Home > Comparison > Healthcare > BSX vs ZBH

The strategic rivalry between Boston Scientific Corporation and Zimmer Biomet Holdings defines the current trajectory of the medical devices sector. Boston Scientific operates as a diversified, innovation-driven medical device leader, while Zimmer Biomet focuses on musculoskeletal healthcare with a specialized product portfolio. This head-to-head pits broad technological integration against focused orthopedic expertise. This analysis aims to identify which company offers a superior risk-adjusted return for a diversified healthcare portfolio.

Table of contents

Companies Overview

Boston Scientific and Zimmer Biomet stand as key players in the competitive medical devices market.

Boston Scientific Corporation: Innovator in Interventional Medical Devices

Boston Scientific dominates with a diversified portfolio across MedSurg, Rhythm and Neuro, and Cardiovascular segments. Its core revenue comes from advanced devices treating cardiovascular, neurological, and gastrointestinal conditions. In 2026, the company focuses on expanding minimally invasive therapies and enhancing remote patient management systems to maintain its competitive edge.

Zimmer Biomet Holdings, Inc.: Specialist in Musculoskeletal Solutions

Zimmer Biomet excels in orthopaedic reconstructive products including knee, hip, spine, and dental solutions. Its revenue engine hinges on surgical implants and devices that address bone and joint disorders globally. The firm’s strategic priority in 2026 centers on integrating robotics and biologics to complement its traditional implant offerings and broaden clinical application.

Strategic Collision: Similarities & Divergences

Both firms operate in the medical devices sector but differ in focus: Boston Scientific pursues a broad interventional approach, while Zimmer Biomet specializes in musculoskeletal care. Their primary battleground lies in surgical innovation and device adoption. Investors face distinct profiles—Boston Scientific’s scale and diversity contrast with Zimmer Biomet’s niche expertise and targeted growth in orthopaedics.

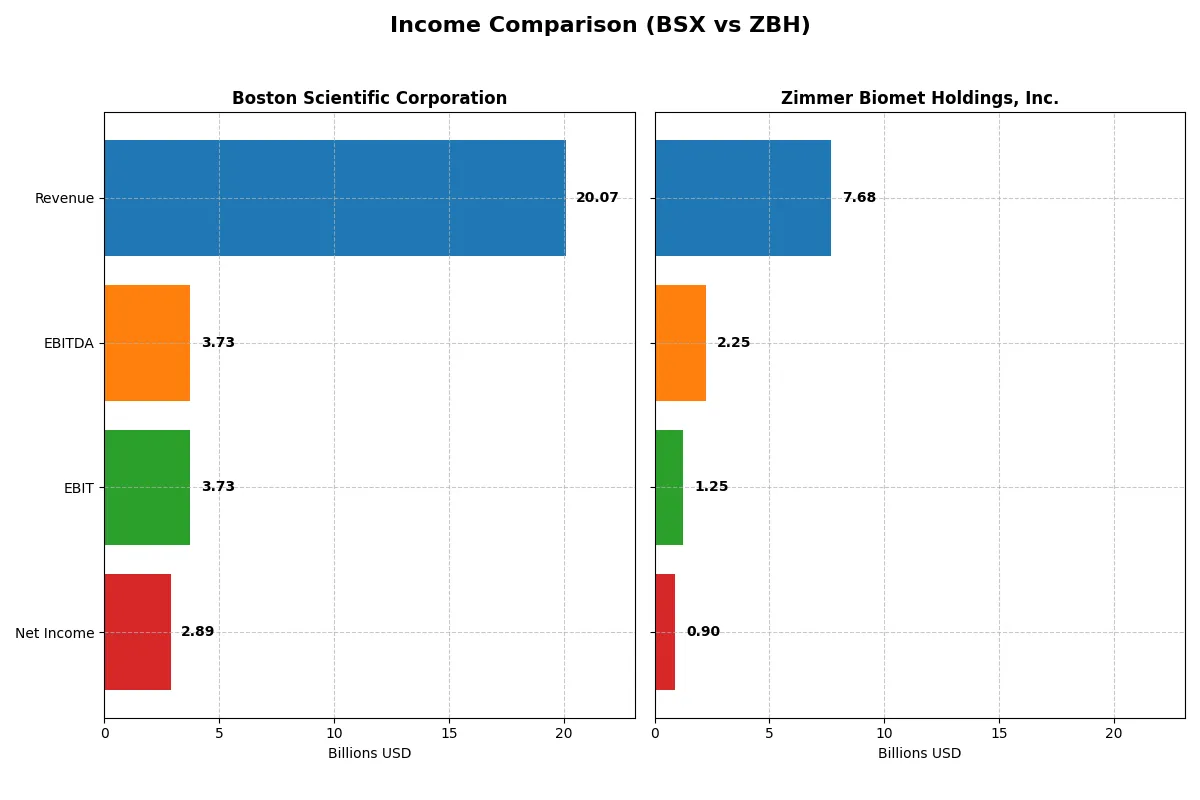

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Boston Scientific Corporation (BSX) | Zimmer Biomet Holdings, Inc. (ZBH) |

|---|---|---|

| Revenue | 20B | 7.68B |

| Cost of Revenue | 6.22B | 2.19B |

| Operating Expenses | 9.88B | 4.20B |

| Gross Profit | 13.85B | 5.49B |

| EBITDA | 3.73B | 2.25B |

| EBIT | 3.73B | 1.25B |

| Interest Expense | 349M | 218M |

| Net Income | 2.89B | 904M |

| EPS | 1.96 | 4.45 |

| Fiscal Year | 2025 | 2024 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals which company converts revenue into profit with superior efficiency and sustainable momentum.

Boston Scientific Corporation Analysis

Boston Scientific’s revenue surged from $11.9B in 2021 to $20.1B in 2025, with net income climbing from $985M to $2.9B. Its gross margin stands strong at 69%, while net margin improved to 14.4%. The 2025 results demonstrate robust efficiency gains and accelerating profitability, reflecting disciplined cost control despite rising operating expenses.

Zimmer Biomet Holdings, Inc. Analysis

Zimmer Biomet’s revenue grew modestly from $6.1B in 2020 to $7.7B in 2024, with net income rebounding to $904M after volatile years. Gross margin remains healthy at 71.5%, but net margin is lower at 11.8%. The latest year shows a slight decline in EBIT and net margin, indicating pressure on operational efficiency and profit conversion.

Verdict: Growth Velocity vs. Margin Resilience

Boston Scientific delivers superior revenue and net income growth with expanding margins, outpacing Zimmer Biomet’s slower expansion and margin contraction. BSX’s scale and accelerating profitability present a stronger fundamental profile. Investors seeking growth backed by improving efficiency will find Boston Scientific’s trajectory more compelling.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of each company:

| Ratios | Boston Scientific (BSX) | Zimmer Biomet (ZBH) |

|---|---|---|

| ROE | 8.5% (2024) | 7.2% (2024) |

| ROIC | 6.1% (2024) | 5.7% (2024) |

| P/E | 70.9x (2024) | 23.7x (2024) |

| P/B | 6.0x (2024) | 1.7x (2024) |

| Current Ratio | 1.08 (2024) | 1.91 (2024) |

| Quick Ratio | 0.64 (2024) | 0.99 (2024) |

| D/E | 0.51 (2024) | 0.50 (2024) |

| Debt-to-Assets | 28.3% (2024) | 29.0% (2024) |

| Interest Coverage | 6.8x (2024) | 5.9x (2024) |

| Asset Turnover | 0.43 (2024) | 0.36 (2024) |

| Fixed Asset Turnover | 4.47 (2024) | 3.75 (2024) |

| Payout Ratio | 0% (2024) | 22% (2024) |

| Dividend Yield | 0% (2024) | 0.91% (2024) |

| Fiscal Year | 2025 | 2024 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios act as a company’s DNA, uncovering hidden risks and operational strengths essential for discerning investors.

Boston Scientific Corporation

Boston Scientific posts a strong net margin of 14.38%, signaling operational efficiency. However, its ROE of 0% and a stretched P/E of 48.91 suggest limited profitability relative to price. The firm does not pay dividends, instead allocating over 10% of revenue to R&D, indicating a growth-focused reinvestment strategy.

Zimmer Biomet Holdings, Inc.

Zimmer Biomet delivers an 11.77% net margin and a moderate ROE of 7.25%, reflecting decent profitability. Its P/E of 23.74 appears fairly valued against sector norms. The company sustains a 0.91% dividend yield, balancing shareholder returns with a moderate R&D spend of about 5.7% of revenue to support innovation.

Premium Valuation vs. Operational Safety

Zimmer Biomet offers a more balanced ratio profile, blending reasonable valuation with steady profitability and shareholder dividends. Boston Scientific’s premium valuation contrasts with zero ROE and absent dividends, fitting investors prioritizing growth over immediate returns.

Which one offers the Superior Shareholder Reward?

Boston Scientific Corporation (BSX) pays no dividend, opting to reinvest free cash flow primarily into growth and innovation, with modest buybacks. Zimmer Biomet Holdings, Inc. (ZBH) yields ~0.9%, with a payout ratio near 22%, supported by robust free cash flow and steady buybacks. Historically, ZBH’s consistent dividends and aggressive share repurchases enhance total shareholder return sustainably. BSX’s zero dividend and limited buybacks suggest a longer runway but more uncertainty for immediate shareholder rewards. I conclude Zimmer Biomet offers a superior total return profile in 2026, balancing income and capital appreciation with a sustainable distribution model.

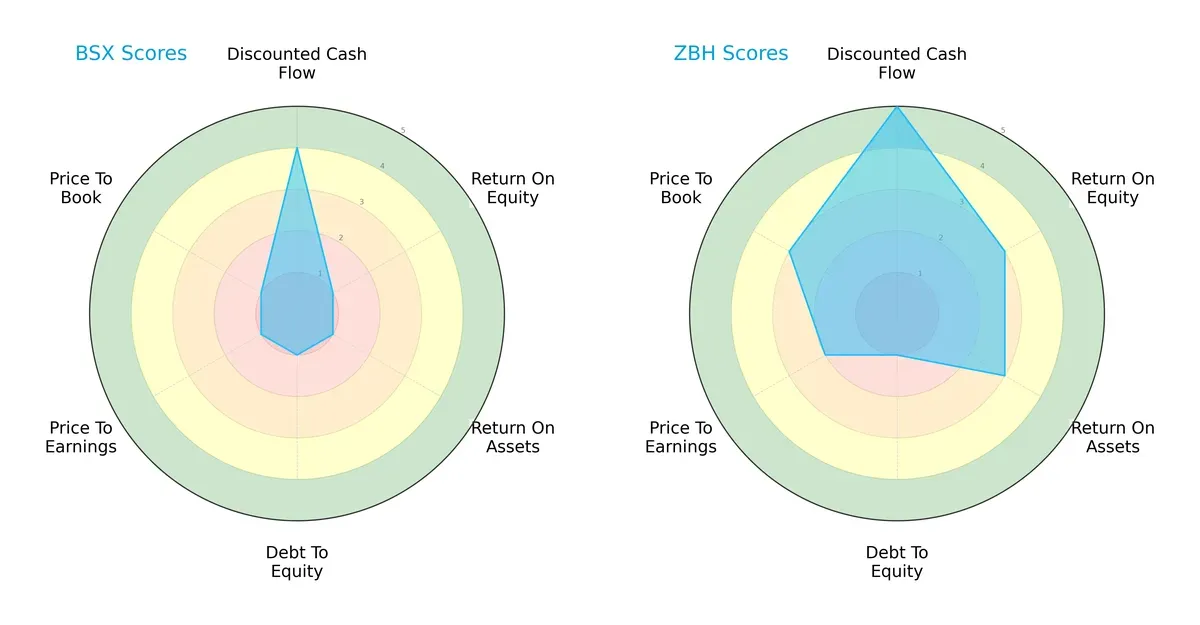

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Boston Scientific Corporation and Zimmer Biomet Holdings, Inc.:

Boston Scientific exhibits a narrow edge in discounted cash flow but scores very low on ROE, ROA, debt-to-equity, and valuation metrics. Zimmer Biomet presents a more balanced profile with moderate ROE and ROA and stronger valuation scores, despite its weak debt-to-equity position. Zimmer leverages operational efficiency, while Boston Scientific depends heavily on cash flow valuation.

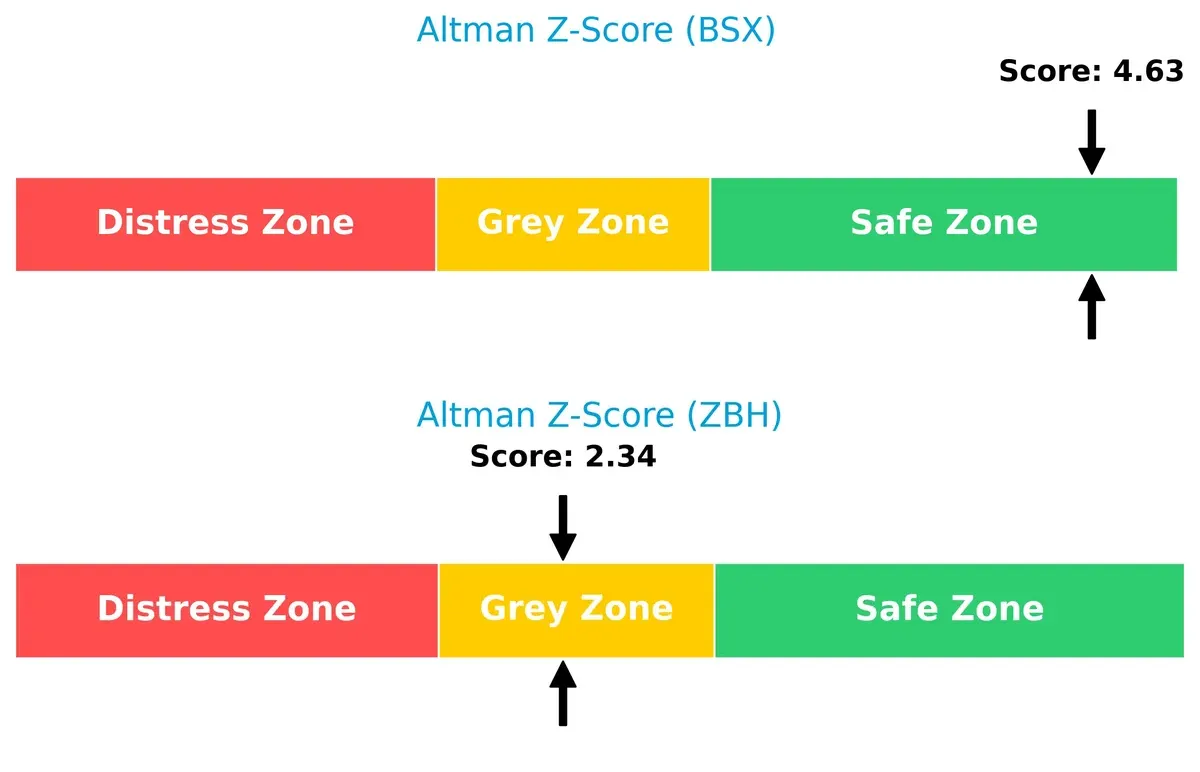

Bankruptcy Risk: Solvency Showdown

Zimmer Biomet’s Altman Z-Score positions it in the grey zone, signaling moderate bankruptcy risk. Boston Scientific scores safely above 4.6, indicating strong long-term financial stability and lower default risk in this cycle:

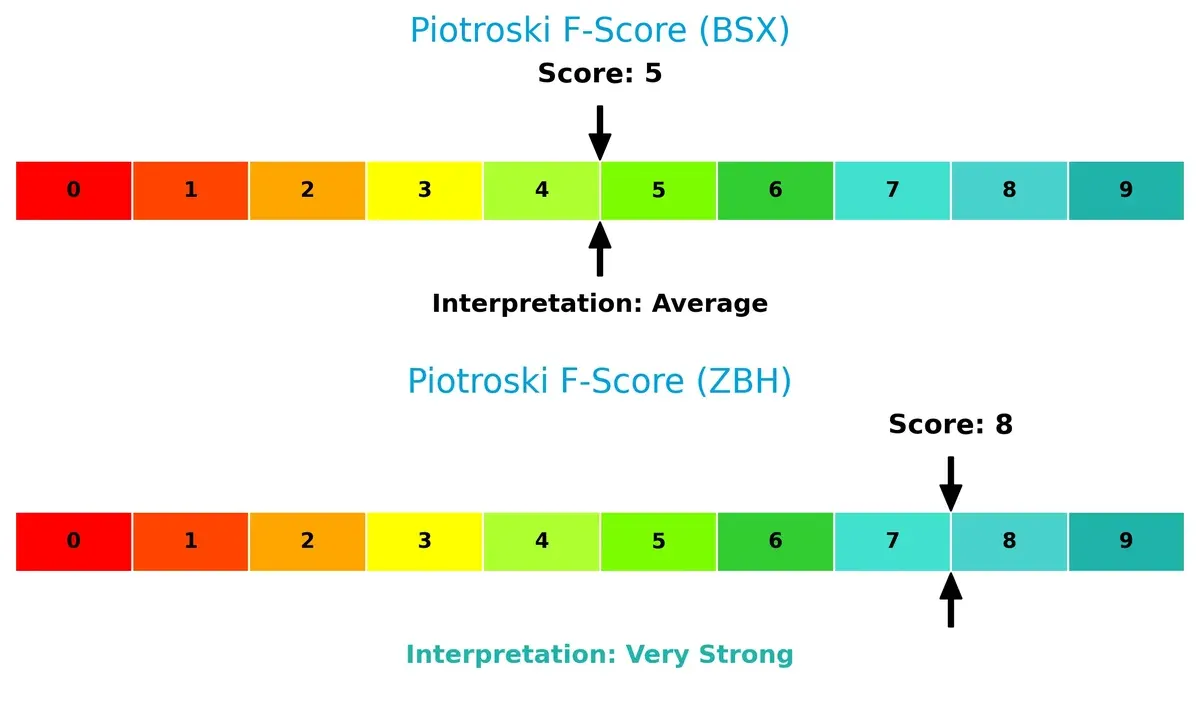

Financial Health: Quality of Operations

Zimmer Biomet’s Piotroski F-Score of 8 signals very strong financial health, reflecting solid profitability and operational efficiency. Boston Scientific’s score of 5 is average, raising caution about internal financial weaknesses compared to its peer:

How are the two companies positioned?

This section dissects the operational DNA of BSX and ZBH by comparing their revenue distribution and internal dynamics, including strengths and weaknesses. The goal is to confront their economic moats and identify which business model offers the most resilient competitive advantage today.

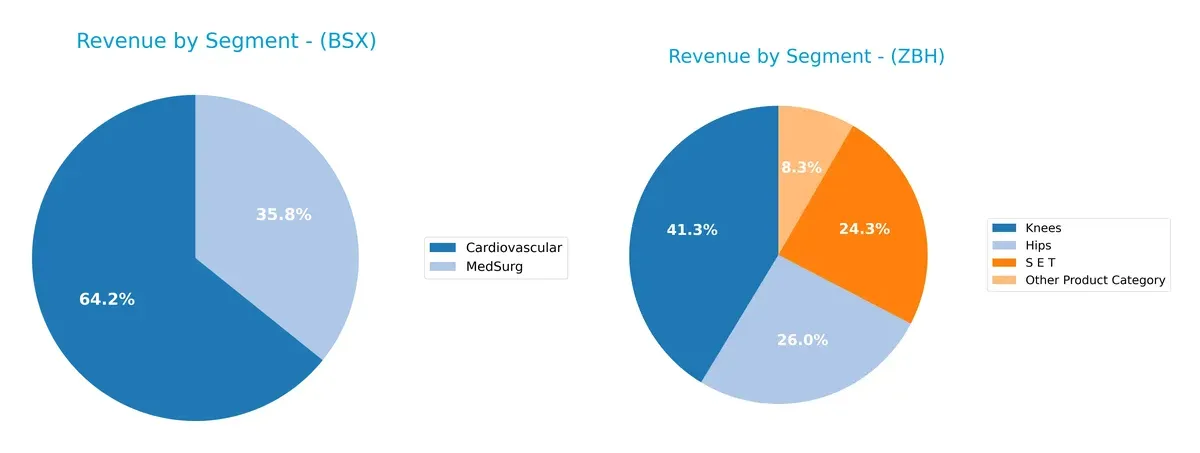

Revenue Segmentation: The Strategic Mix

This comparison dissects how Boston Scientific and Zimmer Biomet diversify their income streams and where their primary sector bets lie:

Boston Scientific leans heavily on Cardiovascular, generating $10.8B in 2024, with MedSurg at $6B. Zimmer Biomet shows a more balanced portfolio: Knees lead at $3.2B, followed by Hips at $2B and S E T at $1.9B. Boston Scientific’s concentration anchors its ecosystem in cardiovascular innovation but risks volatility if that market falters. Zimmer Biomet’s diversified orthopedic mix reduces dependency on a single segment, enhancing resilience.

Strengths and Weaknesses Comparison

This table compares the Strengths and Weaknesses of Boston Scientific Corporation (BSX) and Zimmer Biomet Holdings, Inc. (ZBH):

BSX Strengths

- Strong revenue growth in Cardiovascular segment

- Significant US and Non-US geographic diversification

- Favorable net margin of 14.38%

- Low debt-to-assets ratio and high interest coverage

ZBH Strengths

- Diverse product segments including Hips, Knees, S E T, and Others

- Well-balanced global presence in Americas, Asia Pacific, and EMEA

- Favorable net margin of 11.77%

- Strong current ratio of 1.91 and favorable WACC at 5.75%

BSX Weaknesses

- Unfavorable ROE and ROIC at 0%

- Unavailable WACC data

- High P/E ratio of 48.91 indicating possible overvaluation

- Weak liquidity ratios with current and quick ratios at 0

- Asset and fixed asset turnover unavailable

- No dividend yield

ZBH Weaknesses

- Moderate ROE of 7.25% marked unfavorable

- Neutral ROIC at 5.68%

- Asset turnover low at 0.36

- Dividend yield low at 0.91%

- Quick ratio neutral at 0.99

- P/B ratio neutral at 1.72

Overall, BSX shows strength in profitability and conservative leverage but faces significant liquidity and efficiency challenges. ZBH demonstrates more balanced financial health and diversification but contends with moderate returns and efficiency metrics. Both must address these weaknesses to optimize capital allocation and market positioning.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only reliable shield protecting long-term profits from relentless competition erosion. Here’s how Boston Scientific and Zimmer Biomet defend their turf:

Boston Scientific Corporation: Innovation-Driven Intangible Assets

Boston Scientific relies on innovation and patented medical technologies, reflected in stable margins and strong revenue growth. New cardiovascular and neuro products could deepen its moat in 2026.

Zimmer Biomet Holdings, Inc.: Specialized Orthopedic Expertise

Zimmer Biomet’s moat centers on its deep specialization and surgeon loyalty in orthopedics, contrasting Boston Scientific’s broader device portfolio. Though currently shedding value, its improving ROIC hints at rising competitive strength and expansion potential.

Innovation vs. Specialization: The Moat Showdown

Boston Scientific’s broader innovation moat appears deeper, thanks to superior margin growth and diversified products. Zimmer Biomet shows promise with a focused niche and improving profitability but trails in scale. Boston Scientific stands better poised to defend market share amid evolving healthcare demands.

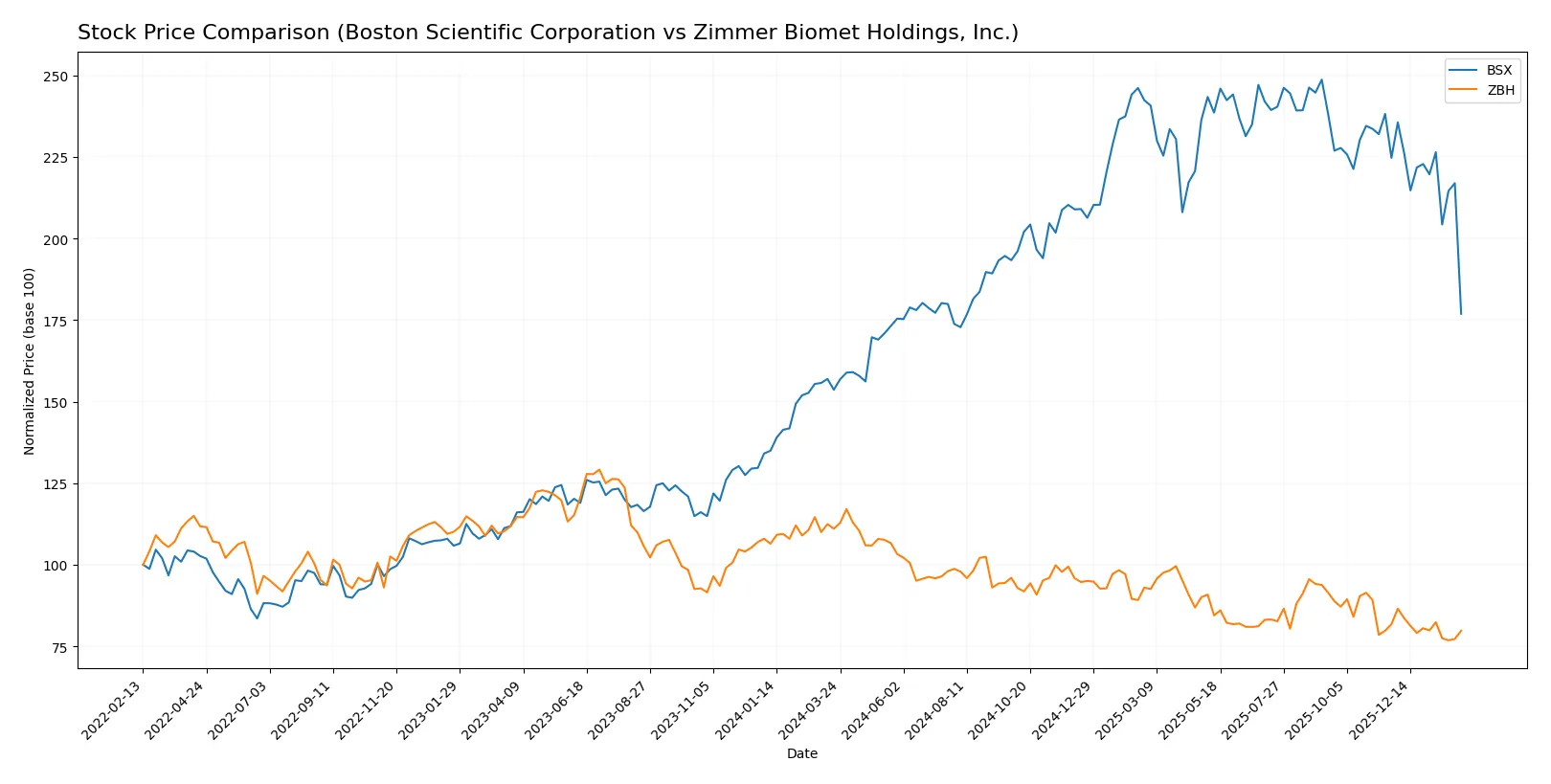

Which stock offers better returns?

The past year shows Boston Scientific’s stock gained 15.16% but with recent deceleration, while Zimmer Biomet declined 28.17%, reflecting sustained bearish pressure and decelerating losses.

Trend Comparison

Boston Scientific’s stock rose 15.16% over the last 12 months, marking a bullish trend with decelerating momentum despite a recent 21.27% drop in the last quarter. Zimmer Biomet’s stock fell 28.17% over the same period, confirming a bearish trend with deceleration and a recent 2.46% decline. Boston Scientific outperformed Zimmer Biomet with stronger overall market performance despite recent volatility.

Target Prices

Analysts set a bullish consensus for Boston Scientific and Zimmer Biomet, suggesting significant upside potential.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Boston Scientific Corporation | 94 | 130 | 108.53 |

| Zimmer Biomet Holdings, Inc. | 86 | 130 | 108 |

Both stocks trade well below consensus targets, implying a 40%+ upside from current prices near $76 and $90 respectively. This gap signals strong analyst confidence despite recent market volatility.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Boston Scientific Corporation Grades

Here are the recent institutional grades for Boston Scientific Corporation:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Canaccord Genuity | Maintain | Buy | 2026-02-05 |

| RBC Capital | Maintain | Outperform | 2026-02-05 |

| JP Morgan | Maintain | Overweight | 2026-02-05 |

| Citigroup | Maintain | Buy | 2026-02-05 |

| TD Cowen | Maintain | Buy | 2026-02-05 |

| UBS | Maintain | Buy | 2026-02-05 |

| Evercore ISI Group | Maintain | Outperform | 2026-02-05 |

| Morgan Stanley | Maintain | Overweight | 2026-02-05 |

| Truist Securities | Maintain | Buy | 2026-02-05 |

| Needham | Maintain | Buy | 2026-02-05 |

Zimmer Biomet Holdings, Inc. Grades

Here are the recent institutional grades for Zimmer Biomet Holdings, Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| UBS | Maintain | Sell | 2026-01-28 |

| Bernstein | Maintain | Market Perform | 2026-01-09 |

| BTIG | Maintain | Buy | 2026-01-08 |

| Evercore ISI Group | Upgrade | Outperform | 2026-01-05 |

| Baird | Downgrade | Neutral | 2025-12-16 |

| Citigroup | Maintain | Neutral | 2025-12-11 |

| Canaccord Genuity | Maintain | Hold | 2025-11-10 |

| UBS | Maintain | Sell | 2025-11-06 |

| JP Morgan | Downgrade | Neutral | 2025-11-06 |

| RBC Capital | Maintain | Outperform | 2025-11-06 |

Which company has the best grades?

Boston Scientific consistently receives positive grades, primarily Buy and Outperform ratings, from multiple firms. Zimmer Biomet’s grades are mixed, with notable Sell and Neutral ratings alongside some Outperform and Buy. Investors may view Boston Scientific’s stronger consensus grades as a sign of broader institutional confidence.

Risks specific to each company

The following categories identify critical pressure points and systemic threats facing Boston Scientific Corporation and Zimmer Biomet Holdings in the 2026 market environment:

1. Market & Competition

Boston Scientific Corporation

- Faces intense competition in diverse medical device segments; innovation pace is crucial to maintain market share.

Zimmer Biomet Holdings, Inc.

- Operates in specialized musculoskeletal and dental markets; competition pressure is moderate but demands continuous product development.

2. Capital Structure & Debt

Boston Scientific Corporation

- Shows favorable debt metrics with low leverage and strong interest coverage, indicating prudent capital management.

Zimmer Biomet Holdings, Inc.

- Maintains moderate debt with a 0.5 debt-to-equity ratio; interest coverage is adequate but debt levels warrant monitoring.

3. Stock Volatility

Boston Scientific Corporation

- Exhibits lower beta (0.657), suggesting less volatility relative to the market; supports risk-averse profiles.

Zimmer Biomet Holdings, Inc.

- Slightly lower beta (0.608) than Boston Scientific, indicating marginally lower stock volatility and steadier price movements.

4. Regulatory & Legal

Boston Scientific Corporation

- Operates globally in highly regulated medical device sectors; regulatory changes could impact product approvals.

Zimmer Biomet Holdings, Inc.

- Also subject to stringent regulations worldwide; legal risks tied to product liability and compliance are material.

5. Supply Chain & Operations

Boston Scientific Corporation

- Complex supply chain spanning diverse device lines; disruption risks heightened by global economic volatility.

Zimmer Biomet Holdings, Inc.

- Supply chain focused on orthopaedic components; less diversified but potentially more resilient due to specialization.

6. ESG & Climate Transition

Boston Scientific Corporation

- Faces moderate ESG risks tied to manufacturing footprint and product lifecycle management; climate initiatives ongoing.

Zimmer Biomet Holdings, Inc.

- ESG efforts focused on sustainable materials and ethical sourcing; climate transition risks manageable but require vigilance.

7. Geopolitical Exposure

Boston Scientific Corporation

- Significant exposure to US and international markets; geopolitical tensions could disrupt supply and sales channels.

Zimmer Biomet Holdings, Inc.

- Operates in Americas, EMEA, and APAC; geopolitical instability in these regions poses moderate risk to operations.

Which company shows a better risk-adjusted profile?

Boston Scientific’s strongest risk lies in its high valuation metrics and operational complexity, which could pressure returns if innovation stalls. Zimmer Biomet faces its greatest risk from moderate debt levels and regulatory challenges. Overall, Zimmer Biomet displays a better risk-adjusted profile, supported by a safer Altman Z-score zone and strong Piotroski score, reflecting stronger financial health and resilience. The disparity in valuation (Boston Scientific’s P/E near 49 vs. Zimmer’s 24) underscores my concern about Boston Scientific’s risk tolerance in a volatile market.

Final Verdict: Which stock to choose?

Boston Scientific’s superpower lies in its robust income growth and operational efficiency, driving strong margins and cash flow expansion. A point of vigilance is its high valuation and declining capital returns, which might suggest stretched expectations. It fits well in an Aggressive Growth portfolio seeking momentum in med-tech innovation.

Zimmer Biomet’s moat is anchored in its steady capital allocation and improving profitability, supported by a safer balance sheet and moderate valuation. Compared to Boston Scientific, it offers better financial stability and a more measured growth trajectory. It suits a GARP portfolio balancing growth potential with prudent risk management.

If you prioritize high-growth momentum and are comfortable with valuation risk, Boston Scientific is the compelling choice due to its superior earnings acceleration. However, if you seek better stability and a healthier balance sheet, Zimmer Biomet offers a more balanced risk-reward profile with a steadily improving moat. Both present distinct analytical scenarios fitting different investor profiles.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Boston Scientific Corporation and Zimmer Biomet Holdings, Inc. to enhance your investment decisions: