Home > Comparison > Healthcare > WST vs BAX

The strategic rivalry between West Pharmaceutical Services, Inc. and Baxter International Inc. shapes the evolution of the healthcare instruments and supplies sector. West operates as a specialized manufacturer of injectable drug containment and delivery systems, while Baxter offers a diversified portfolio spanning dialysis, infusion, and critical care products. This analysis pits West’s focused innovation against Baxter’s broad healthcare platform to identify the superior risk-adjusted opportunity for diversified portfolios.

Table of contents

Companies Overview

West Pharmaceutical Services and Baxter International both hold critical roles in the global healthcare instruments market, shaping drug delivery and patient care solutions.

West Pharmaceutical Services, Inc.: Innovator in Injectable Drug Delivery Systems

West Pharmaceutical Services dominates the injectable drug containment and delivery segment. It generates revenue through proprietary products like stoppers, seals, and custom syringe components, alongside contract manufacturing for medical devices. In 2026, it strategically focuses on expanding integrated solutions, blending advanced packaging technologies with regulatory and technical support to enhance drug safety and efficacy worldwide.

Baxter International Inc.: Comprehensive Healthcare Solutions Provider

Baxter International stands as a diversified healthcare products leader, generating sales from dialysis therapies, intravenous treatments, surgical devices, and connected care technologies. Its 2026 strategy emphasizes expanding critical care and renal therapies, alongside integrated patient monitoring systems, to address complex hospital and homecare needs across roughly 100 countries.

Strategic Collision: Similarities & Divergences

Both companies operate in medical instruments but differ sharply in scope. West centers on a specialized containment and delivery ecosystem, while Baxter pursues a broad healthcare product portfolio with a focus on integrated patient care. Their primary battleground is the injectable and infusion therapy market. West offers depth in drug packaging innovation; Baxter leverages scale and product diversity. These differences define distinct risk profiles and competitive moats in healthcare investing.

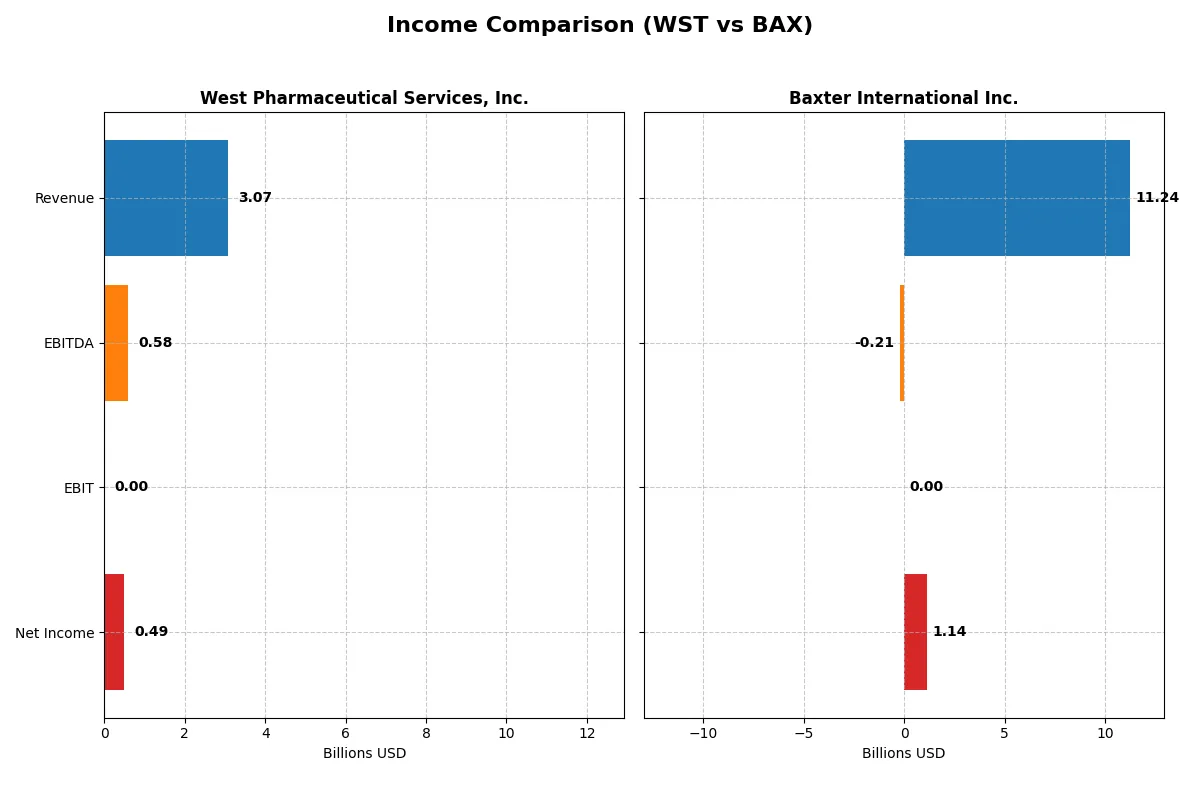

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | West Pharmaceutical Services, Inc. (WST) | Baxter International Inc. (BAX) |

|---|---|---|

| Revenue | 3.07B | 11.24B |

| Cost of Revenue | 1.97B | 7.87B |

| Operating Expenses | 468M | 132M |

| Gross Profit | 1.10B | 3.38B |

| EBITDA | 585M | -206M |

| EBIT | 0 | 0 |

| Interest Expense | 17M | 238M |

| Net Income | 494M | 1.14B |

| EPS | 6.83 | -1.87 |

| Fiscal Year | 2025 | 2025 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals the true efficiency and profitability of two major players in the healthcare sector over recent years.

West Pharmaceutical Services, Inc. Analysis

West Pharmaceutical Services posts steady revenue growth, reaching 3.07B in 2025 with a favorable gross margin of 35.9%. Despite a strong top line, net income declined to 494M, reflecting margin compression. The net margin held at a solid 16.1%, but EBIT margin deteriorated, signaling rising operating costs that erode efficiency.

Baxter International Inc. Analysis

Baxter International reported 11.2B revenue in 2025, growing moderately but with a lower gross margin of 30%. The company suffered an operating loss in 2025, pushing EBIT margin to zero. Yet, net income rebounded to 1.14B, driven by exceptional non-operating items, lifting net margin to 10.1% despite operating challenges.

Margin Strength vs. Earnings Volatility

West shows superior margin control and consistent revenue expansion, but declining net income signals operational strain. Baxter’s revenue scale outpaces West, yet its profitability remains volatile and reliant on non-core gains. For investors, West’s stable margin profile offers more predictability, while Baxter’s profile entails higher risk due to earnings instability.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | West Pharmaceutical Services, Inc. (WST) | Baxter International Inc. (BAX) |

|---|---|---|

| ROE | 18.4% (2024) | 18.5% (2025) |

| ROIC | 15.7% (2024) | -0.04% (2025) |

| P/E | 48.5x (2024) | 8.6x (2025) |

| P/B | 8.9x (2024) | 1.6x (2025) |

| Current Ratio | 2.79 (2024) | 2.31 (2025) |

| Quick Ratio | 2.11 (2024) | 1.56 (2025) |

| D/E | 0.11 (2024) | 1.58 (2025) |

| Debt-to-Assets | 8.4% (2024) | 48.4% (2025) |

| Interest Coverage | 205.0 (2024) | -0.03 (2025) |

| Asset Turnover | 0.79 (2024) | 0.02 (2025) |

| Fixed Asset Turnover | 1.72 (2024) | 0.11 (2025) |

| Payout ratio | 12.0% (2024) | 30.6% (2025) |

| Dividend yield | 0.25% (2024) | 3.55% (2025) |

| Fiscal Year | 2024 | 2025 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios serve as a company’s DNA, exposing hidden risks and operational excellence critical for informed investment decisions.

West Pharmaceutical Services, Inc.

West Pharmaceutical exhibits a solid net margin of 16.06%, indicating operational strength despite a lack of reported ROE and ROIC, which raises concerns. The stock trades at a high P/E of 40.29, signaling stretched valuation. Dividend yield is minimal at 0.31%, suggesting modest shareholder returns, with reinvestment likely focused on R&D and growth.

Baxter International Inc.

Baxter International reports a striking net margin of 322.73% and a strong ROE at 18.53%, reflecting pronounced profitability and efficient capital use. Its P/E ratio of 8.63 identifies the stock as attractively valued. The company delivers a healthy 3.55% dividend yield, balancing shareholder returns with some debt leverage, as debt-to-equity stands unfavorable at 1.58.

Premium Valuation vs. Operational Safety

Baxter offers a better balance of profitability and valuation, with favorable margins and a compelling dividend, despite moderate debt. West’s stretched multiples and missing profitability metrics increase investment risk. Baxter suits income-focused investors, while West may appeal to those prioritizing growth and innovation.

Which one offers the Superior Shareholder Reward?

I compare West Pharmaceutical Services (WST) and Baxter International (BAX) by their dividend yields, payout ratios, and buyback intensity. WST yields 0.31% with a 12% payout ratio, signaling strong free cash flow coverage and conservative distribution. It complements dividends with moderate buybacks, sustaining long-term value. BAX offers a 3.55% yield but with a volatile payout and negative free cash flow, raising sustainability concerns. Its heavy debt load and inconsistent cash generation limit buybacks, risking shareholder returns. I find WST’s balanced, sustainable model superior for total shareholder reward in 2026.

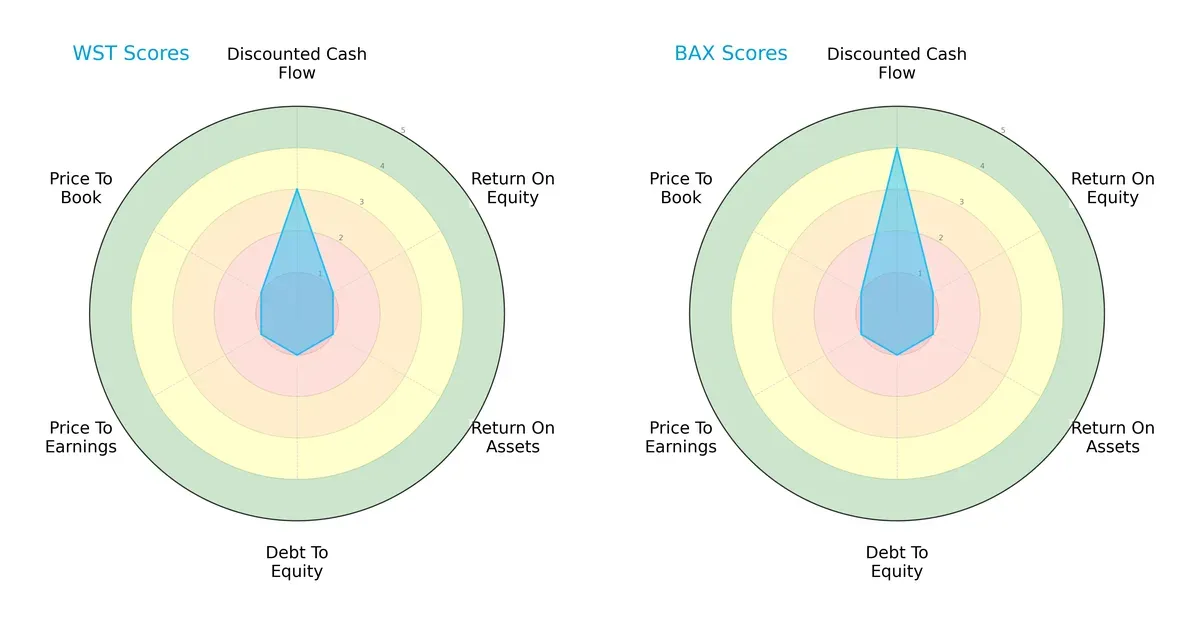

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of West Pharmaceutical Services and Baxter International Inc., highlighting their core financial strengths and weaknesses:

Both companies carry very unfavorable scores in ROE, ROA, Debt/Equity, P/E, and P/B ratios, indicating financial challenges. Baxter edges West slightly with a more favorable discounted cash flow score (4 vs. 3). Neither firm presents a balanced profile; West and Baxter both rely on weak profitability and valuation metrics, signaling caution for investors seeking stability.

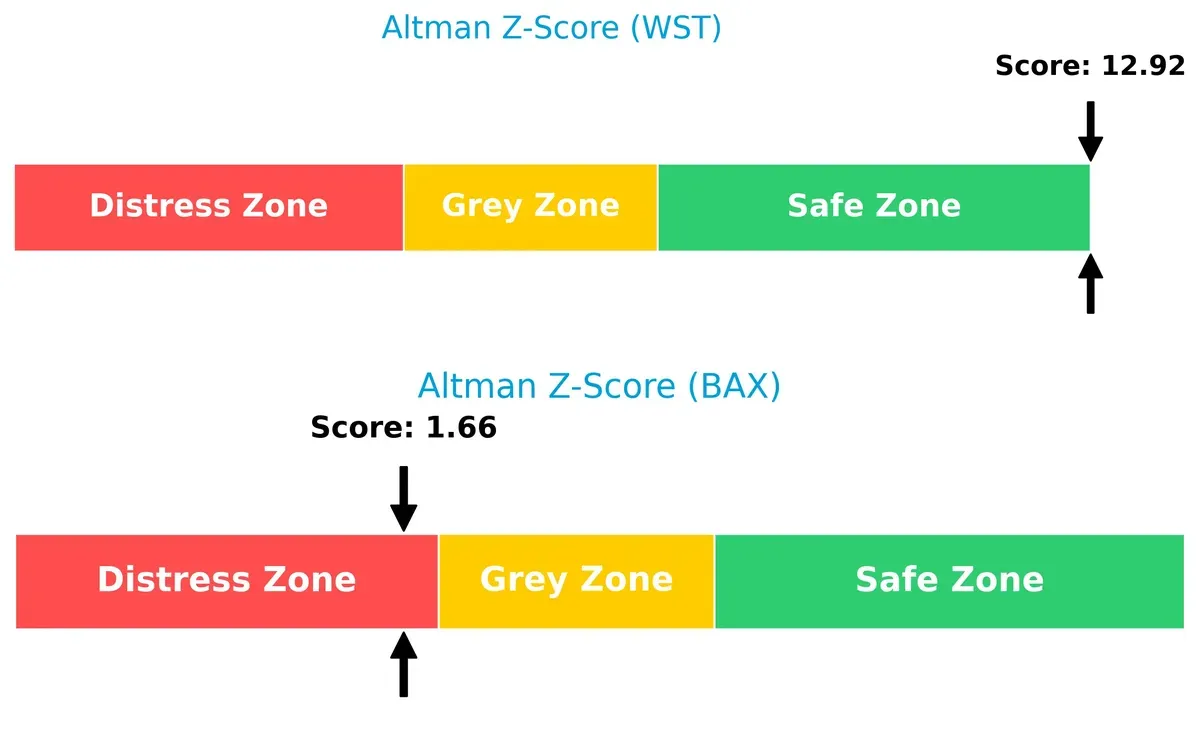

Bankruptcy Risk: Solvency Showdown

West Pharmaceutical’s Altman Z-Score of 12.9 places it firmly in the safe zone, contrasting sharply with Baxter’s 1.66 in the distress zone. This wide delta signals West’s superior long-term solvency and a significantly lower bankruptcy risk in the current cycle:

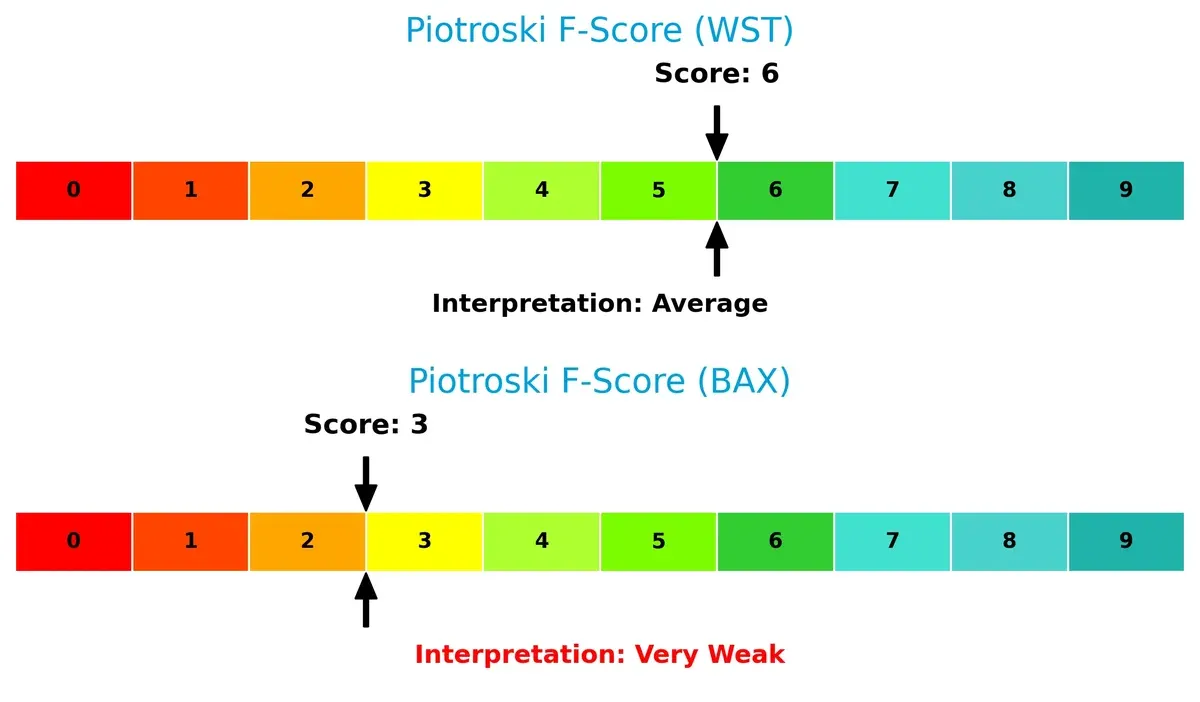

Financial Health: Quality of Operations

West’s Piotroski F-Score of 6 suggests average financial health and operational quality. Baxter’s score of 3 flags very weak fundamentals and potential red flags in profitability and liquidity, underscoring West’s stronger internal metrics:

How are the two companies positioned?

This section dissects the operational DNA of West Pharmaceutical Services and Baxter International by comparing their revenue distribution and internal dynamics. The goal is to confront their economic moats and identify which model offers the most resilient, sustainable competitive advantage today.

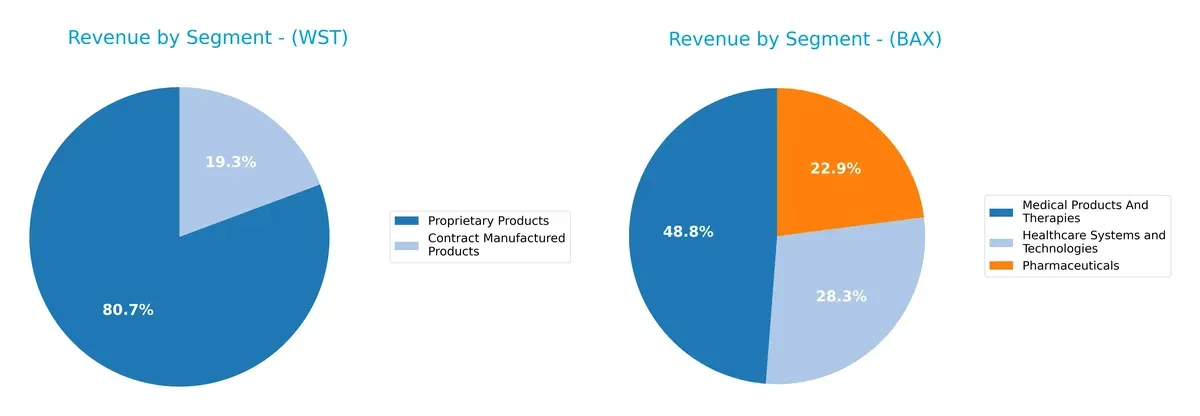

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how West Pharmaceutical Services and Baxter International diversify their income streams and where their primary sector bets lie:

West Pharmaceutical Services anchors revenue in Proprietary Products with $2.33B in 2024, supplemented by $559M in Contract Manufactured Products. Baxter International dwarfs this with a broader mix: $5.21B from Medical Products and Therapies, $2.41B Pharmaceuticals, and $2.95B Healthcare Systems and Technologies in 2024. Baxter’s diversified portfolio reduces concentration risk, while West pivots heavily on proprietary innovation, exposing it to sector-specific shifts. Baxter’s ecosystem lock-in drives steady growth across multiple healthcare verticals.

Strengths and Weaknesses Comparison

This table compares the strengths and weaknesses of West Pharmaceutical Services, Inc. (WST) and Baxter International Inc. (BAX):

WST Strengths

- Strong proprietary products revenue of 2.33B USD

- Favorable net margin at 16.06% indicates profitability

- Low debt-to-assets ratio suggests conservative leverage

- Established US and European market presence

BAX Strengths

- Highly diversified product segments exceeding 10B USD total revenue

- Strong net margin at 322.73% and ROE at 18.53% show robust profitability

- Favorable current and quick ratios indicate strong liquidity

- Global footprint with significant US and EMEA sales

WST Weaknesses

- Unfavorable ROE and ROIC at 0% reflect poor capital efficiency

- Unavailable WACC limits cost of capital assessment

- Poor liquidity with current and quick ratios at 0

- High P/E ratio of 40.29 may imply overvaluation

- Negative interest coverage signals financial risk

BAX Weaknesses

- Negative ROIC at -0.04% shows capital allocation concerns

- High debt-to-equity ratio of 1.58 indicates leverage risk

- Unfavorable interest coverage and asset turnover ratios

- Moderate P/B ratio at 1.6 suggests fair valuation

WST demonstrates solid profitability and conservative leverage but faces capital efficiency challenges and liquidity concerns. BAX’s broad diversification and strong profitability contrast with some leverage and capital allocation weaknesses, shaping distinct strategic priorities for both companies.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only true defense protecting long-term profits from relentless competitive erosion. Here’s how West Pharmaceutical and Baxter International compare:

West Pharmaceutical Services, Inc.: Specialized Intangible Assets Moat

West’s moat centers on proprietary drug containment and delivery technologies, reflected in stable gross margins near 36%. However, declining ROIC signals pressure on capital efficiency in 2026.

Baxter International Inc.: Broad Product Portfolio and Scale Moat

Baxter’s moat relies on diversified healthcare products and global scale, but its negative ROIC spread versus WACC reveals value destruction. Margin volatility challenges its competitive positioning amid market shifts.

Specialized Innovation vs. Scale Efficiency: Who Defends Better?

West’s intangible asset moat offers deeper specialization but faces capital return headwinds. Baxter’s scale is broad but financially less efficient. West is better positioned to protect market share through focused innovation.

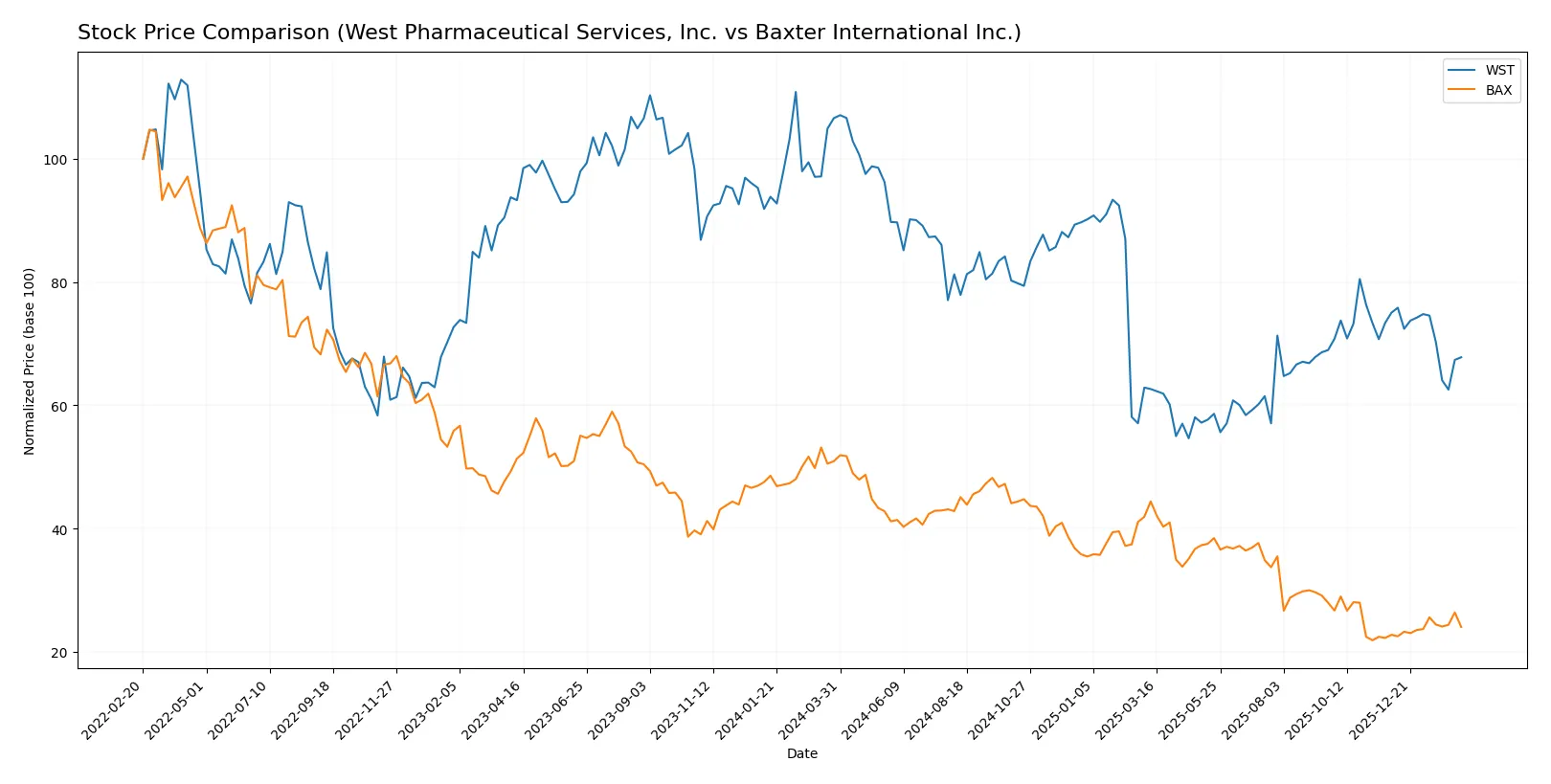

Which stock offers better returns?

The past year shows divergent paths: West Pharmaceutical’s stock declines sharply with decelerating losses, while Baxter International’s stock falls steeply overall but rebounds recently with mild gains.

Trend Comparison

West Pharmaceutical Services, Inc. shows a 36.41% price decline over 12 months, indicating a bearish trend with decelerating losses and a high volatility level (std. dev. 50.53). The recent quarter confirms continued weakness with a 9.65% drop.

Baxter International Inc. suffers a 52.81% drop over the year, a bearish trend but with accelerating losses. Volatility remains low (std. dev. 6.66). Notably, the recent quarter reverses course with a 5.6% gain and a mild positive slope.

Comparing trends, Baxter’s stock delivered the weakest yearly performance but shows recent recovery, while West’s losses have slowed. Overall, West’s decline is less severe than Baxter’s.

Target Prices

Analysts show a bullish consensus for both West Pharmaceutical Services and Baxter International.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| West Pharmaceutical Services, Inc. | 265 | 340 | 304.43 |

| Baxter International Inc. | 15 | 25 | 20.71 |

West Pharmaceutical’s consensus target exceeds its current price by over 21%, signaling strong growth expectations. Baxter’s target sits slightly above its current price, reflecting moderate upside potential.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

West Pharmaceutical Services, Inc. Grades

The latest institutional grades for West Pharmaceutical Services, Inc. are detailed here:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Barclays | Maintain | Equal Weight | 2026-02-13 |

| Evercore ISI Group | Maintain | Outperform | 2026-02-03 |

| Barclays | Maintain | Equal Weight | 2025-10-27 |

| Keybanc | Maintain | Overweight | 2025-10-24 |

| UBS | Maintain | Buy | 2025-10-24 |

| Evercore ISI Group | Maintain | Outperform | 2025-10-23 |

| Barclays | Maintain | Equal Weight | 2025-10-02 |

| Barclays | Maintain | Equal Weight | 2025-07-25 |

| UBS | Maintain | Buy | 2025-07-25 |

| Evercore ISI Group | Maintain | Outperform | 2025-07-25 |

Baxter International Inc. Grades

The institutional grades for Baxter International Inc. from leading firms are summarized below:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Barclays | Maintain | Overweight | 2026-02-13 |

| Barclays | Maintain | Overweight | 2026-01-09 |

| Morgan Stanley | Maintain | Underweight | 2025-12-02 |

| Citigroup | Maintain | Neutral | 2025-10-31 |

| UBS | Maintain | Neutral | 2025-10-31 |

| Argus Research | Downgrade | Hold | 2025-10-31 |

| Goldman Sachs | Maintain | Neutral | 2025-10-31 |

| Evercore ISI Group | Maintain | Outperform | 2025-10-07 |

| Barclays | Maintain | Overweight | 2025-08-04 |

| Stifel | Downgrade | Hold | 2025-08-04 |

Which company has the best grades?

West Pharmaceutical Services holds consistently stronger grades, including multiple “Outperform” and “Buy” ratings. Baxter International shows mixed signals with more “Neutral” and some downgrades. This contrast may influence investor confidence and portfolio positioning.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

West Pharmaceutical Services, Inc.

- Faces intense competition in injectable drug delivery systems; innovation critical to maintain market share.

Baxter International Inc.

- Competes across diverse healthcare products; must manage competitive pressures in dialysis and critical care markets.

2. Capital Structure & Debt

West Pharmaceutical Services, Inc.

- Maintains low debt levels, a favorable sign for financial stability and flexibility.

Baxter International Inc.

- Carries higher debt-to-equity (1.58), increasing financial risk and interest burden.

3. Stock Volatility

West Pharmaceutical Services, Inc.

- Exhibits moderate beta (1.19), implying sensitivity to market swings but with growth potential.

Baxter International Inc.

- Lower beta (0.585) indicates reduced volatility and defensive stock characteristics.

4. Regulatory & Legal

West Pharmaceutical Services, Inc.

- Must navigate strict medical device regulations globally; recalls could impact reputation.

Baxter International Inc.

- Faces complex regulations across multiple product lines; compliance failures pose material risks.

5. Supply Chain & Operations

West Pharmaceutical Services, Inc.

- Global manufacturing footprint; supply chain disruptions could impair delivery timelines.

Baxter International Inc.

- Extensive operations with reliance on third-party suppliers; vulnerable to geopolitical and logistical risks.

6. ESG & Climate Transition

West Pharmaceutical Services, Inc.

- ESG initiatives improving but lack detailed disclosure; transition risks remain.

Baxter International Inc.

- Increasing focus on sustainability; stronger reporting may attract ESG-focused investors.

7. Geopolitical Exposure

West Pharmaceutical Services, Inc.

- Exposure to multiple global markets; geopolitical tensions could disrupt supply or sales.

Baxter International Inc.

- Operates in ~100 countries; geopolitical instability in emerging markets could affect revenues.

Which company shows a better risk-adjusted profile?

West Pharmaceutical Services faces significant operational and market risks but benefits from a strong balance sheet and lower debt. Baxter International carries higher debt and financial leverage risks, compounded by weaker liquidity ratios and distress signals in bankruptcy risk scores. However, Baxter’s lower stock volatility and broader product diversification provide some defensive buffer. The standout risk for West is its unfavorable profitability ratios despite a safe Altman Z-score. Baxter’s critical vulnerability lies in its distress-zone Altman Z-score and very weak Piotroski score, signaling potential financial instability. Considering these factors, West Pharmaceutical presents a better risk-adjusted profile, supported by its robust Altman Z-score of 12.9, whereas Baxter lingers in the distress zone at 1.66, justifying heightened caution.

Final Verdict: Which stock to choose?

West Pharmaceutical Services, Inc. boasts a superpower in operational cash generation with steady revenue growth and solid gross margins. Its main point of vigilance is declining profitability metrics and a stretched valuation, which may pressure future returns. It fits an aggressive growth portfolio seeking exposure to medical device innovation.

Baxter International Inc. leverages a strategic moat through diversified healthcare product lines and solid dividend yield, offering a recurring revenue safety net. Compared to West, Baxter presents a more conservative profile with better liquidity but suffers from value destruction signs and uneven profitability. It suits a GARP (Growth at a Reasonable Price) portfolio balancing income and stability.

If you prioritize growth backed by cash generation and can tolerate valuation risks, West outshines as the compelling choice due to its operational efficiency. However, if you seek better stability and income with a defensive stance, Baxter offers superior dividend yield and liquidity despite its value challenges. Both require careful risk monitoring given their recent financial headwinds.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of West Pharmaceutical Services, Inc. and Baxter International Inc. to enhance your investment decisions: