In the fast-evolving semiconductor industry, Arm Holdings plc and Cirrus Logic, Inc. stand out as key innovators shaping technology’s future. Arm focuses on CPU architecture and licensing, powering a broad range of devices globally, while Cirrus Logic excels in mixed-signal processing for audio and industrial applications. This article compares their market positions and innovation strategies to help you decide which company deserves a place in your investment portfolio.

Table of contents

Companies Overview

I will begin the comparison between Arm Holdings plc American Depositary Shares (ARM) and Cirrus Logic, Inc. (CRUS) by providing an overview of these two companies and their main differences.

Arm Holdings plc Overview

Arm Holdings plc, headquartered in Cambridge, UK, is a technology company specializing in designing and licensing central processing unit products and related technologies. Founded in 1990, Arm’s microprocessors and system IPs serve various markets including automotive, computing infrastructure, consumer technologies, and IoT. The company operates globally and functions as a subsidiary of Kronos II LLC, with a market cap of approximately 111B USD.

Cirrus Logic, Inc. Overview

Cirrus Logic, based in Austin, Texas, is a fabless semiconductor firm focused on low-power, high-precision mixed-signal processing solutions. Established in 1984, Cirrus offers codecs, amplifiers, DSPs, and SoundClear audio technology for consumer electronics like smartphones and automotive audio systems, as well as industrial applications. The company has a market cap near 6.3B USD and sells through direct and indirect channels.

Key similarities and differences

Both ARM and Cirrus Logic operate in the semiconductor industry and provide technology crucial to consumer and industrial electronics. ARM primarily licenses CPU designs and system IPs globally, targeting broad applications including IoT and automotive markets. Cirrus Logic focuses on mixed-signal audio and power management ICs, delivering integrated solutions for audio performance and industrial controls, with a stronger emphasis on fabless manufacturing and direct sales.

Income Statement Comparison

Below is a side-by-side comparison of the latest fiscal year income statement metrics for Arm Holdings plc and Cirrus Logic, Inc.

| Metric | Arm Holdings plc American Depositary Shares | Cirrus Logic, Inc. |

|---|---|---|

| Market Cap | 111B | 6.3B |

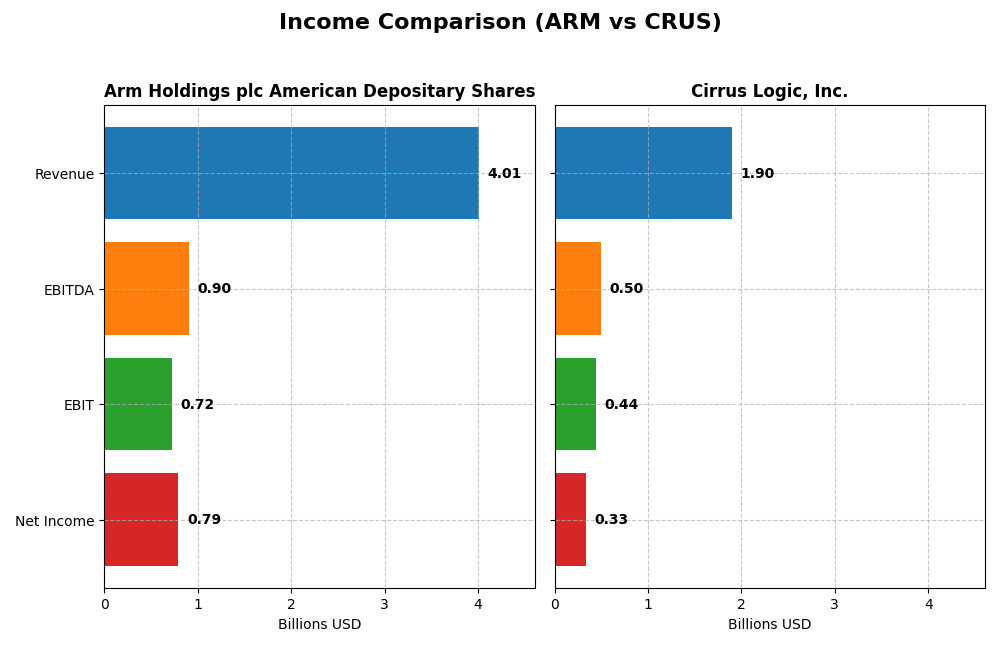

| Revenue | 4.01B | 1.90B |

| EBITDA | 903M | 497M |

| EBIT | 720M | 445M |

| Net Income | 792M | 332M |

| EPS | 0.75 | 6.24 |

| Fiscal Year | 2025 | 2025 |

Income Statement Interpretations

Arm Holdings plc American Depositary Shares

Arm Holdings showed strong revenue growth from 2.03B in 2021 to 4.01B in 2025, nearly doubling over five years. Net income rose from 388M to 792M, reflecting solid profitability improvements. Margins remained robust, with a gross margin near 95% and net margin around 20% in 2025. The latest year saw a 24% revenue increase and more than doubled EBIT, signaling strong operational leverage and margin expansion.

Cirrus Logic, Inc.

Cirrus Logic’s revenue increased from 1.37B in 2021 to 1.90B in 2025, a more modest 39% rise over the period. Net income grew steadily from 217M to 332M. Margins held favorably, with a gross margin above 52% and a net margin near 17.5% in 2025. The most recent year showed moderate 6% revenue growth but stronger EBIT and net margin improvements, indicating effective expense management and profitability gains.

Which one has the stronger fundamentals?

Both companies present favorable income statement fundamentals with over 90% positive evaluations. Arm exhibits higher revenue and net income growth rates and superior gross margins close to 95%, indicating strong pricing power and operational efficiency. Cirrus Logic maintains solid margins and steady growth but at a slower pace. Arm’s more pronounced margin expansion and earnings growth suggest relatively stronger fundamentals based solely on income statement metrics.

Financial Ratios Comparison

The table below presents the most recent financial ratios for Arm Holdings plc and Cirrus Logic, Inc., providing a clear basis for comparison across key performance and financial health indicators.

| Ratios | Arm Holdings plc (ARM) | Cirrus Logic, Inc. (CRUS) |

|---|---|---|

| ROE | 11.58% | 17.01% |

| ROIC | 10.28% | 14.20% |

| P/E | 141.58 | 15.95 |

| P/B | 16.40 | 2.71 |

| Current Ratio | 5.20 | 6.35 |

| Quick Ratio | 5.20 | 4.82 |

| D/E (Debt to Equity) | 5.21% | 7.37% |

| Debt-to-Assets | 3.99% | 6.18% |

| Interest Coverage | 0 | 457.0 |

| Asset Turnover | 0.45 | 0.81 |

| Fixed Asset Turnover | 5.61 | 6.62 |

| Payout ratio | 0 | 0 |

| Dividend yield | 0 | 0 |

Interpretation of the Ratios

Arm Holdings plc American Depositary Shares

Arm Holdings shows a mix of strong and weak ratios, with a notably high price-to-earnings ratio of 141.58 and a low return on invested capital at 10.28%, both unfavorable signals. Its debt levels and interest coverage are favorable, indicating low financial risk. The company does not pay dividends, reflecting a focus on reinvestment and growth rather than shareholder payouts presently.

Cirrus Logic, Inc.

Cirrus Logic exhibits generally strong ratios, including a favorable return on equity of 17.01% and a solid net margin of 17.48%. Its valuation multiples and debt metrics are mostly neutral to favorable, although its current ratio is less ideal. Like Arm, Cirrus Logic does not distribute dividends, likely prioritizing reinvestment and operational expansion over cash returns to shareholders.

Which one has the best ratios?

Cirrus Logic holds a more favorable overall ratio profile, with 57.14% favorable ratios compared to Arm’s 42.86%. Arm faces challenges with valuation and efficiency metrics, whereas Cirrus balances profitability and financial health more effectively. Both companies avoid dividends, focusing on growth, but Cirrus’s stronger returns and lower risks give it an edge in ratio strength.

Strategic Positioning

This section compares the strategic positioning of Arm Holdings plc and Cirrus Logic, Inc., focusing on market position, key segments, and exposure to technological disruption:

Arm Holdings plc American Depositary Shares

- Large market cap of 111B USD with high beta of 4.36 indicating high competitive pressure in semiconductors.

- Focuses on licensing CPUs, GPUs, and IP for automotive, computing infrastructure, consumer tech, and IoT markets.

- Operates globally with products embedded in numerous devices, implying significant exposure to rapid semiconductor technological changes.

Cirrus Logic, Inc.

- Smaller market cap of 6.3B USD with beta near 1.08 reflecting moderate competitive pressure in semiconductors.

- Specializes in low-power mixed-signal processing for portable audio and high-performance industrial applications.

- Focused on mixed-signal and audio processing ICs, with exposure to evolving portable and industrial electronics technologies.

Arm Holdings plc vs Cirrus Logic, Inc. Positioning

Arm pursues a diversified business model through licensing across multiple high-growth markets, while Cirrus Logic concentrates on audio and mixed-signal ICs. Arm’s scale supports broad reach but faces intense competition; Cirrus Logic’s niche focus targets specialized segments with less market breadth.

Which has the best competitive advantage?

Cirrus Logic shows a very favorable MOAT with ROIC exceeding WACC and a growing trend, indicating durable value creation. Arm’s MOAT is unfavorable with ROIC below WACC, suggesting value destruction despite stable profitability.

Stock Comparison

The stock price movements of Arm Holdings plc American Depositary Shares (ARM) and Cirrus Logic, Inc. (CRUS) over the past 12 months reveal contrasting dynamics, with ARM experiencing a significant decline and CRUS showing notable gains, despite recent downward adjustments.

Trend Analysis

Arm Holdings plc’s stock displayed a bearish trend over the past year, with a price decrease of 21.17%. The trend decelerated, showing high volatility (std deviation 19.31) and a recent sharper decline of 38.11% from November 2025 to January 2026.

Cirrus Logic, Inc.’s stock demonstrated a bullish trend across the last 12 months, rising 34.06%, although the upward momentum decelerated. Recent weeks showed a mild 7.06% drop with reduced volatility (std deviation 3.68).

Comparing both, Cirrus Logic delivered the highest market performance over the analyzed period, contrasting with Arm Holdings’ significant depreciation and recent seller dominance in volume.

Target Prices

Analysts present a clear target price consensus for Arm Holdings plc and Cirrus Logic, Inc., reflecting positive market expectations.

| Company | Target High | Target Low | Consensus |

|---|---|---|---|

| Arm Holdings plc American Depositary Shares | 210 | 120 | 166 |

| Cirrus Logic, Inc. | 155 | 100 | 138.75 |

The consensus target prices for both companies are significantly above their current stock prices ($105.11 for Arm and $123.28 for Cirrus Logic), indicating optimistic analyst outlooks and potential upside for investors.

Analyst Opinions Comparison

This section compares analysts’ ratings and grades for Arm Holdings plc American Depositary Shares (ARM) and Cirrus Logic, Inc. (CRUS):

Rating Comparison

ARM Rating

- Rating: B, classified as Very Favorable

- Discounted Cash Flow Score: 3, Moderate

- ROE Score: 3, Moderate

- ROA Score: 4, Favorable

- Debt To Equity Score: 4, Favorable

- Overall Score: 3, Moderate

CRUS Rating

- Rating: A-, classified as Very Favorable

- Discounted Cash Flow Score: 4, Favorable

- ROE Score: 4, Favorable

- ROA Score: 5, Very Favorable

- Debt To Equity Score: 3, Moderate

- Overall Score: 4, Favorable

Which one is the best rated?

Based strictly on the provided data, CRUS holds a higher rating of A- and scores more favorably across most financial metrics, including discounted cash flow, ROE, ROA, and overall score, compared to ARM’s B rating and moderate scores.

Scores Comparison

Here is the comparison of Arm and Cirrus Logic scores based on the Altman Z-Score and Piotroski Score:

Arm Scores

- Altman Z-Score: 32.43, indicating safe zone with very low bankruptcy risk.

- Piotroski Score: 7, classified as strong financial health.

Cirrus Logic Scores

- Altman Z-Score: 11.94, indicating safe zone with low bankruptcy risk.

- Piotroski Score: 7, classified as strong financial health.

Which company has the best scores?

Both Arm and Cirrus Logic have strong Piotroski Scores of 7, reflecting solid financial health. Arm has a considerably higher Altman Z-Score, signaling a stronger buffer against bankruptcy risk compared to Cirrus Logic.

Grades Comparison

Here is a detailed comparison of the recent grades assigned to Arm Holdings plc and Cirrus Logic, Inc.:

Arm Holdings plc Grades

The following table summarizes Arm’s recent grades from reputable grading companies:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| B of A Securities | Downgrade | Neutral | 2026-01-13 |

| B of A Securities | Maintain | Buy | 2025-12-16 |

| Goldman Sachs | Downgrade | Sell | 2025-12-15 |

| Loop Capital | Maintain | Buy | 2025-11-12 |

| TD Cowen | Maintain | Buy | 2025-11-06 |

| Rosenblatt | Maintain | Buy | 2025-11-06 |

| Wells Fargo | Maintain | Overweight | 2025-11-06 |

| Mizuho | Maintain | Outperform | 2025-11-06 |

| Barclays | Maintain | Overweight | 2025-11-06 |

| UBS | Maintain | Buy | 2025-11-06 |

Arm Holdings shows a majority of buy and outperform ratings, though recent downgrades to neutral and sell indicate some caution.

Cirrus Logic, Inc. Grades

The following table outlines Cirrus Logic’s recent grades from verified grading firms:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Keybanc | Maintain | Overweight | 2025-11-05 |

| Barclays | Maintain | Equal Weight | 2025-11-05 |

| Stifel | Maintain | Buy | 2025-11-05 |

| Benchmark | Maintain | Buy | 2025-11-05 |

| Susquehanna | Maintain | Positive | 2025-10-22 |

| Stifel | Maintain | Buy | 2025-10-17 |

| Stifel | Maintain | Buy | 2025-09-12 |

| Barclays | Maintain | Equal Weight | 2025-05-07 |

| Barclays | Maintain | Equal Weight | 2025-04-22 |

| Stifel | Maintain | Buy | 2025-04-17 |

Cirrus Logic maintains mostly buy and equal weight ratings with no downgrades, reflecting stable analyst sentiment.

Which company has the best grades?

Both companies have a consensus “Buy” rating, but Arm Holdings has a broader mix of buy and outperform grades with a few recent downgrades, while Cirrus Logic shows consistently stable buy and equal weight ratings. Investors may interpret Arm’s mixed signals as increased caution compared to Cirrus Logic’s steadier outlook.

Strengths and Weaknesses

Below is a comparison of key strengths and weaknesses for Arm Holdings plc (ARM) and Cirrus Logic, Inc. (CRUS) based on the latest available data.

| Criterion | Arm Holdings plc (ARM) | Cirrus Logic, Inc. (CRUS) |

|---|---|---|

| Diversification | Moderate: Revenues mainly from licensing and royalties (~$4.0B total in 2025) | Moderate: Focused on high-performance mixed signal and portable audio products (~$1.9B total in 2025) |

| Profitability | Mixed: Net margin 19.77% (favorable), ROIC 10.28% (unfavorable vs. WACC 24.3%) | Strong: Net margin 17.48%, ROIC 14.2% (both favorable, WACC 8.76%) |

| Innovation | High: Leading semiconductor IP innovator but challenges in value creation | High: Consistent innovation in mixed signal and audio tech with durable profitability |

| Global presence | Significant: Licensing model supports broad global reach | Moderate: Niche market with global customers, more specialized |

| Market Share | Strong in semiconductor IP market but facing profitability issues | Solid in audio and mixed signal markets with growing ROIC and stable margins |

Key takeaways: Cirrus Logic demonstrates stronger value creation with favorable ROIC exceeding its cost of capital and better profitability ratios. Arm Holdings, while innovative and globally diversified, struggles with value destruction due to high capital costs and weaker operational efficiency. Investors should weigh CRUS’s durable competitive advantage against ARM’s growth potential tempered by risk.

Risk Analysis

Below is a comparative table of key risks for Arm Holdings plc (ARM) and Cirrus Logic, Inc. (CRUS) based on their most recent 2025 data:

| Metric | Arm Holdings plc (ARM) | Cirrus Logic, Inc. (CRUS) |

|---|---|---|

| Market Risk | High beta (4.36) indicating high volatility | Moderate beta (1.08), more stable |

| Debt level | Very low debt-to-equity (0.05), strong balance sheet | Low debt-to-equity (0.07), financially stable |

| Regulatory Risk | Moderate, operates internationally including China | Moderate, US-based with global sales |

| Operational Risk | Moderate, complex licensing business model | Moderate, relies on innovation in mixed-signal ICs |

| Environmental Risk | Low, typical for semiconductor IP companies | Low, fabless model reduces direct manufacturing impact |

| Geopolitical Risk | Elevated due to operations in multiple geopolitical hotspots | Moderate, mainly US-based but with international exposure |

The most significant risks are ARM’s high market volatility (beta 4.36) and exposure to geopolitical tensions, which could impact supply chains and licensing agreements. CRUS shows more balanced financials and lower volatility but faces operational risks tied to technological innovation cycles. Both companies maintain strong balance sheets with minimal debt, reducing financial risk.

Which Stock to Choose?

Arm Holdings plc (ARM) shows a favorable income evolution with a 23.94% revenue growth in 2025 and strong profitability metrics like a 19.77% net margin. However, its financial ratios are slightly unfavorable overall, with high valuation multiples (PE 141.58) and a debt ratio of 0.05. The company’s ROIC is below its WACC, indicating value destruction, despite a very favorable credit rating (B).

Cirrus Logic, Inc. (CRUS) exhibits moderate income growth at 5.99% revenue increase in 2025 and solid profitability with a 17.48% net margin. Its financial ratios are globally favorable, showing balanced valuation multiples (PE 15.95) and manageable debt levels (DE 0.07). The company creates value with ROIC exceeding WACC and holds a very favorable rating (A-).

For investors, CRUS might appear more favorable due to its value-creating moat, balanced valuation, and solid financial health, which could suit risk-averse or quality-focused profiles. ARM’s rapid income growth and strong margins could appeal to growth-oriented investors comfortable with higher valuation risks.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Arm Holdings plc American Depositary Shares and Cirrus Logic, Inc. to enhance your investment decisions: