Home > Comparison > Technology > ADI vs NVEC

The strategic rivalry between Analog Devices, Inc. and NVE Corporation shapes the semiconductor sector’s innovation frontier. Analog Devices operates as a capital-intensive semiconductor powerhouse with broad industrial and automotive applications. In contrast, NVE Corporation focuses on niche spintronic sensor technology with a lean operational model. This analysis pits scale and diversification against specialization to identify which trajectory offers superior risk-adjusted returns for a diversified portfolio in 2026.

Table of contents

Companies Overview

Analog Devices and NVE Corporation anchor critical niches within the semiconductor industry, shaping innovation in sensor and signal processing technologies.

Analog Devices, Inc.: Leader in Integrated Signal Processing

Analog Devices commands a dominant position in analog, mixed-signal, and digital signal processing markets. Its core revenue stems from integrated circuits and subsystems that convert and condition real-world analog signals across automotive, industrial, and communications sectors. In 2026, the company sharpened its strategic focus on high-performance amplifiers and power management solutions to capitalize on evolving digital infrastructure demands.

NVE Corporation: Pioneer in Spintronic Sensor Technology

NVE Corporation specializes in spintronics-based sensors, a nanotech frontier leveraging electron spin for data acquisition and transmission. Its revenue primarily derives from sensors and couplers tailored to factory automation and medical device markets. The latest strategic emphasis targets expanding industrial Internet of Things applications through custom spintronic solutions, despite its comparatively modest scale and niche market scope.

Strategic Collision: Similarities & Divergences

Both companies operate within semiconductors but pursue distinctly different technologies—Analog Devices emphasizes broad signal processing ecosystems, while NVE focuses on specialized spintronic devices. The primary battleground lies in industrial sensing applications, where Analog Devices’ scale contrasts with NVE’s niche innovation. These divergent business models create unique risk and growth profiles, reflecting Analog Devices’ market breadth versus NVE’s focused technical edge.

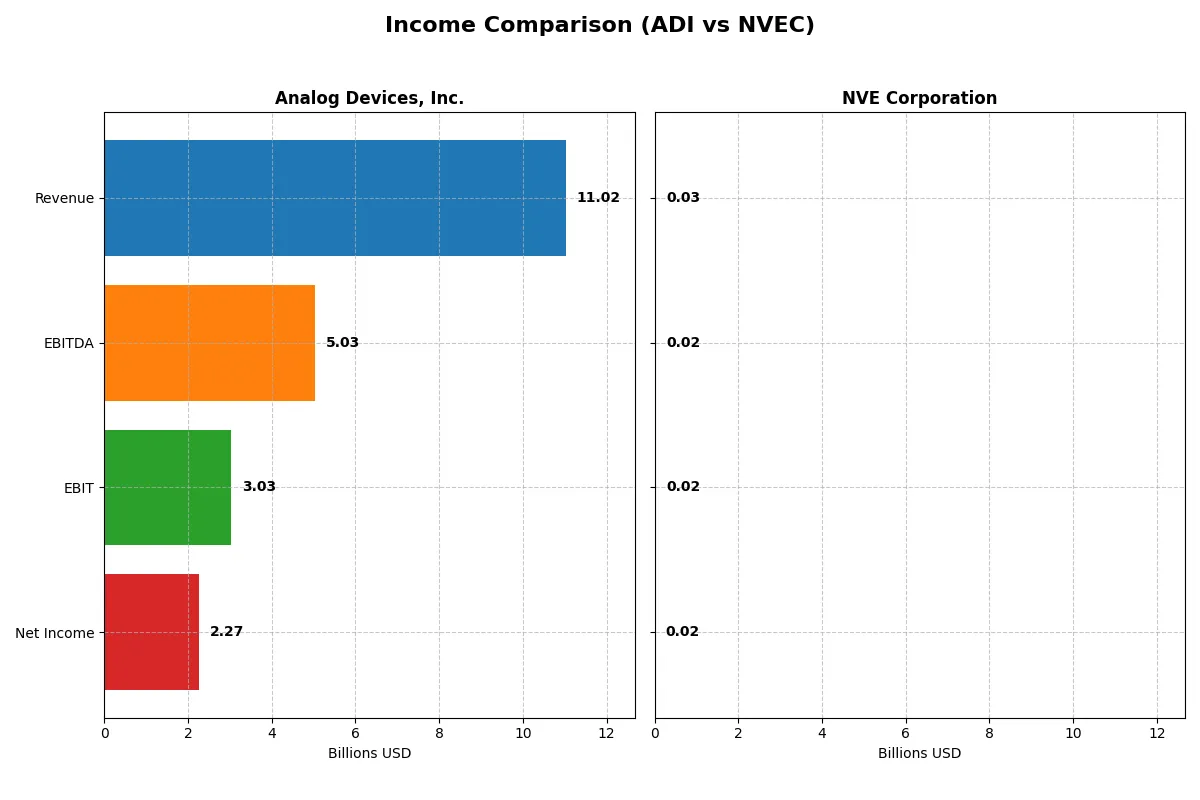

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Analog Devices, Inc. (ADI) | NVE Corporation (NVEC) |

|---|---|---|

| Revenue | 11.0B | 25.9M |

| Cost of Revenue | 5.0B | 4.2M |

| Operating Expenses | 3.0B | 5.6M |

| Gross Profit | 6.0B | 21.6M |

| EBITDA | 5.0B | 16.3M |

| EBIT | 3.0B | 16.0M |

| Interest Expense | 318M | 0 |

| Net Income | 2.3B | 15.1M |

| EPS | 4.59 | 3.12 |

| Fiscal Year | 2025 | 2025 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals which company operates with superior efficiency and profitability in their respective markets.

Analog Devices, Inc. Analysis

Analog Devices (ADI) shows a robust revenue growth from $7.3B in 2021 to $11B in 2025, with net income rising from $1.39B to $2.27B. Its gross margin remains strong at 54.66%, while net margin climbed to 20.58%, signaling improved operational efficiency. The latest year highlights a solid momentum with EBITDA surging 44%, reflecting disciplined cost management and margin expansion.

NVE Corporation Analysis

NVE Corporation (NVEC) posted revenues declining from $38M in 2023 to $26M in 2025, with net income dipping from $22.7M to $15.1M over the same period. Despite shrinking sales, NVEC boasts exceptional margins: a gross margin of 83.63% and net margin at 58.22%, demonstrating high profitability. However, the recent revenue contraction and EBIT decline indicate challenges in sustaining top-line growth momentum.

Margin Strength vs. Growth Trajectory

ADI outpaces NVEC in revenue and net income growth, showcasing impressive scale-up and margin improvement. NVEC leads in absolute margin percentages but faces revenue shrinkage and profit pressure. For investors prioritizing consistent growth and expanding profitability, ADI’s profile offers a more attractive blend of scale and improving efficiency.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | Analog Devices, Inc. (ADI) | NVE Corporation (NVEC) |

|---|---|---|

| ROE | 6.7% | 24.2% |

| ROIC | 5.5% | 21.1% |

| P/E | 51.1 | 20.5 |

| P/B | 3.42 | 4.95 |

| Current Ratio | 2.19 | 28.40 |

| Quick Ratio | 1.68 | 22.03 |

| D/E | 0.26 | 0.01 |

| Debt-to-Assets | 18.1% | 1.4% |

| Interest Coverage | 9.45 | 0 |

| Asset Turnover | 0.23 | 0.40 |

| Fixed Asset Turnover | 3.32 | 8.91 |

| Payout Ratio | 84.9% | 128.4% |

| Dividend Yield | 1.66% | 6.28% |

| Fiscal Year | 2025 | 2025 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios act as a company’s DNA, unveiling hidden risks and operational strengths that raw numbers alone cannot expose.

Analog Devices, Inc.

ADI’s net margin of 20.58% signals solid profitability, though its ROE at 6.7% trails industry norms, indicating weaker shareholder returns. The stock trades at a stretched P/E of 51.05 and a P/B of 3.42, reflecting an expensive valuation. It delivers a moderate 1.66% dividend yield, balancing returns with substantial R&D reinvestment at 16% of revenue.

NVE Corporation

NVEC boasts a robust 58.22% net margin and a high ROE of 24.19%, demonstrating operational efficiency and strong shareholder profitability. Its P/E ratio at 20.46 remains reasonable, though the P/B at 4.95 appears elevated. NVEC offers a generous 6.28% dividend yield, underpinned by efficient capital use and minimal debt, with a remarkable current ratio of 28.4.

Premium Valuation vs. Operational Safety

NVEC outperforms ADI in profitability and shareholder returns while maintaining a more balanced valuation profile despite its high P/B. ADI’s premium valuation and modest returns suggest higher risk. NVEC suits investors seeking operational efficiency and income, whereas ADI fits those betting on growth through reinvestment.

Which one offers the Superior Shareholder Reward?

I see Analog Devices (ADI) delivers a modest 1.66% dividend yield with a high payout ratio near 85%, signaling aggressive cash return but limited room for growth reinvestment. Its buyback program is steady but less intense. NVE Corporation (NVEC) offers a striking 6.28% yield with a payout ratio exceeding 100%, supported by exceptionally strong margins and free cash flow. NVEC’s buybacks complement dividends aggressively, but the over-100% payout flags sustainability risks. Historically, I’ve observed that NVEC’s yield and cash return intensity outpace ADI, but ADI’s balanced payout and reinvestment may sustain value longer. For 2026, NVEC offers a superior total return potential, though with higher distribution risk.

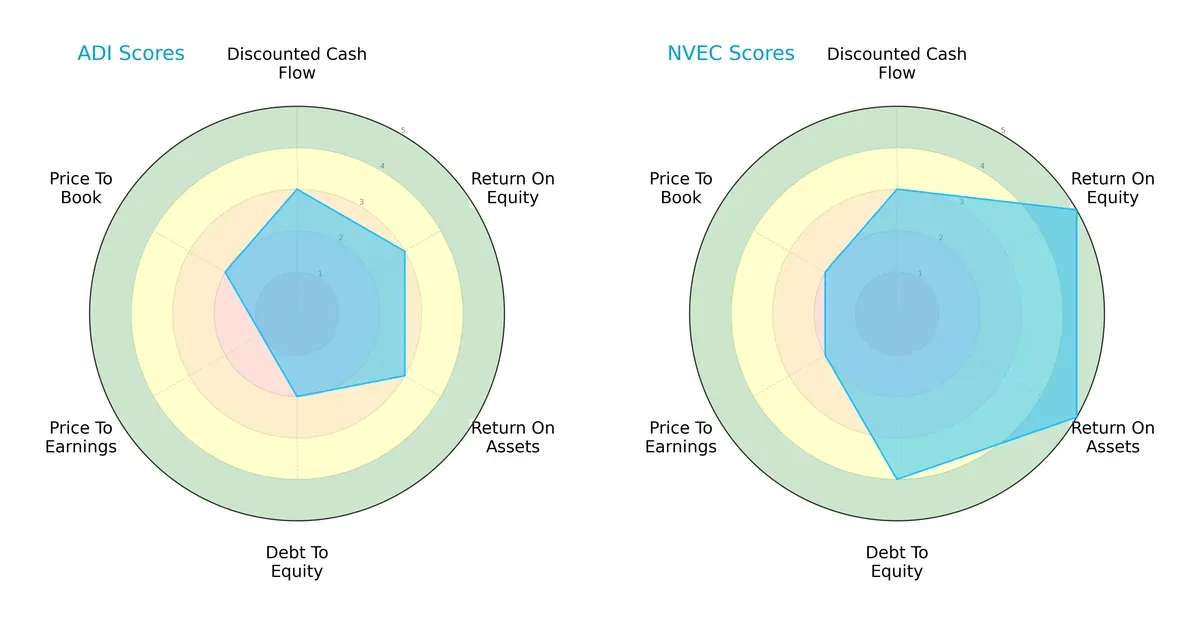

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Analog Devices, Inc. and NVE Corporation, highlighting their financial strengths and valuation profiles:

NVE Corporation demonstrates superior profitability with top-tier ROE and ROA scores of 5 each, compared to Analog Devices’ moderate scores of 3. NVE also maintains a stronger balance sheet, reflected in a 4 debt-to-equity score versus ADI’s 2. However, both share similar discounted cash flow scores of 3, signaling comparable future cash flow expectations. Analog Devices shows a valuation weakness, scoring only 1 on price-to-earnings, indicating it may be overvalued relative to earnings. Overall, NVE presents a more balanced and robust financial profile, while Analog Devices leans on moderate operational efficiency but suffers from valuation concerns.

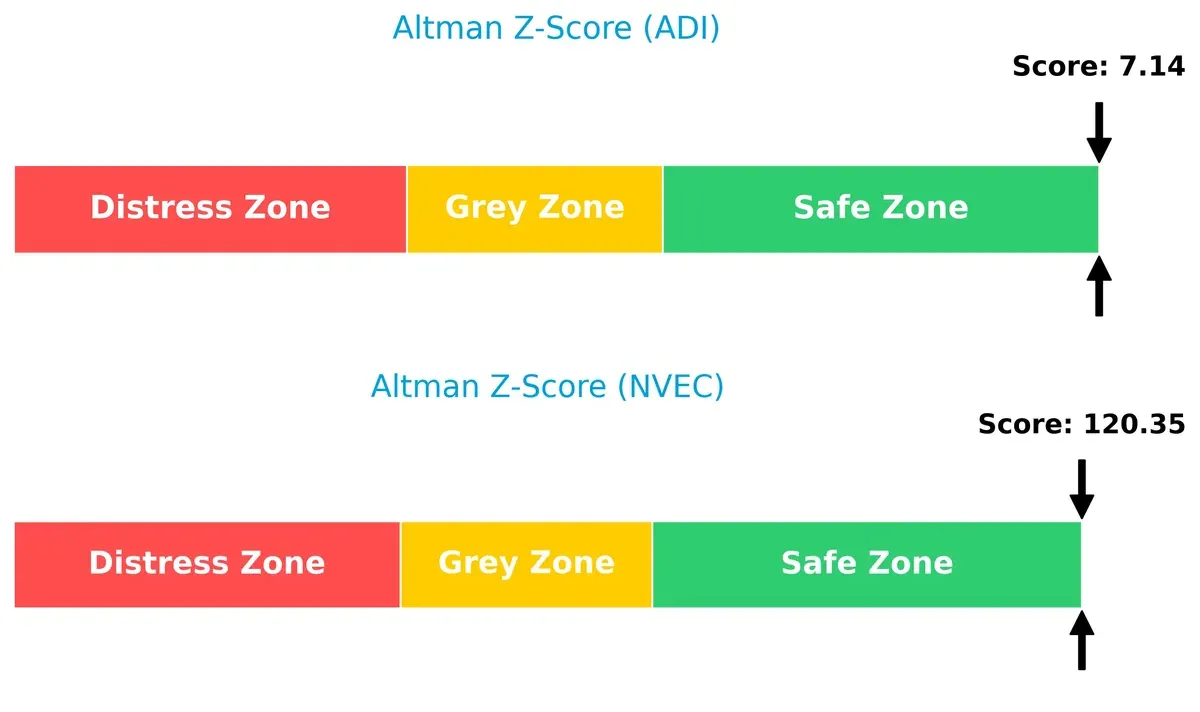

Bankruptcy Risk: Solvency Showdown

NVE Corporation’s Altman Z-Score of 120.4 vastly exceeds Analog Devices’ 7.1, placing both firmly in the safe zone but highlighting NVE’s exceptional financial resilience. This wide delta suggests NVE has a significantly lower risk of bankruptcy and stronger solvency to withstand economic downturns:

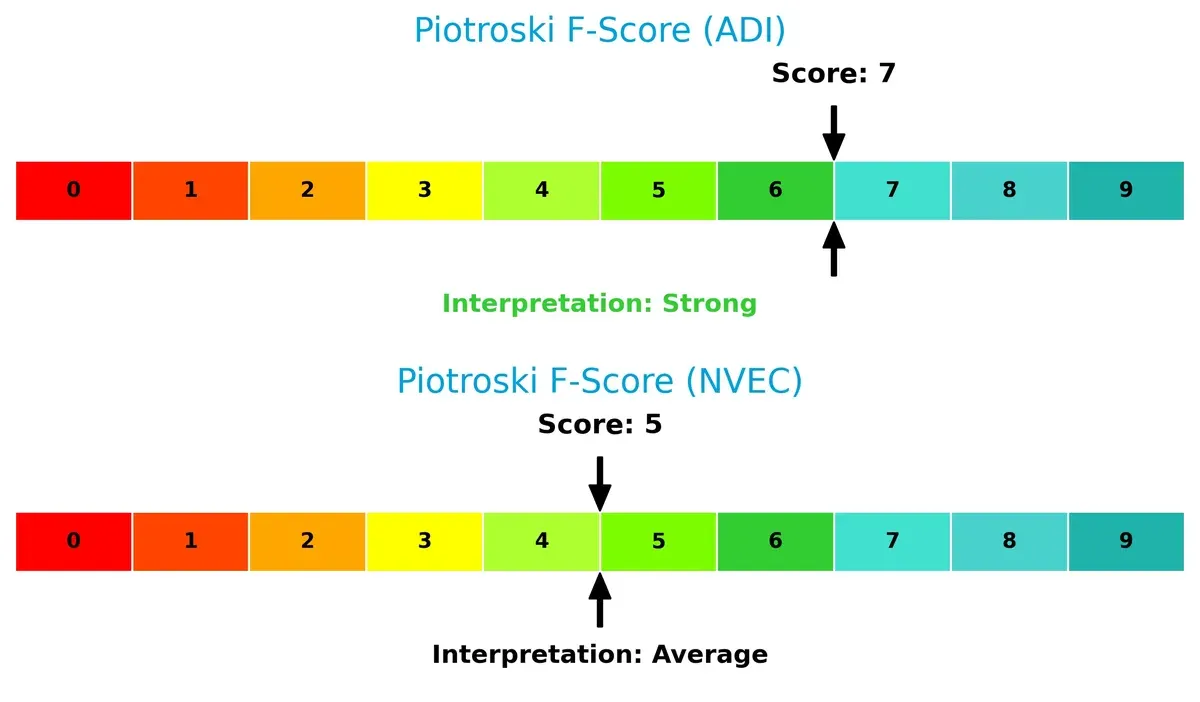

Financial Health: Quality of Operations

Analog Devices leads with a Piotroski F-Score of 7, signaling strong internal financial health and operational quality. NVE’s score of 5, while average, indicates some caution around its internal metrics. This gap suggests Analog Devices is better positioned for sustainable profitability and fewer red flags in its financial statements:

How are the two companies positioned?

This section dissects Analog Devices and NVE’s operational DNA by comparing their revenue distribution and internal dynamics. Ultimately, it confronts their economic moats to reveal which model offers the most durable competitive edge today.

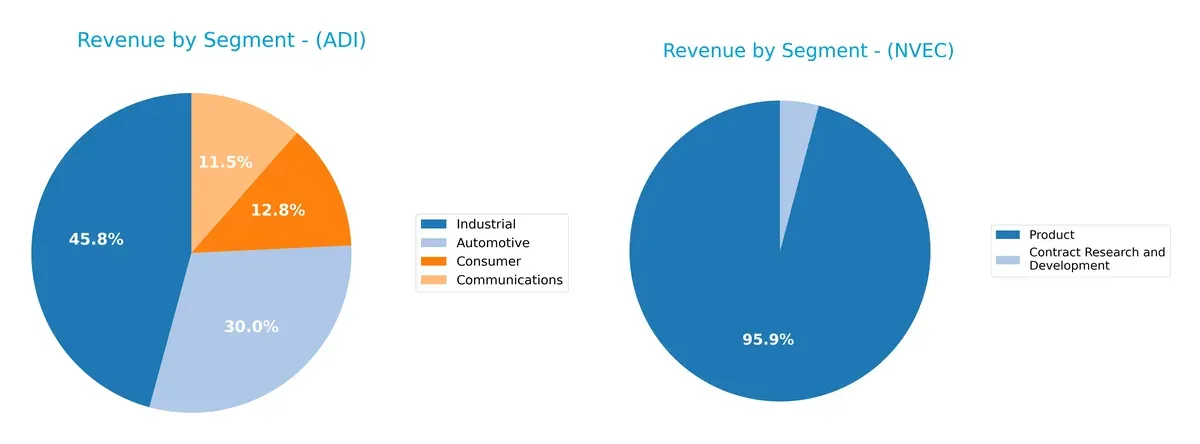

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how Analog Devices, Inc. and NVE Corporation diversify their income streams and where their primary sector bets lie:

Analog Devices anchors its revenue in Industrial ($4.3B) and Automotive ($2.8B), with Communications ($1.1B) and Consumer ($1.2B) segments adding balance. This mix reflects a strategic emphasis on infrastructure and automotive ecosystems, reducing concentration risk. Conversely, NVE relies heavily on its Product segment ($25.9M), dwarfing Contract Research ($1.1M). This focus signals high dependency on a single revenue stream, increasing vulnerability but possibly reflecting niche market leadership.

Strengths and Weaknesses Comparison

This table compares the Strengths and Weaknesses of Analog Devices, Inc. (ADI) and NVE Corporation (NVEC):

ADI Strengths

- Diversified revenue across Automotive, Industrial, Communications, Consumer sectors

- Favorable net margin at 20.58%

- Strong liquidity ratios: current ratio 2.19, quick ratio 1.68

- Low debt levels: debt to assets 18.05%

- Global sales with balanced exposure to US, China, Europe, Japan

NVEC Strengths

- High profitability: net margin 58.22%, ROE 24.19%, ROIC 21.14%

- Very low debt: debt to assets 1.43%, DE 0.01

- Excellent fixed asset turnover 8.91

- Strong innovation focus with significant R&D spend

- Favorable interest coverage with infinite value

ADI Weaknesses

- Unfavorable ROE at 6.7%, below cost of capital

- High P/E of 51.05 and P/B of 3.42 indicating expensive valuation

- Asset turnover 0.23 is low, reducing capital efficiency

- Market concentration risks as Industrial segment dominates revenue

- Neutral dividend yield limits income appeal

NVEC Weaknesses

- Unfavorable current ratio at 28.4, signaling potential liquidity mismanagement

- Elevated P/B ratio at 4.95 may indicate overvaluation

- Asset turnover 0.4 is moderate but could improve

- Limited geographic diversification, US-centric revenue

- Smaller scale revenue compared to ADI

Both companies exhibit strong profitability and solid balance sheets but differ in scale and diversification. ADI’s broad sector and geographic reach contrast with NVEC’s superior margins and capital efficiency. Each firm faces valuation and operational challenges that shape their strategic focus.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat alone shields long-term profits from relentless competition and market forces. Let’s dissect the distinct moats of Analog Devices and NVE Corporation:

Analog Devices, Inc. (ADI): Innovation and Scale-Driven Intangible Assets

ADI’s competitive edge stems from deep intangible assets and broad integration in analog and mixed-signal semiconductors. Its financials show margin stability and strong revenue growth, despite a slightly unfavorable ROIC versus WACC. In 2026, expanding into automotive and industrial IoT markets could deepen its moat, though rising capital costs remain a risk.

NVE Corporation (NVEC): Niche Spintronics Technology with High ROIC

NVEC’s moat centers on proprietary spintronic technology, creating a narrow but highly profitable niche. Unlike ADI, NVEC delivers a very favorable ROIC exceeding WACC by 11.7%, reflecting efficient capital deployment. The company’s focus on industrial IoT sensors offers growth potential, yet recent revenue declines suggest sensitivity to market cycles.

Intangible Assets vs. Technology Leadership: Who Holds the Stronger Moat?

NVEC commands a deeper moat with its superior ROIC and focused technology, signaling durable competitive advantage. ADI’s intangible asset base is broader but less capital efficient. NVEC is better positioned to defend market share amid rising competition and economic pressure.

Which stock offers better returns?

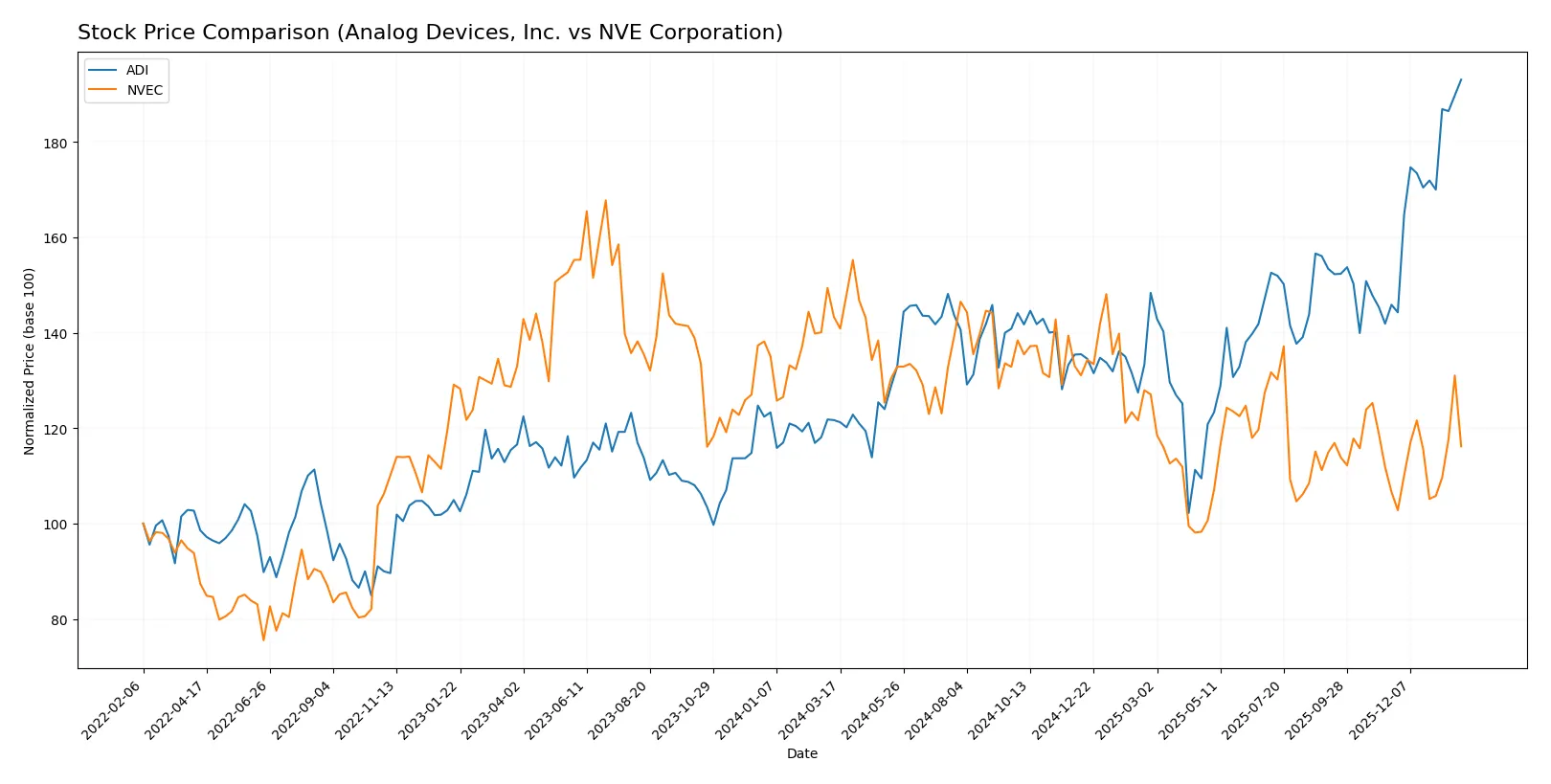

The past year reveals stark contrasts: Analog Devices, Inc. surged over 58%, showing accelerating momentum, while NVE Corporation declined nearly 19%, despite recent modest gains.

Trend Comparison

Analog Devices, Inc. shows a bullish 58.66% gain over the past 12 months with accelerating upward momentum and notable volatility, peaking at 310.88 and bottoming at 164.6.

NVE Corporation exhibits a bearish trend, falling 18.93% over the year with accelerating decline, moderate volatility, and a high of 90.18 and a low of 56.99 during the period.

Analog Devices clearly outperformed NVE Corporation, delivering superior market returns with strong acceleration, while NVE struggled despite recent slight gains.

Target Prices

Analysts set a clear target consensus for Analog Devices, Inc. (ADI) reflecting moderate upside potential.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Analog Devices, Inc. | 270 | 375 | 316 |

The consensus target of $316 sits slightly above ADI’s current $311 price, suggesting modest appreciation potential. For NVE Corporation (NVEC), no verified target price data is available from recognized analysts.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Here is the comparison of institutional grades for Analog Devices, Inc. and NVE Corporation:

Analog Devices, Inc. Grades

The table below summarizes recent grades from reputable grading companies for Analog Devices, Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Susquehanna | Maintain | Positive | 2026-01-22 |

| B of A Securities | Maintain | Buy | 2026-01-21 |

| Stifel | Maintain | Buy | 2026-01-16 |

| Oppenheimer | Maintain | Outperform | 2026-01-16 |

| Wells Fargo | Upgrade | Overweight | 2026-01-15 |

| Citigroup | Maintain | Buy | 2026-01-15 |

| Keybanc | Maintain | Overweight | 2026-01-13 |

| Truist Securities | Maintain | Hold | 2025-12-19 |

| UBS | Maintain | Buy | 2025-12-08 |

| Truist Securities | Maintain | Hold | 2025-11-26 |

NVE Corporation Grades

No reliable institutional grades are available for NVE Corporation.

Which company has the best grades?

Analog Devices, Inc. holds multiple positive and buy ratings from credible firms, signaling strong market confidence. NVE Corporation lacks available grades, leaving investor sentiment less clear.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

Analog Devices, Inc.

- Faces intense competition from larger semiconductor players with broad product portfolios.

NVE Corporation

- Competes in a niche spintronics market but with limited scale and slower growth potential.

2. Capital Structure & Debt

Analog Devices, Inc.

- Maintains a conservative debt-to-equity ratio (0.26) and strong interest coverage (9.54).

NVE Corporation

- Virtually no debt (D/E 0.01) and infinite interest coverage, indicating very low financial risk.

3. Stock Volatility

Analog Devices, Inc.

- Beta near 1.03 suggests market-level volatility aligned with NASDAQ tech stocks.

NVE Corporation

- Higher beta (1.20) indicates above-market volatility and greater sensitivity to market swings.

4. Regulatory & Legal

Analog Devices, Inc.

- Subject to complex global regulations due to large scale and multinational operations.

NVE Corporation

- Smaller scale reduces regulatory complexity but exposes it to risks from less diversified compliance.

5. Supply Chain & Operations

Analog Devices, Inc.

- Large, diversified supply chain but exposed to semiconductor cycle fluctuations and global disruptions.

NVE Corporation

- Niche supplier with limited operational scale, making supply chain disruptions potentially more impactful.

6. ESG & Climate Transition

Analog Devices, Inc.

- Faces pressure to improve ESG metrics due to size and investor scrutiny in technology sector.

NVE Corporation

- Smaller firm may face fewer ESG pressures but also less capacity to invest in transition initiatives.

7. Geopolitical Exposure

Analog Devices, Inc.

- Global footprint increases exposure to trade tensions, especially US-China relations.

NVE Corporation

- Primarily US-based, limiting geopolitical risk but with some international sales exposure.

Which company shows a better risk-adjusted profile?

NVE Corporation’s strongest risk lies in its high stock volatility and small operational scale, which heighten market sensitivity and supply chain risks. Analog Devices faces systemic risks from global competition and geopolitical tensions but maintains a stronger capital structure and diversified operations. Given these factors, NVE’s superior profitability and financial leverage are offset by its volatility and operational concentration. Analog Devices presents a more balanced and slightly favorable risk-adjusted profile, supported by robust liquidity and a prudent debt level. The recent decline in NVE’s share price by over 6% versus ADI’s more moderate drop signals heightened market concern over NVE’s risk exposure.

Final Verdict: Which stock to choose?

Analog Devices (ADI) stands out for its robust operational efficiency and consistent income growth. Its ability to expand profitability despite a slightly unfavorable moat signals management’s skill in navigating industry challenges. Investors should monitor its below-cost-of-capital returns as a cautionary flag. ADI suits portfolios targeting steady growth with an appetite for moderate risk.

NVE Corporation (NVEC) boasts a commanding moat with superior return on invested capital well above its cost of capital. Its high margins and strong capital allocation emphasize durable competitive advantages. Compared to ADI, NVEC offers greater financial safety but faces recent revenue headwinds. It fits portfolios focused on quality growth and resilience at a reasonable valuation.

If you prioritize stable cash flow expansion and operational resilience, Analog Devices is the compelling choice due to its proven income growth trajectory. However, if you seek durable competitive advantages and better capital efficiency, NVE Corporation offers superior long-term value creation and financial strength. Both present distinct strategic profiles worth considering in diversified growth strategies.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Analog Devices, Inc. and NVE Corporation to enhance your investment decisions: