

| Cirrus Logic, Inc. | 155 | 100 | 138.75 |

For Lattice Semiconductor, the consensus target of 83 is slightly below the current price of 85.23, suggesting moderate downside risk. Cirrus Logic shows a consensus target of 138.75, well above its current price of 123.28, indicating potential upside according to analysts.

Analyst Opinions Comparison

This section compares analysts’ ratings and grades for Lattice Semiconductor Corporation and Cirrus Logic, Inc.:

Rating Comparison

LSCC Rating

- Rating: B-, indicating a very favorable overall financial standing.

- Discounted Cash Flow Score: Moderate at 3, suggesting average valuation outlook.

- ROE Score: Moderate at 2, showing average efficiency in generating equity returns.

- ROA Score: Moderate at 3, indicating average asset utilization.

- Debt To Equity Score: Favorable at 4, reflecting low financial risk.

- Overall Score: Moderate at 2, summarizing an average financial profile.

CRUS Rating

- Rating: A-, reflecting a very favorable overall financial standing.

- Discounted Cash Flow Score: Favorable at 4, indicating a better valuation view.

- ROE Score: Favorable at 4, showing strong efficiency in generating equity returns.

- ROA Score: Very favorable at 5, indicating excellent asset utilization.

- Debt To Equity Score: Moderate at 3, indicating moderate financial risk.

- Overall Score: Favorable at 4, summarizing a strong financial profile.

Which one is the best rated?

Based strictly on the provided data, Cirrus Logic (CRUS) is better rated than Lattice Semiconductor (LSCC) across all key financial scores except debt-to-equity, where LSCC scores slightly better. Overall, CRUS demonstrates a stronger financial standing.

Scores Comparison

Here is a comparison of the financial scores of Lattice Semiconductor Corporation (LSCC) and Cirrus Logic, Inc. (CRUS):

LSCC Scores

- Altman Z-Score: 52.69, indicating a very safe zone.

- Piotroski Score: 5, reflecting average financial health.

CRUS Scores

- Altman Z-Score: 11.94, indicating a safe zone.

- Piotroski Score: 7, reflecting strong financial health.

Which company has the best scores?

Based solely on the provided data, LSCC has a higher Altman Z-Score suggesting stronger bankruptcy safety, while CRUS has a better Piotroski Score indicating stronger financial health. Each company excels in different score metrics.

Grades Comparison

The following presents the latest grades assigned to Lattice Semiconductor Corporation and Cirrus Logic, Inc. by recognized grading firms:

Lattice Semiconductor Corporation Grades

This table summarizes recent grades from established grading companies for Lattice Semiconductor Corporation.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Keybanc | Maintain | Overweight | 2026-01-13 |

| Stifel | Maintain | Buy | 2025-11-04 |

| Baird | Maintain | Outperform | 2025-11-04 |

| Needham | Maintain | Buy | 2025-11-04 |

| Rosenblatt | Maintain | Buy | 2025-11-04 |

| Benchmark | Maintain | Buy | 2025-11-04 |

| Susquehanna | Maintain | Positive | 2025-10-22 |

| Keybanc | Maintain | Overweight | 2025-09-30 |

| Needham | Maintain | Buy | 2025-09-22 |

| Benchmark | Maintain | Buy | 2025-09-11 |

Overall, Lattice Semiconductor Corporation consistently receives positive ratings, predominantly “Buy” and “Overweight,” indicating confidence from multiple firms.

Cirrus Logic, Inc. Grades

Below is a summary of recent grades from reputable grading companies for Cirrus Logic, Inc.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Keybanc | Maintain | Overweight | 2025-11-05 |

| Barclays | Maintain | Equal Weight | 2025-11-05 |

| Stifel | Maintain | Buy | 2025-11-05 |

| Benchmark | Maintain | Buy | 2025-11-05 |

| Susquehanna | Maintain | Positive | 2025-10-22 |

| Stifel | Maintain | Buy | 2025-10-17 |

| Stifel | Maintain | Buy | 2025-09-12 |

| Barclays | Maintain | Equal Weight | 2025-05-07 |

| Barclays | Maintain | Equal Weight | 2025-04-22 |

| Stifel | Maintain | Buy | 2025-04-17 |

Cirrus Logic shows a mix of “Buy” and “Equal Weight” grades, suggesting a generally positive but somewhat more cautious outlook compared to Lattice Semiconductor.

Which company has the best grades?

Lattice Semiconductor Corporation has received more uniformly positive grades, mainly “Buy” and “Overweight,” compared to Cirrus Logic’s blend of “Buy” and “Equal Weight.” This may indicate a stronger consensus of confidence in Lattice’s prospects, potentially affecting investor sentiment and portfolio allocation decisions.

Strengths and Weaknesses

Below is a comparative table summarizing the key strengths and weaknesses of Lattice Semiconductor Corporation (LSCC) and Cirrus Logic, Inc. (CRUS) based on the most recent financial and strategic data:

| Criterion | Lattice Semiconductor Corporation (LSCC) | Cirrus Logic, Inc. (CRUS) |

|---|---|---|

| Diversification | Limited product range; relies heavily on licensing and distributor sales | Well-diversified with strong segments in Portable Audio and Mixed Signal products |

| Profitability | Moderate net margin (12%) but unfavorable ROIC (4.59%) below WACC (11.86%) | Strong profitability with net margin 17.48%, ROIC (14.2%) above WACC (8.76%) |

| Innovation | Limited recent growth in ROIC; value destruction suggests innovation challenges | Demonstrates durable competitive advantage with growing ROIC and innovation-driven growth |

| Global presence | Moderate global footprint but less diversified revenue streams | Strong global presence supported by diverse product segments and stable revenue growth |

| Market Share | Smaller market share with declining financial efficiency | Larger market share with consistent value creation and expanding profitability |

Key takeaways: Cirrus Logic exhibits a robust competitive advantage with strong profitability, diversification, and innovation, making it a more attractive investment. Conversely, Lattice Semiconductor faces challenges in value creation and efficiency, warranting caution for investors.

Risk Analysis

Below is a comparative risk assessment table for Lattice Semiconductor Corporation (LSCC) and Cirrus Logic, Inc. (CRUS) based on the most recent data available:

| Metric | Lattice Semiconductor Corporation (LSCC) | Cirrus Logic, Inc. (CRUS) |

|---|---|---|

| Market Risk | High beta of 1.716 indicates high volatility | Moderate beta of 1.084 indicates moderate volatility |

| Debt level | Very low debt-to-equity (0.02), low debt-to-assets (1.81%) | Low debt-to-equity (0.07), debt-to-assets (6.18%) |

| Regulatory Risk | Moderate, typical for semiconductor industry | Moderate, typical for semiconductor industry |

| Operational Risk | Moderate, with solid operational metrics but slightly unfavorable ROE and WACC | Lower operational risk with favorable ROE and strong financial ratios |

| Environmental Risk | Moderate, as semiconductor manufacturing involves energy use and waste | Moderate, similar industry environmental considerations |

| Geopolitical Risk | Exposure to Asia, Europe, Americas trade tensions | Exposure to international markets, especially US and Asia |

Synthesizing these risks, LSCC carries higher market risk due to its elevated beta and slightly unfavorable financial efficiency metrics. CRUS shows a stronger financial profile with lower operational and debt risk. Geopolitical and regulatory risks remain relevant for both, given global supply chain sensitivities in semiconductors. Investors should weigh market volatility and operational efficiency carefully when choosing between these stocks.

Which Stock to Choose?

Lattice Semiconductor Corporation (LSCC) shows a favorable income statement with a 12.0% net margin but has experienced a 30.9% revenue decline over one year. Its financial ratios are slightly unfavorable overall, with low ROE (8.6%) and ROIC (4.59%), yet it maintains low debt levels and a very favorable interest coverage. The company’s economic moat is very unfavorable, indicating value destruction and declining profitability, despite a very favorable B- rating.

Cirrus Logic, Inc. (CRUS) demonstrates a favorable income statement with a 17.48% net margin and steady revenue growth of 6% over one year. Its financial ratios are globally favorable, featuring strong ROE (17.0%) and ROIC (14.2%), moderate debt, and excellent interest coverage. The company exhibits a very favorable economic moat with growing profitability and holds a very favorable A- rating, supported by strong Altman Z-Score and Piotroski scores.

Investors seeking growth potential might find CRUS more appealing due to its favorable financial ratios, durable competitive advantage, and consistent income growth. Conversely, more risk-tolerant investors aware of LSCC’s recent income challenges but favorable income quality and low debt might see different opportunities. Both companies exhibit strengths and risks, so the preferable choice could depend on the investor’s risk profile and investment strategy.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Lattice Semiconductor Corporation and Cirrus Logic, Inc. to enhance your investment decisions: