Home > Comparison > Financial Services > COF vs PYPL

The strategic rivalry between Capital One Financial Corporation and PayPal Holdings, Inc. shapes the evolution of the financial services sector. Capital One operates as a diversified credit services powerhouse, blending traditional banking with consumer and commercial lending. PayPal, by contrast, leads as a technology-driven digital payments platform with global reach. This analysis pits Capital One’s capital-intensive model against PayPal’s scalable tech platform to identify which offers superior risk-adjusted returns for a diversified portfolio.

Table of contents

Companies Overview

Capital One and PayPal dominate distinct niches within the financial services industry, reflecting divergent market dynamics.

Capital One Financial Corporation: Diversified Credit Services Leader

Capital One stands as a major financial services holding company focused on credit cards, consumer, and commercial banking. Its core revenue derives from interest on credit card loans and diversified lending products. In 2026, Capital One emphasizes expanding its digital and branch networks across the US, Canada, and UK to deepen customer engagement and loan growth.

PayPal Holdings, Inc.: Global Digital Payments Innovator

PayPal operates a technology-driven payments platform serving merchants and consumers globally. It generates revenue primarily through transaction fees on digital payments across 200 markets and multiple currencies. In 2026, PayPal prioritizes enhancing its ecosystem with brands like Venmo and Braintree to capture e-commerce growth and expand cross-border payment capabilities.

Strategic Collision: Similarities & Divergences

Capital One champions a traditional lending model blending physical and digital channels, while PayPal pursues an open, technology-first approach focused on digital payments and fintech innovation. Their primary battleground lies in consumer financial engagement—lending versus payments. These distinct models shape contrasting investment profiles: Capital One offers exposure to credit risk and loan growth, whereas PayPal delivers scalability and network effects in global digital commerce.

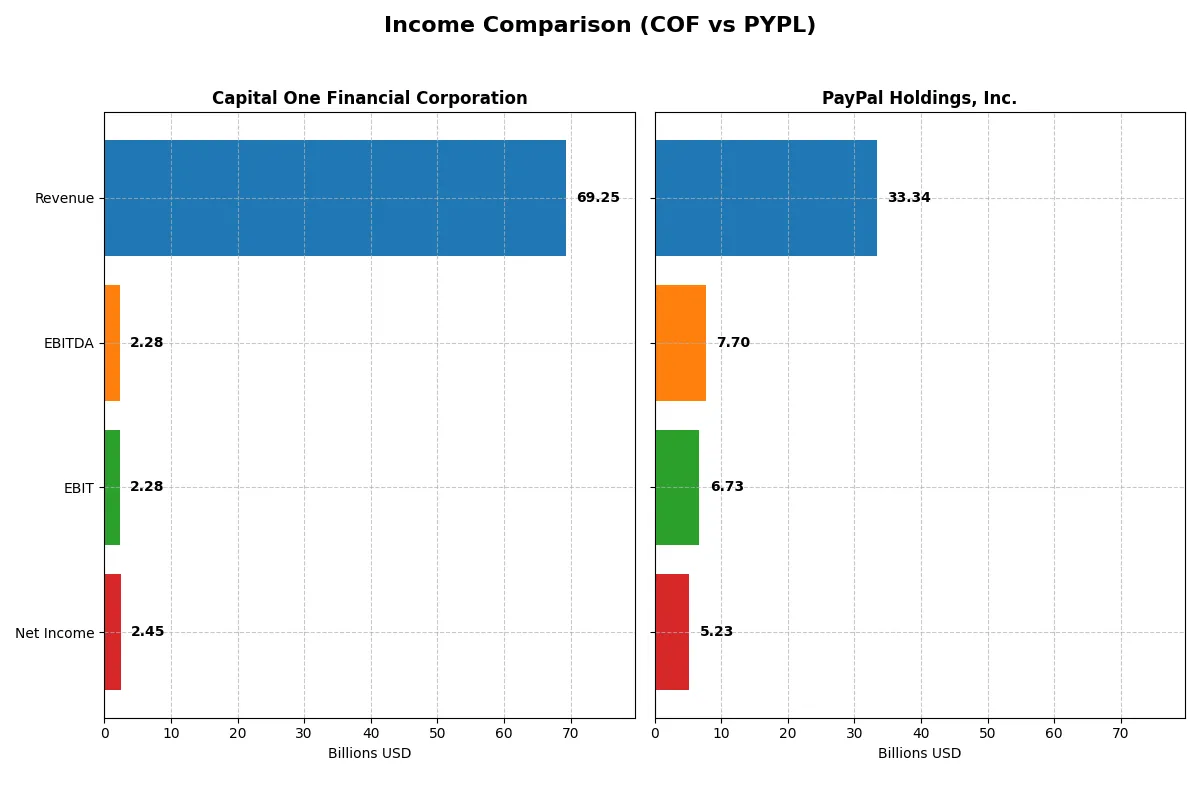

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Capital One Financial Corporation (COF) | PayPal Holdings, Inc. (PYPL) |

|---|---|---|

| Revenue | 69.3B | 33.3B |

| Cost of Revenue | 36.5B | 17.7B |

| Operating Expenses | 30.5B | 9.1B |

| Gross Profit | 32.8B | 15.7B |

| EBITDA | 2.3B | 7.7B |

| EBIT | 2.3B | 6.7B |

| Interest Expense | 30.5B | 0.4B |

| Net Income | 2.5B | 5.2B |

| EPS | 4.03 | 5.46 |

| Fiscal Year | 2025 | 2025 |

Income Statement Analysis: The Bottom-Line Duel

The forthcoming income statement comparison reveals which company converts revenue into profits most efficiently, driving long-term shareholder value.

Capital One Financial Corporation Analysis

Capital One’s revenue surged from $32B in 2021 to $69B in 2025, demonstrating strong top-line growth. However, net income dropped sharply from $12B to $2.45B over the same period, eroding net margins to just 3.5%. Gross margins remain solid near 47%, but operating expenses and interest costs weigh heavily on profitability. The 2025 decline in EBIT and net income signals deteriorating operational efficiency.

PayPal Holdings, Inc. Analysis

PayPal’s revenue grew moderately from $25B in 2021 to $33B in 2025, with net income rising from $4.17B to $5.23B. Gross margin steadied around 47%, while net margin expanded to nearly 16%, reflecting strong cost control and operational leverage. EBIT margin improved to over 20% in 2025, highlighting efficient capital allocation and sustainable profit growth. Recent momentum supports PayPal’s improving profitability profile.

Margin Power vs. Revenue Scale

PayPal outperforms Capital One on profitability and margin expansion, despite more modest revenue growth. Capital One’s impressive revenue scale masks declining net income and rising costs, signaling potential risks. For investors, PayPal’s profile of steady profit growth and superior margin control presents a more attractive, fundamentally sound investment opportunity.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | Capital One Financial Corporation (COF) | PayPal Holdings, Inc. (PYPL) |

|---|---|---|

| ROE | 7.8% (2024) | 25.8% (2025) |

| ROIC | 3.7% (2024) | 15.0% (2025) |

| P/E | 14.4x (2024) | 10.7x (2025) |

| P/B | 1.12x (2024) | 2.76x (2025) |

| Current Ratio | 0.14 (2024) | 1.29 (2025) |

| Quick Ratio | 0.14 (2024) | 1.29 (2025) |

| D/E | 0.75 (2024) | 0.49 (2025) |

| Debt-to-Assets | 9.3% (2024) | 12.5% (2025) |

| Interest Coverage | 0.40x (2024) | N/A (2025) |

| Asset Turnover | 0.11 (2024) | 0.41 (2025) |

| Fixed Asset Turnover | 12.0 (2024) | 19.5 (2025) |

| Payout Ratio | 24.4% (2024) | 2.5% (2025) |

| Dividend Yield | 1.70% (2024) | 0.23% (2025) |

| Fiscal Year | 2024 | 2025 |

*Note: Data reflects the most recent full fiscal year available for each company. Some metrics for Capital One’s 2025 year are unavailable or zero.*

Efficiency & Valuation Duel: The Vital Signs

Financial ratios act as a company’s DNA, unveiling hidden risks and operational efficiency critical for investment decisions.

Capital One Financial Corporation

Capital One shows weak profitability with a 0% ROE and a low 3.54% net margin, signaling operational challenges. Its P/E ratio at 53.42 marks the stock as expensive relative to earnings. The company offers a modest 1.07% dividend yield, reflecting limited shareholder returns amid reinvestment constraints.

PayPal Holdings, Inc.

PayPal delivers strong profitability with a 25.83% ROE and a 15.78% net margin, indicating efficient operations. Its P/E of 10.7 suggests a reasonably valued stock. PayPal’s low 0.23% dividend yield underscores a growth-focused reinvestment strategy, notably in R&D, supporting future expansion.

Premium Valuation vs. Operational Safety

PayPal outperforms with healthier profitability and a fair valuation, offering a better risk-reward balance than Capital One’s stretched multiples and weak returns. Investors prioritizing growth and operational strength may find PayPal’s profile more compelling.

Which one offers the Superior Shareholder Reward?

I observe that Capital One (COF) offers a 1.7% dividend yield with a sustainable 24% payout ratio, backed by strong free cash flow. Its moderate buybacks complement dividends, balancing shareholder returns and growth. PayPal (PYPL) pays nearly no dividends, focusing on reinvestment and growth, with smaller buybacks. Historically in financials, consistent dividends plus buybacks like COF’s model typically deliver steadier total returns. PYPL’s growth strategy suits risk-tolerant investors but lacks immediate yield. I conclude COF offers the superior shareholder reward in 2026 due to its balanced, sustainable distribution and buyback approach.

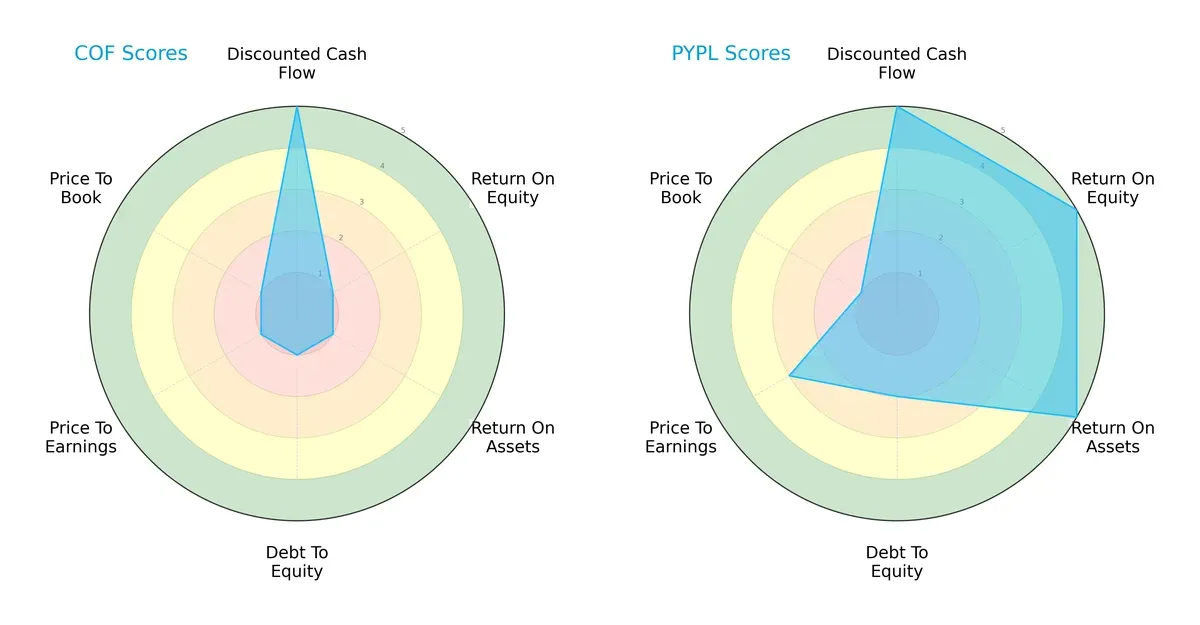

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Capital One Financial Corporation and PayPal Holdings, Inc., highlighting their core financial strengths and vulnerabilities:

PayPal dominates with strong profitability metrics, scoring 5 in ROE and ROA, while Capital One lags with just 1 in these areas. Both share a top DCF score of 5, indicating sound future cash flow expectations. Capital One’s balance sheet is highly leveraged, reflected in a weak Debt/Equity score of 1 versus PayPal’s moderate 2. PayPal shows a more balanced profile, though it trades at a moderate valuation, whereas Capital One’s valuation metrics signal undervaluation but come with financial risks.

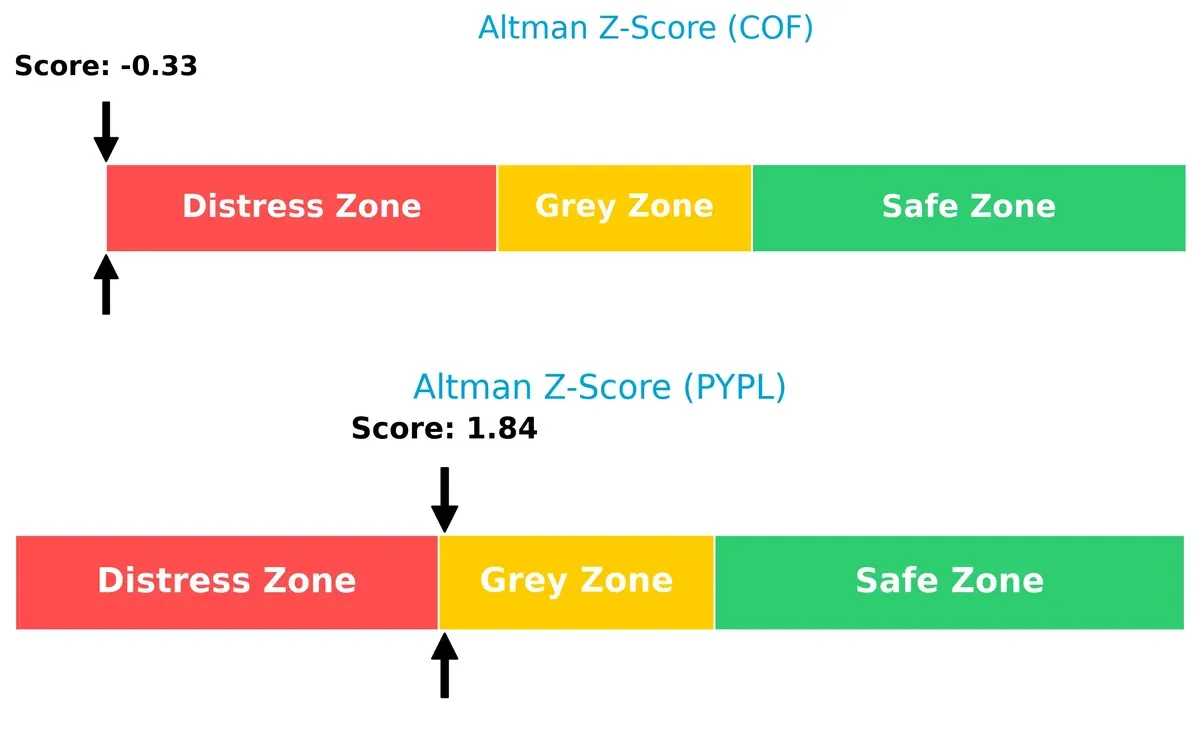

Bankruptcy Risk: Solvency Showdown

Capital One’s Altman Z-Score of -0.33 starkly contrasts with PayPal’s 1.84, putting Capital One deep in distress and PayPal in a moderate risk grey zone:

This gap signals PayPal’s stronger long-term survival odds amid economic cycles, while Capital One faces significant solvency concerns that investors must weigh carefully.

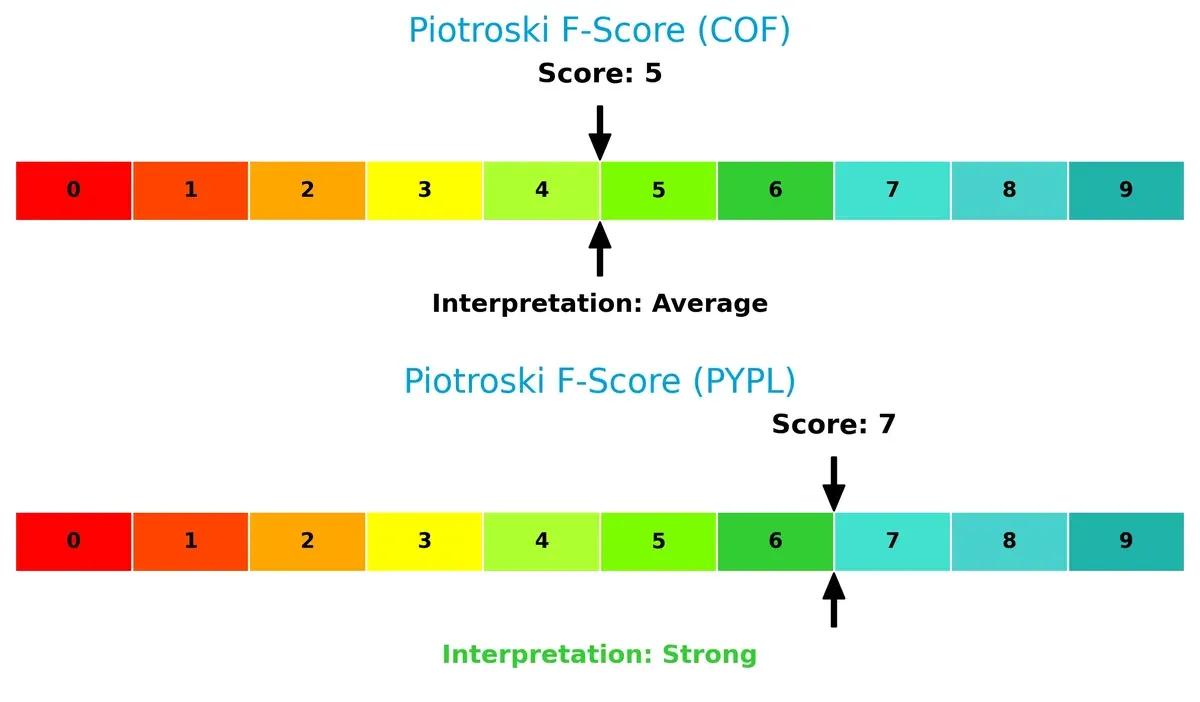

Financial Health: Quality of Operations

PayPal’s Piotroski F-Score of 7 indicates strong financial health, outperforming Capital One’s average score of 5, which raises some red flags internally:

PayPal’s superior operational metrics reflect better profitability, liquidity, and efficiency. Capital One’s middling score warns of potential weaknesses in internal controls or capital management that could impact future stability.

How are the two companies positioned?

This section dissects the operational DNA of Capital One and PayPal by comparing their revenue distribution and internal dynamics—strengths and weaknesses. The goal is to confront their economic moats to determine which model offers a more resilient, sustainable competitive advantage today.

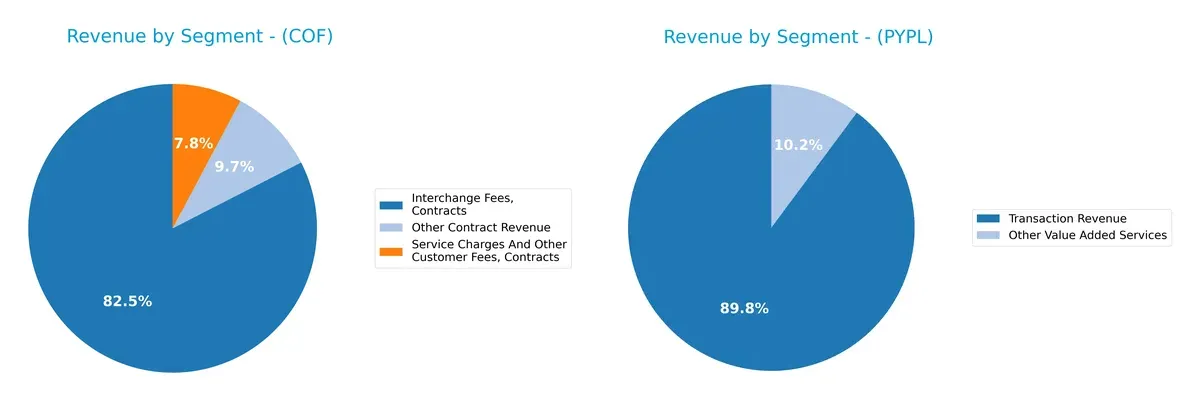

Revenue Segmentation: The Strategic Mix

The following visual comparison dissects how Capital One and PayPal diversify their income streams and where their primary sector bets lie:

Capital One anchors its revenue in Credit Card services, generating $25.7B in 2023, dwarfing Consumer Banking’s $9.3B and Commercial Banking’s $3.5B. This concentration signals reliance on credit infrastructure but exposes Capital One to credit cycle risks. PayPal pivots on Transaction Revenue, $29B in 2024, with Other Value Added Services at $3B, showing a more diversified digital payments ecosystem that supports platform lock-in and recurring revenue streams.

Strengths and Weaknesses Comparison

This table compares the strengths and weaknesses of Capital One Financial Corporation and PayPal Holdings, Inc.:

Capital One Financial Corporation Strengths

- Diversified revenue from credit card, consumer, and commercial banking

- Strong US market presence with $35.4B revenue

- Favorable debt-to-assets and debt-equity ratios

PayPal Holdings, Inc. Strengths

- High profitability with 15.78% net margin and 25.83% ROE

- Global revenue with significant non-US business

- Strong innovation in value-added services and efficient asset turnover

Capital One Financial Corporation Weaknesses

- Unfavorable profitability metrics including 0% ROE and ROIC

- Weak liquidity ratios with current and quick ratios at 0

- Very low interest coverage ratio (0.07)

- High P/E ratio at 53.42 signals expensive valuation

PayPal Holdings, Inc. Weaknesses

- Lower asset turnover ratio at 0.41

- Dividend yield low at 0.23%

- Neutral weighted average cost of capital at 9.07%

Capital One’s strengths lie in its diversified financial services and strong US presence but are undermined by weak profitability and liquidity. PayPal shows robust profitability and global reach, though asset utilization and dividend yield present challenges. Both companies must address these weaknesses to sustain competitive positioning.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only true shield protecting long-term profits from relentless competition erosion. Let’s examine how Capital One and PayPal defend their turf:

Capital One Financial Corporation: Cost Advantage in Credit Services

Capital One leverages cost advantages through scale and risk management, reflected in stable gross margins near 47%. However, declining ROIC signals weakening efficiency. Expansion into digital banking could either deepen or stress its moat in 2026.

PayPal Holdings, Inc.: Network Effects and Platform Ecosystem

PayPal’s moat stems from powerful network effects, driving high EBIT margins (20.2%) and growing ROIC above WACC by 5.9%. Its diversified global payments network fuels steady growth and strengthens its ecosystem into 2026.

Verdict: Cost Efficiency vs. Network Effects

PayPal exhibits a wider, deeper moat with growing profitability and sustainable capital returns. Capital One’s cost advantage faces erosion amid declining ROIC. PayPal stands better positioned to defend and extend market share moving forward.

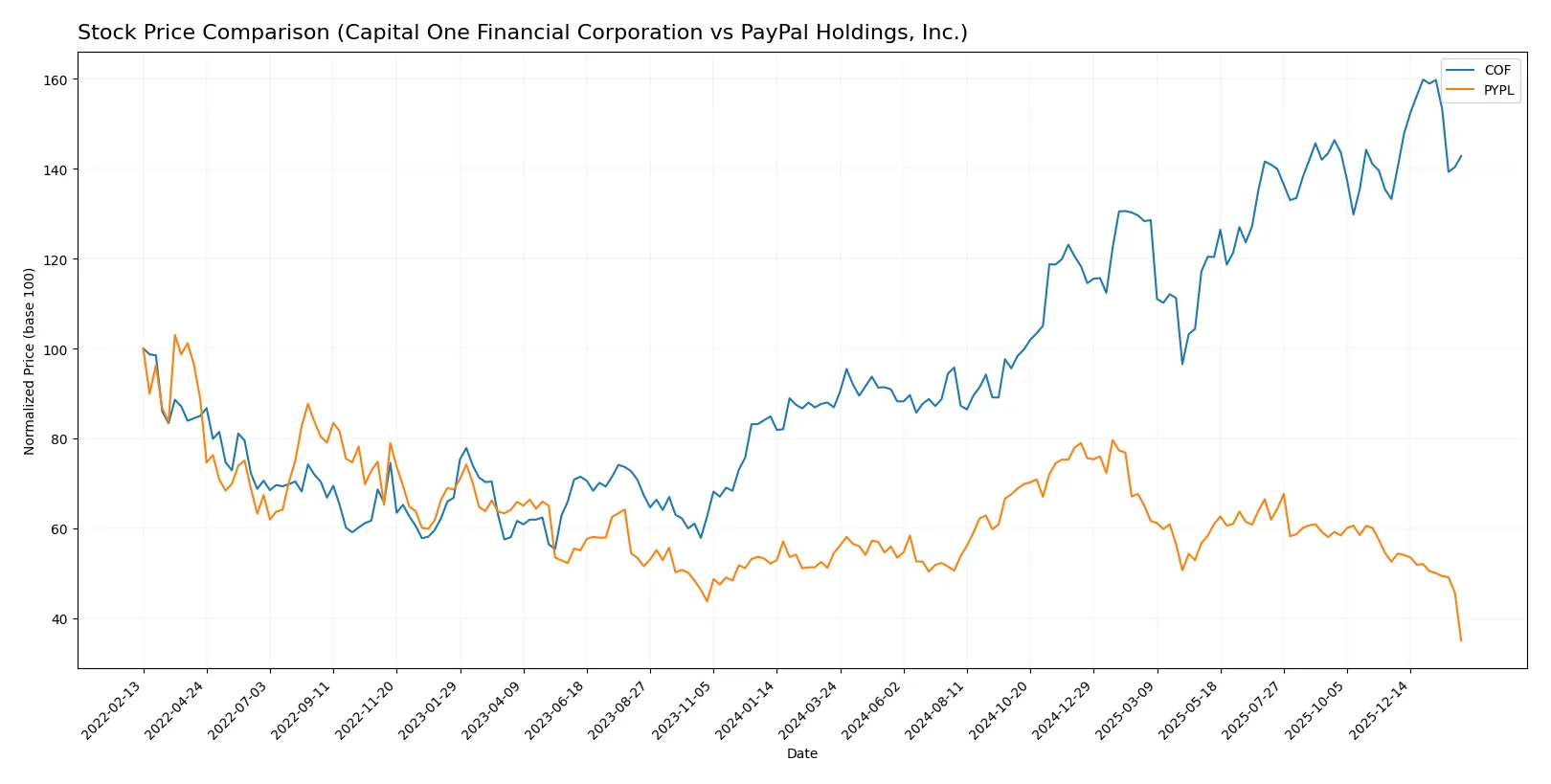

Which stock offers better returns?

Over the past year, Capital One Financial Corporation’s stock surged 64.4%, while PayPal Holdings, Inc. declined 35.7%, reflecting contrasting trading dynamics and investor sentiment in their sectors.

Trend Comparison

Capital One’s stock gained 64.4% over the past 12 months, marking a bullish trend with decelerating momentum and notable volatility, reaching a high of 249.32 and a low of 133.7.

PayPal’s stock dropped 35.7% in the same period, exhibiting a bearish trend with decelerating decline, lower volatility, and price ranging between 40.42 and 91.81.

Capital One’s bullish performance clearly outpaces PayPal’s bearish trajectory, delivering the highest market returns over the past year.

Target Prices

Analysts present a mixed but generally optimistic target price consensus for these financial services stocks.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Capital One Financial Corporation | 218 | 300 | 273.62 |

| PayPal Holdings, Inc. | 34 | 87 | 53.95 |

Capital One’s consensus target at 273.62 suggests upside from the current 222.79 price, reflecting confidence in its diversified banking model. PayPal’s 53.95 target also implies significant appreciation potential from its 40.42 price, despite wider target range reflecting uncertainty in digital payments growth.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Capital One Financial Corporation Grades

The table below summarizes recent grades from reputable financial institutions for Capital One Financial Corporation.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Truist Securities | Maintain | Buy | 2026-01-27 |

| Barclays | Maintain | Overweight | 2026-01-26 |

| BTIG | Maintain | Buy | 2026-01-23 |

| Morgan Stanley | Maintain | Overweight | 2026-01-20 |

| JP Morgan | Maintain | Neutral | 2026-01-12 |

| TD Cowen | Maintain | Buy | 2026-01-08 |

| Barclays | Maintain | Overweight | 2026-01-06 |

| Wells Fargo | Maintain | Overweight | 2026-01-05 |

| Keefe, Bruyette & Woods | Maintain | Outperform | 2026-01-02 |

| Citigroup | Maintain | Buy | 2025-12-31 |

PayPal Holdings, Inc. Grades

The table below outlines recent grades issued by established financial firms for PayPal Holdings, Inc.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Needham | Maintain | Hold | 2026-02-04 |

| Citizens | Downgrade | Market Perform | 2026-02-04 |

| Canaccord Genuity | Downgrade | Hold | 2026-02-04 |

| Morgan Stanley | Maintain | Underweight | 2026-02-04 |

| Wells Fargo | Maintain | Equal Weight | 2026-02-04 |

| Goldman Sachs | Maintain | Sell | 2026-02-04 |

| Macquarie | Maintain | Outperform | 2026-02-04 |

| JP Morgan | Maintain | Neutral | 2026-02-04 |

| Citigroup | Maintain | Neutral | 2026-02-04 |

| Evercore ISI Group | Maintain | In Line | 2026-02-04 |

Which company has the best grades?

Capital One consistently receives strong Buy and Overweight ratings, reflecting institutional confidence. PayPal’s grades show more caution, with several Hold and Underweight ratings. This divergence signals Capital One is currently viewed more favorably by analysts, potentially influencing investor sentiment and portfolio positioning.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

Capital One Financial Corporation

- Faces intense competition in traditional credit services with pressure from fintech disruptors.

PayPal Holdings, Inc.

- Competes in a fast-evolving digital payments space with rising rivalry from both startups and established tech giants.

2. Capital Structure & Debt

Capital One Financial Corporation

- Shows favorable debt-to-equity metrics but very weak interest coverage, raising refinancing risk concerns.

PayPal Holdings, Inc.

- Maintains moderate leverage with solid interest coverage, supporting financial flexibility and stability.

3. Stock Volatility

Capital One Financial Corporation

- Beta of 1.12 indicates moderate volatility relative to the market, reflecting sector cyclicality.

PayPal Holdings, Inc.

- Higher beta at 1.42 suggests greater sensitivity to market swings and technology sector risks.

4. Regulatory & Legal

Capital One Financial Corporation

- Exposure to stringent banking regulations and compliance costs in multiple jurisdictions.

PayPal Holdings, Inc.

- Faces regulatory scrutiny over data privacy, payment processing, and cross-border transactions.

5. Supply Chain & Operations

Capital One Financial Corporation

- Relies on stable banking infrastructure but vulnerable to operational disruptions and cybersecurity threats.

PayPal Holdings, Inc.

- Depends heavily on technology platforms and third-party integrations, exposing it to tech outages and security risks.

6. ESG & Climate Transition

Capital One Financial Corporation

- Increasing pressure to align lending and investment practices with climate goals.

PayPal Holdings, Inc.

- Faces challenges integrating ESG principles into global payment operations and reducing carbon footprint.

7. Geopolitical Exposure

Capital One Financial Corporation

- Operations concentrated primarily in North America and UK, subject to regional economic and political shifts.

PayPal Holdings, Inc.

- Global presence in ~200 markets exposes it to diverse geopolitical risks and currency fluctuations.

Which company shows a better risk-adjusted profile?

PayPal’s most impactful risk is its heightened market volatility and regulatory scrutiny in global payments. Capital One’s greatest threat lies in weak financial ratios, especially interest coverage, risking funding challenges. Despite PayPal’s volatility, its robust profitability and stronger financial health give it a superior risk-adjusted profile. Capital One’s distressed Altman Z-score and poor profitability metrics justify caution in this credit services cycle.

Final Verdict: Which stock to choose?

Capital One Financial Corporation’s superpower lies in its strong revenue growth and robust cash flow generation, reflecting operational resilience. However, its declining profitability and financial distress signals call for caution. It suits investors with a high-risk tolerance aiming for aggressive growth plays in the financial sector.

PayPal Holdings, Inc. boasts a durable strategic moat through a growing return on invested capital and efficient capital usage. Its solid profitability and healthier balance sheet offer better stability than Capital One. PayPal fits well in portfolios seeking growth at a reasonable price (GARP) with a focus on sustainable competitive advantages.

If you prioritize aggressive growth fueled by rapid top-line expansion and cash flow, Capital One might be the compelling choice despite its risks. However, if you seek a company with a proven moat, consistent profitability, and greater financial stability, PayPal offers a more balanced investment scenario. Each appeals to distinct investor profiles, underscoring the importance of aligning choice with strategy and risk appetite.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Capital One Financial Corporation and PayPal Holdings, Inc. to enhance your investment decisions: