Home > Comparison > Healthcare > WST vs ATR

The strategic rivalry between West Pharmaceutical Services, Inc. and AptarGroup, Inc. shapes the competitive landscape in the healthcare instruments and supplies sector. West operates as a specialized designer and manufacturer of injectable drug delivery systems, while AptarGroup spans diversified dispensing and sealing solutions across pharma, beauty, and food markets. This analysis evaluates their distinct operational models to identify which company offers a superior risk-adjusted profile for diversified portfolios.

Table of contents

Companies Overview

West Pharmaceutical Services and AptarGroup stand as key innovators in the medical instruments and supplies market.

West Pharmaceutical Services, Inc.: Leader in Injectable Drug Delivery Systems

West Pharmaceutical Services dominates the injectable drug containment and delivery systems market. Its revenue springs mainly from proprietary and contract-manufactured products, including stoppers, seals, and self-injection devices. In 2026, West focuses strategically on advanced drug delivery technologies and integrated packaging solutions to serve biologic and pharmaceutical clients globally.

AptarGroup, Inc.: Diversified Dispensing and Material Science Innovator

AptarGroup excels in dispensing, sealing, and material science solutions across pharma, beauty, and food markets. Its core revenue comes from pumps, valves, and elastomer components, especially for pharmaceutical and consumer products. Aptar’s 2026 strategy emphasizes sustainability partnerships and digital health platforms, reflecting its commitment to innovation and market expansion.

Strategic Collision: Similarities & Divergences

Both companies lead in healthcare packaging but differ fundamentally: West focuses on closed-system injectable delivery, while Aptar pursues a broader, cross-industry portfolio with sustainability and digital integration. The primary battleground is injectable pharma components. West offers specialization and advanced integration; Aptar presents diversification and innovation breadth. Their investment profiles diverge between niche excellence and multi-market resilience.

Income Statement Comparison

The following data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | West Pharmaceutical Services, Inc. (WST) | AptarGroup, Inc. (ATR) |

|---|---|---|

| Revenue | 2.89B | 3.58B |

| Cost of Revenue | 1.89B | 2.23B |

| Operating Expenses | 408M | 859M |

| Gross Profit | 1.00B | 1.36B |

| EBITDA | 744M | 777M |

| EBIT | 588M | 514M |

| Interest Expense | 2.9M | 44M |

| Net Income | 493M | 375M |

| EPS | 6.75 | 5.65 |

| Fiscal Year | 2024 | 2024 |

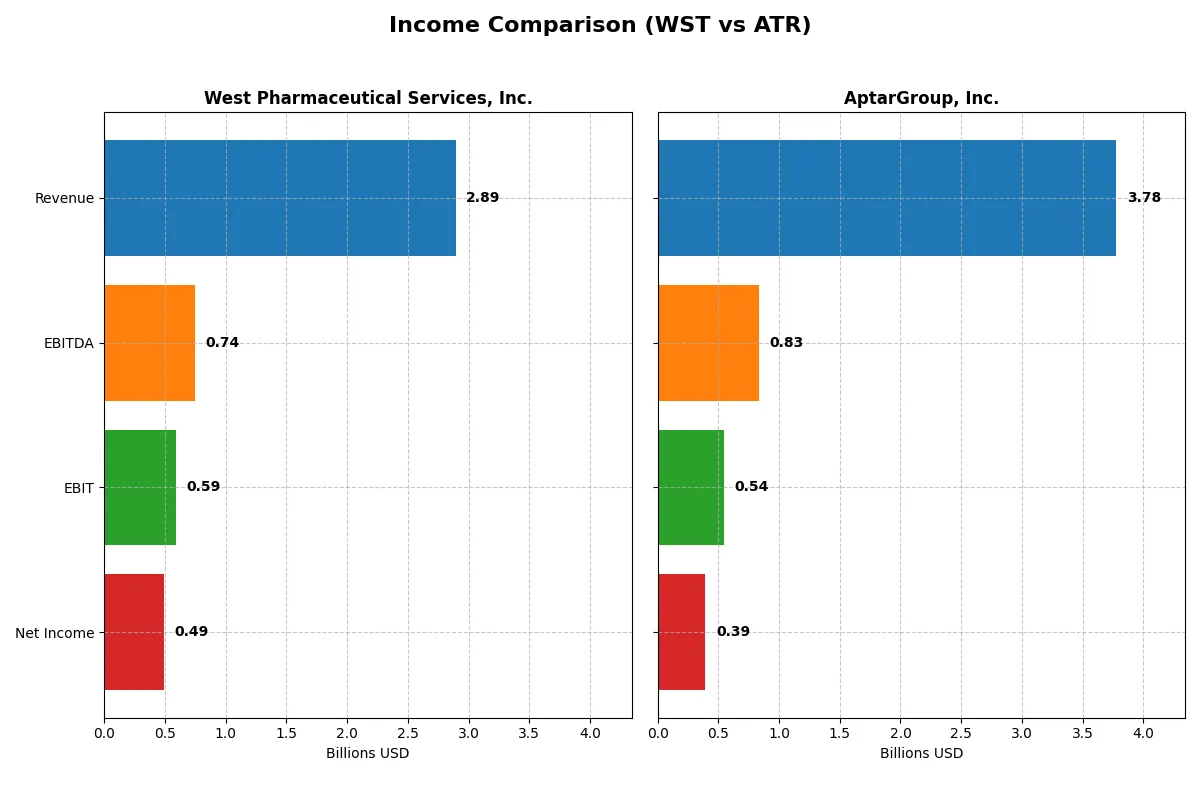

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals the true efficiency and profitability trajectory of two leading pharmaceutical packaging companies.

West Pharmaceutical Services, Inc. Analysis

West Pharmaceutical Services shows a steady revenue base near 2.9B in 2024, slightly down from 2023. Net income dropped to 493M, reflecting a 15% decline from the prior year. Despite this, West maintains strong margins: a favorable 34.65% gross margin and a solid 17.03% net margin, indicating efficient cost control and resilient profitability. The recent margin contraction signals short-term pressures, yet the overall five-year growth in revenue and net income remains robust.

AptarGroup, Inc. Analysis

AptarGroup posted 3.78B revenue in 2025, up 5.4% year-over-year, showing steady top-line momentum. Net income reached 393M, a strong 6.5% rise in EPS, although the net margin remains modest at 10.4%. Gross margin contracted by 17.6% last year, suggesting cost pressures despite improving operating income. Over five years, AptarGroup achieved impressive net income growth of over 60%, reflecting effective capital allocation and operational adjustments.

Margin Strength vs. Growth Momentum

West leads in margin quality with a superior gross and net margin, proving its operational efficiency in a challenging year. AptarGroup, meanwhile, delivers stronger revenue and net income growth, reflecting momentum and scale expansion. For investors prioritizing consistent profitability and margin stability, West’s profile is more attractive. Conversely, those favoring growth potential may lean toward AptarGroup’s upward earnings trajectory.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | West Pharmaceutical Services, Inc. (WST) | AptarGroup, Inc. (ATR) |

|---|---|---|

| ROE | 18.4% | 15.2% |

| ROIC | 15.7% | 10.7% |

| P/E | 48.5 | 27.8 |

| P/B | 8.91 | 4.22 |

| Current Ratio | 2.79 | 1.38 |

| Quick Ratio | 2.11 | 0.95 |

| D/E (Debt-to-Equity) | 0.11 | 0.44 |

| Debt-to-Assets | 8.4% | 24.3% |

| Interest Coverage | 205.0 | 11.3 |

| Asset Turnover | 0.79 | 0.81 |

| Fixed Asset Turnover | 1.72 | 2.37 |

| Payout Ratio | 12.0% | 30.5% |

| Dividend Yield | 0.25% | 1.09% |

| Fiscal Year | 2024 | 2024 |

Efficiency & Valuation Duel: The Vital Signs

Ratios serve as a company’s financial DNA, exposing hidden risks and operational strength beneath the surface numbers.

West Pharmaceutical Services, Inc.

West Pharmaceutical delivers strong profitability with an 18.37% ROE and a solid 17.03% net margin, demonstrating efficient capital use. However, its valuation appears stretched, with a high P/E of 48.53 and a P/B of 8.91. Shareholders receive a modest 0.25% dividend yield, reflecting a cautious payout amid reinvestment in R&D and growth.

AptarGroup, Inc.

AptarGroup shows moderate profitability with a 10.4% net margin but reports no ROE or ROIC, indicating less clarity on capital efficiency. The P/E ratio stands at a reasonable 20.41, suggesting a fair valuation. AptarGroup supports shareholders with a 1.5% dividend yield, balancing returns while allocating heavily to R&D at over 16% of revenue for innovation.

Premium Valuation vs. Growth Investment

West’s superior profitability contrasts with its stretched valuation, raising risk despite operational strength. AptarGroup offers a fair price and meaningful dividends but lacks clear capital returns data. Investors seeking growth may lean toward West’s efficiency, while those prioritizing valuation and steady yield might favor AptarGroup’s profile.

Which one offers the Superior Shareholder Reward?

I compare West Pharmaceutical Services (WST) and AptarGroup (ATR) on dividends and buybacks. WST yields a modest 0.25%, with a low payout ratio near 12%, indicating ample free cash flow coverage and capital for growth. Its consistent buybacks boost total returns sustainably. ATR offers a higher 1.5% yield but pays out over 30% of earnings, pressuring reinvestment capacity. ATR’s smaller buyback program limits share count reduction. Historically, WST balances dividends and buybacks more prudently, fueling durable value creation. I conclude WST offers a superior total shareholder return profile in 2026 through disciplined capital allocation and sustainable payouts.

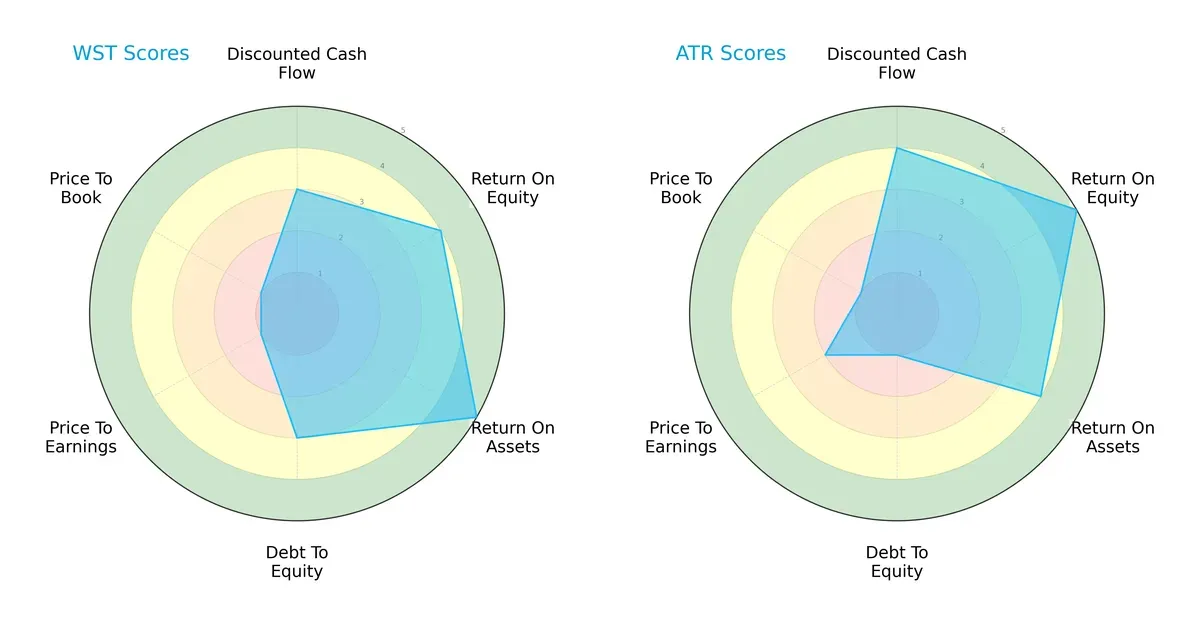

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of West Pharmaceutical Services and AptarGroup, highlighting their financial strengths and valuation challenges:

West Pharmaceutical Services shows strength in asset utilization (ROA 5) and a balanced debt profile (Debt/Equity 3). AptarGroup excels in equity efficiency (ROE 5) and discounted cash flow valuation (DCF 4), but carries higher financial risk with a weak debt score (1). West offers a more balanced profile, while AptarGroup relies on a pronounced return on equity advantage.

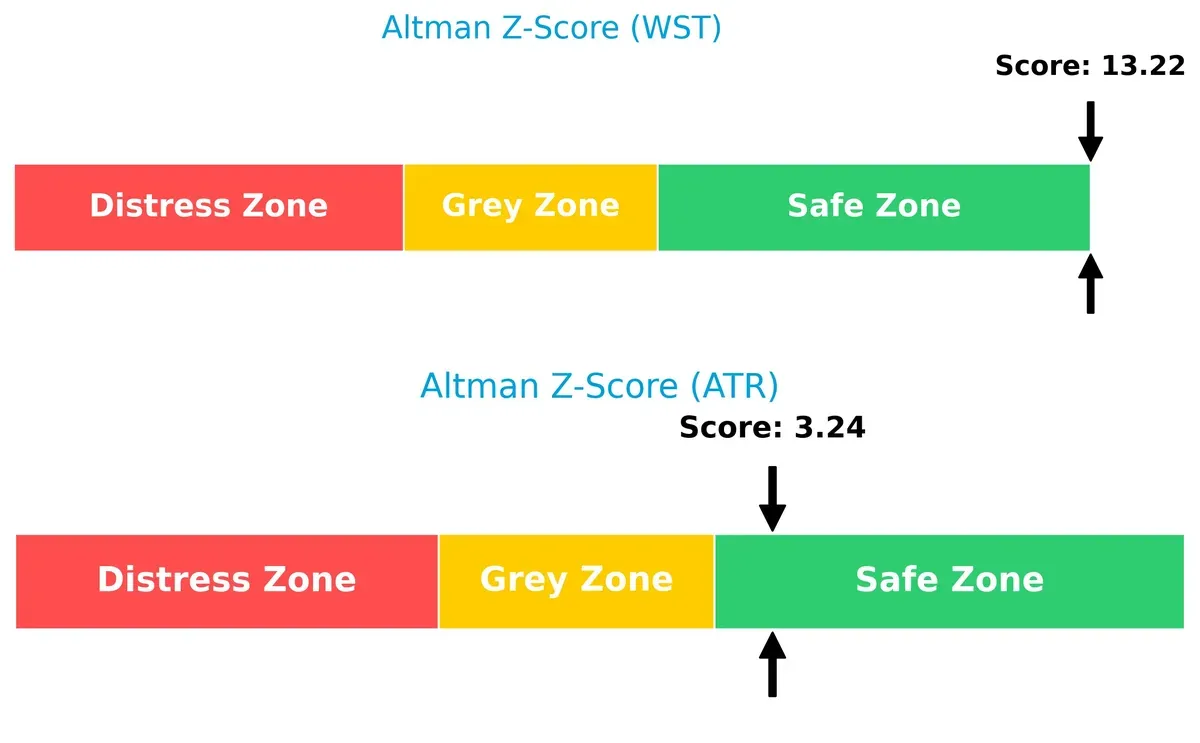

Bankruptcy Risk: Solvency Showdown

West’s Altman Z-Score of 13.2 far exceeds AptarGroup’s 3.2, signaling West’s robust solvency and lower bankruptcy risk in this cycle:

Financial Health: Quality of Operations

Both firms share an average Piotroski F-Score of 6, indicating moderate operational quality without immediate red flags:

How are the two companies positioned?

This section dissects the operational DNA of West Pharmaceutical Services and AptarGroup by comparing revenue distribution by segment and internal dynamics. The final goal is to confront their economic moats to identify which model offers the most resilient and sustainable competitive advantage today.

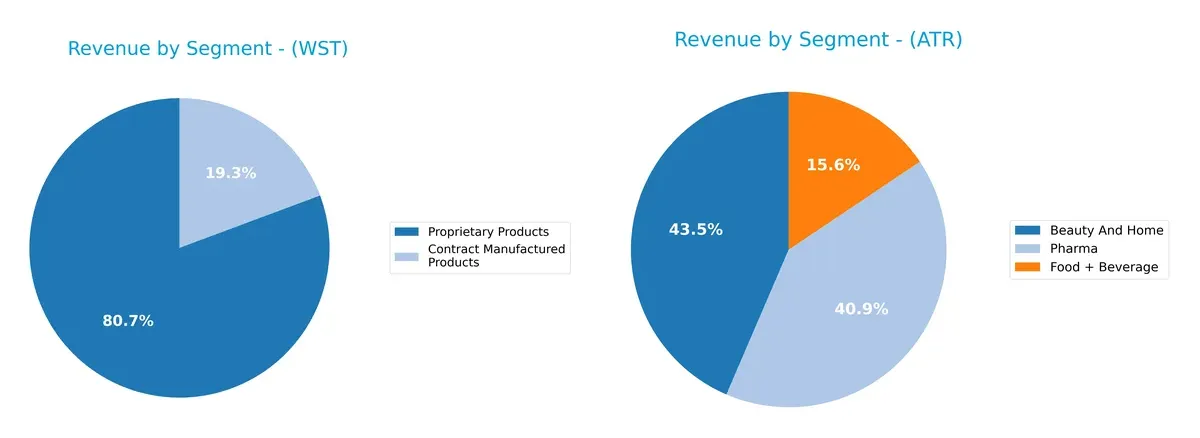

Revenue Segmentation: The Strategic Mix

This comparison dissects how West Pharmaceutical Services and AptarGroup diversify their income streams and reveals where their primary sector bets lie:

West Pharmaceutical Services anchors its revenue in Proprietary Products, generating $2.33B in 2024, dwarfing its Contract Manufactured Products at $559M. AptarGroup shows a more diversified portfolio with Beauty and Home at $1.46B, Pharma $1.37B, and Food + Beverage $524M in 2022. While West pivots on proprietary innovation, Aptar balances end-market exposure, reducing concentration risk but requiring broader operational agility.

Strengths and Weaknesses Comparison

This table compares the strengths and weaknesses of West Pharmaceutical Services (WST) and AptarGroup (ATR):

WST Strengths

- Strong profitability with 17% net margin and 18% ROE

- Low debt levels with 0.11 debt/equity ratio

- High current and quick ratios indicating liquidity

- Diverse proprietary and contract manufactured products

- Solid global presence, especially in the US and Europe

ATR Strengths

- Favorable WACC at 5.75% supports cost-effective capital

- Diverse revenue streams across Beauty, Pharma, Food & Beverage

- Strong interest coverage ratio of 10.32x

- Broad geographic footprint including US, Europe, China

- Favorable debt ratios with zero debt to assets

WST Weaknesses

- High valuation multiples with PE at 48.53 and PB at 8.91

- Dividend yield is low at 0.25%, limiting income appeal

- Neutral asset turnover ratios suggest moderate efficiency

ATR Weaknesses

- Zero ROE and ROIC highlight profitability challenges

- Unfavorable liquidity with current and quick ratios at zero

- Asset turnover ratios are zero, indicating poor asset use

- Higher percentage of unfavorable ratios at 42.86%

West Pharmaceutical exhibits robust profitability and financial stability but carries high valuation risk. AptarGroup shows geographical and product diversification but struggles with returns and liquidity. These profiles suggest contrasting strategic priorities between growth discipline and operational improvement.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only true shield protecting long-term profits from relentless competition erosion. Let’s dissect the moats of two key players in pharmaceutical packaging:

West Pharmaceutical Services, Inc.: Innovation-Driven Switching Costs

West’s moat stems from high switching costs embedded in proprietary injectable drug containment systems. This manifests in stable 20%+ EBIT margins and a 6.4% ROIC premium over WACC. In 2026, expanding advanced delivery devices should deepen this moat.

AptarGroup, Inc.: Broad Market Reach Without Economic Value Creation

Aptar’s moat relies on diversified dispensing solutions across pharma and consumer sectors but lacks value creation, shown by a negative ROIC-WACC spread and declining profitability. Despite solid revenue growth, its moat risks erosion without innovation breakthroughs.

Innovation and Value Creation vs. Market Breadth Without Defensive Economics

West holds a deeper, more sustainable moat with growing ROIC and robust margins. Aptar’s broad product reach fails to translate into value creation, leaving it vulnerable. West is better positioned to defend and grow market share in 2026 and beyond.

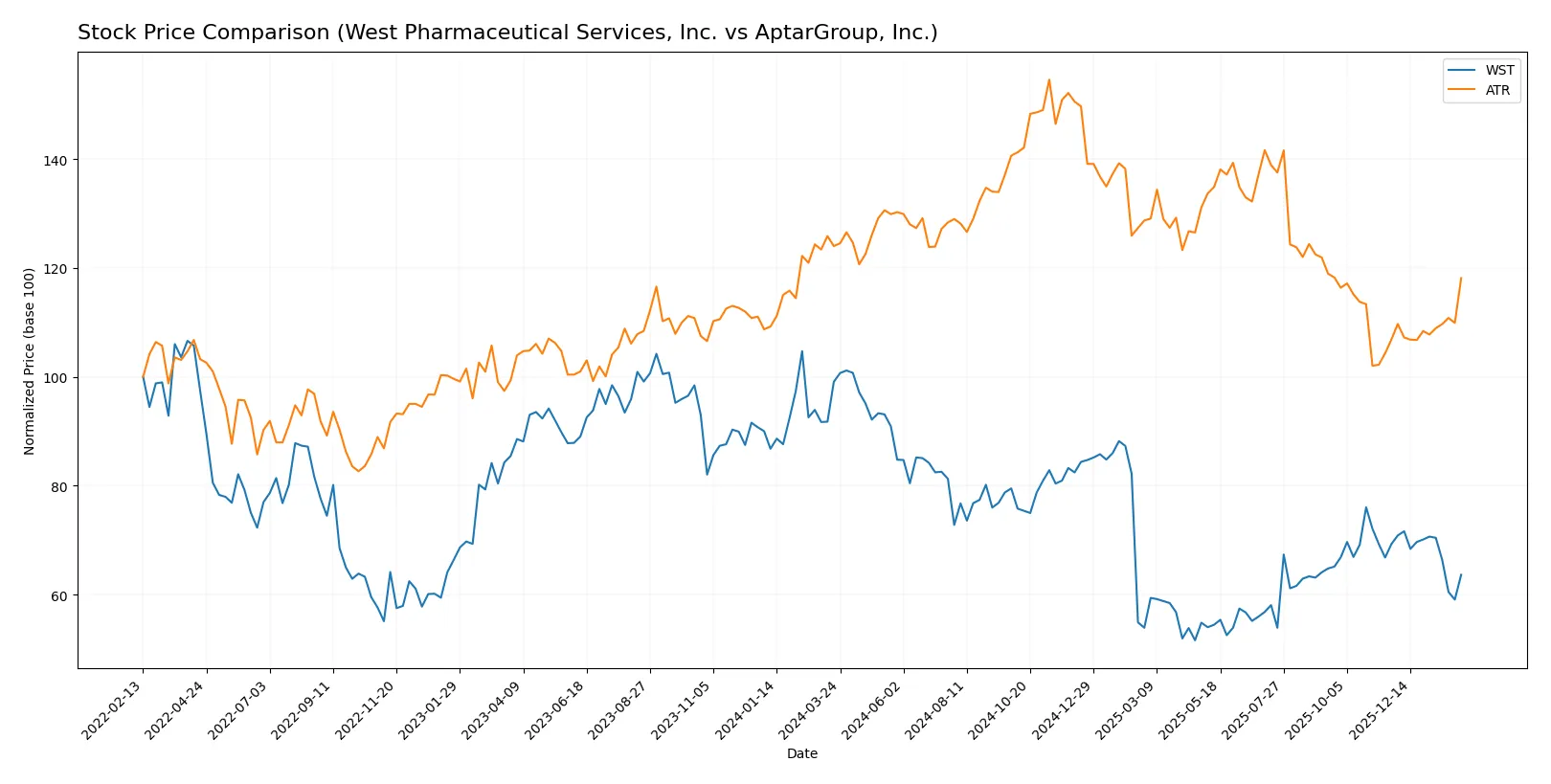

Which stock offers better returns?

The past year saw both West Pharmaceutical Services, Inc. and AptarGroup, Inc. experience declining prices, with West showing a sharper drop and higher volatility, while AptarGroup displayed recent positive momentum.

Trend Comparison

West Pharmaceutical Services, Inc. dropped 35.77% over the past 12 months, marking a bearish trend with decelerating losses and significant volatility (std dev 51.48). Its highest and lowest prices ranged from 395.71 to 201.9.

AptarGroup, Inc. declined 4.74% overall, also bearish but with accelerating momentum. Recently, it gained 10.53% amid lower volatility (std dev 13.76) and a positive trend slope, signaling a potential turnaround.

AptarGroup’s stock outperformed West Pharmaceutical, showing less severe losses and recent gains, making it the stronger performer over the analyzed period.

Target Prices

Analysts present a mixed but constructive outlook on these medical instruments leaders.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| West Pharmaceutical Services, Inc. | 285 | 355 | 323.5 |

| AptarGroup, Inc. | 133 | 220 | 166 |

West Pharmaceutical’s target consensus at 323.5 suggests a 30% upside from the current 249 price. AptarGroup shows more conservative upside potential near 24%, reflecting diverging analyst confidence.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

West Pharmaceutical Services, Inc. Grades

The table below summarizes recent grades from reliable institutions for West Pharmaceutical Services, Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Evercore ISI Group | maintain | Outperform | 2026-02-03 |

| Barclays | maintain | Equal Weight | 2025-10-27 |

| UBS | maintain | Buy | 2025-10-24 |

| Keybanc | maintain | Overweight | 2025-10-24 |

| Evercore ISI Group | maintain | Outperform | 2025-10-23 |

| Barclays | maintain | Equal Weight | 2025-10-02 |

| Barclays | maintain | Equal Weight | 2025-07-25 |

| UBS | maintain | Buy | 2025-07-25 |

| Evercore ISI Group | maintain | Outperform | 2025-07-25 |

| Keybanc | maintain | Overweight | 2025-02-14 |

AptarGroup, Inc. Grades

Below are recent grades for AptarGroup, Inc. from recognized grading companies:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Wells Fargo | downgrade | Equal Weight | 2026-01-06 |

| Baird | maintain | Outperform | 2025-11-03 |

| Wells Fargo | maintain | Overweight | 2025-11-03 |

| Wells Fargo | maintain | Overweight | 2025-09-10 |

| Wells Fargo | maintain | Overweight | 2025-08-04 |

| Raymond James | maintain | Outperform | 2025-08-04 |

| Wells Fargo | maintain | Overweight | 2025-07-18 |

| Raymond James | maintain | Outperform | 2025-07-15 |

| Wells Fargo | maintain | Overweight | 2025-05-06 |

| Raymond James | maintain | Outperform | 2025-04-22 |

Which company has the best grades?

West Pharmaceutical Services, Inc. consistently earns “Outperform” and “Buy” ratings while AptarGroup’s grades mostly range from “Overweight” to “Outperform” with one recent downgrade. This suggests West Pharmaceutical holds a slight edge in analyst confidence, potentially attracting more investor interest.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

West Pharmaceutical Services, Inc. (WST)

- Competes in specialized injectable drug delivery systems with high innovation barriers, sustaining a strong moat.

AptarGroup, Inc. (ATR)

- Faces broad competition across pharma, beauty, and food sectors, diluting focus and competitive advantage.

2. Capital Structure & Debt

West Pharmaceutical Services, Inc. (WST)

- Low debt-to-equity (0.11) and strong interest coverage (203x) indicate conservative leverage and financial stability.

AptarGroup, Inc. (ATR)

- Minimal debt reported, but lack of liquidity metrics and unclear capital structure pose transparency risks.

3. Stock Volatility

West Pharmaceutical Services, Inc. (WST)

- Beta of 1.19 suggests moderate sensitivity to market swings, typical for healthcare instruments sector.

AptarGroup, Inc. (ATR)

- Beta at 0.48 reflects lower volatility, providing defensive characteristics amid market turbulence.

4. Regulatory & Legal

West Pharmaceutical Services, Inc. (WST)

- Exposure to complex pharmaceutical regulations globally heightens compliance costs and approval risks.

AptarGroup, Inc. (ATR)

- Diverse product lines across regulated pharma and consumer sectors increase regulatory complexity and legal risk.

5. Supply Chain & Operations

West Pharmaceutical Services, Inc. (WST)

- Relies on advanced materials and manufacturing precision, vulnerable to supply disruptions and raw material price swings.

AptarGroup, Inc. (ATR)

- Broad geographic footprint and multiple segments diversify operational risks but add supply chain complexity.

6. ESG & Climate Transition

West Pharmaceutical Services, Inc. (WST)

- Limited public ESG disclosures; risks from evolving environmental standards may impact manufacturing and materials sourcing.

AptarGroup, Inc. (ATR)

- Active partnerships on recycled materials signal ESG engagement but transition risks remain amid regulatory shifts.

7. Geopolitical Exposure

West Pharmaceutical Services, Inc. (WST)

- Global operations expose WST to trade tensions, tariffs, and regulatory divergences, especially in Asia and Europe.

AptarGroup, Inc. (ATR)

- Similar global exposure; diverse markets soften impact but geopolitical instability could disrupt supply chains.

Which company shows a better risk-adjusted profile?

West Pharmaceutical Services bears significant regulatory and supply chain risks but boasts strong financial health and conservative leverage. AptarGroup shows lower stock volatility and ESG initiatives but suffers from weaker capital structure transparency and broader competitive pressures. WST’s robust Altman Z-score (13.2) and low debt mark it safer against distress. AptarGroup’s moderate Z-score (3.2) and unclear liquidity metrics raise caution. Hence, WST presents a superior risk-adjusted profile amid 2026 uncertainties.

Final Verdict: Which stock to choose?

West Pharmaceutical Services, Inc. (WST) boasts an enduring economic moat through its consistent value creation and strong capital efficiency. Its superpower lies in generating high returns on invested capital well above its cost of capital. A point of vigilance remains its recent profitability deceleration, suggesting sensitivity to market cycles. WST suits portfolios targeting long-term aggressive growth.

AptarGroup, Inc. (ATR) leverages a strategic moat in its solid recurring revenue streams and innovation in specialty packaging. While it lacks WST’s capital efficiency, ATR offers a more reasonable valuation and better near-term stability. Its profile fits Growth at a Reasonable Price (GARP) investors seeking steady income with moderate risk.

If you prioritize sustainable capital efficiency and can tolerate valuation premiums, WST outshines with its robust economic moat and growth potential. However, if you seek better near-term stability and a more balanced risk-reward tradeoff, ATR offers a more conservative path with its defensible recurring revenues. Each scenario matches distinct investor ambitions and risk tolerances.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of West Pharmaceutical Services, Inc. and AptarGroup, Inc. to enhance your investment decisions: