Home > Comparison > Technology > ADI vs NVMI

The strategic rivalry between Analog Devices, Inc. and Nova Ltd. shapes the semiconductor industry’s evolution. Analog Devices operates as a capital-intensive technology leader with diversified analog and mixed-signal solutions. Nova Ltd. focuses on specialized process control systems for semiconductor manufacturing, leveraging niche metrology expertise. This head-to-head pits broad market dominance against targeted innovation. This analysis will identify which trajectory offers superior risk-adjusted returns for a diversified portfolio navigating technology sector dynamics.

Table of contents

Companies Overview

Analog Devices, Inc. and Nova Ltd. stand as key players shaping the semiconductor industry’s future.

Analog Devices, Inc.: Semiconductor Innovator with Diverse Signal Processing

Analog Devices dominates the semiconductor space by designing and manufacturing integrated circuits that convert analog signals to digital and vice versa. Its core revenue stems from products like data converters, power management ICs, and high-performance amplifiers. In 2026, the company focuses strategically on expanding its presence across automotive, industrial, and communications sectors worldwide.

Nova Ltd.: Precision Metrology Leader in Semiconductor Manufacturing

Nova Ltd. specializes in process control systems critical for semiconductor fabrication. It generates revenue by selling metrology platforms that measure dimensions, films, and chemicals for wafer processing steps. In 2026, Nova centers its strategy on enhancing accuracy and reliability for advanced chipmakers globally, supporting logic, memory, and foundry manufacturing.

Strategic Collision: Precision Versus Integration in a Competitive Market

While Analog Devices pursues a broad signal processing ecosystem, Nova concentrates on niche metrology precision. Both battle for supremacy in semiconductor production but from different angles—Analog Devices targets diversified applications, Nova zeroes in on manufacturing accuracy. Their investment profiles diverge: Analog Devices offers scale and stability; Nova promises specialized growth amid high technical barriers.

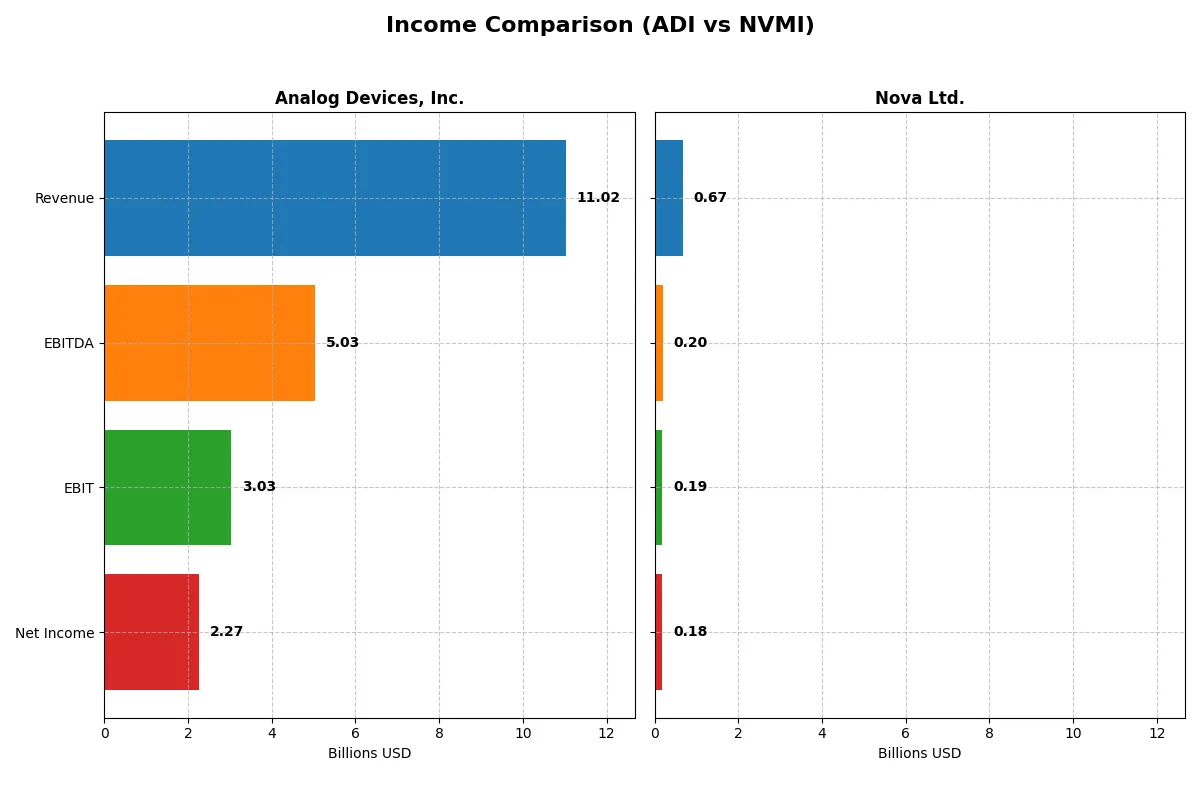

Income Statement Comparison

The following data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Analog Devices, Inc. (ADI) | Nova Ltd. (NVMI) |

|---|---|---|

| Revenue | 11.0B | 672M |

| Cost of Revenue | 5.0B | 285M |

| Operating Expenses | 3.0B | 200M |

| Gross Profit | 6.0B | 387M |

| EBITDA | 5.0B | 205M |

| EBIT | 3.0B | 188M |

| Interest Expense | 318M | 1.6M |

| Net Income | 2.3B | 185M |

| EPS | 4.59 | 6.31 |

| Fiscal Year | 2025 | 2024 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals the true operational efficiency and growth momentum of Analog Devices, Inc. and Nova Ltd. in recent years.

Analog Devices, Inc. Analysis

ADI’s revenue rose sharply from $7.3B in 2021 to $11B in 2025, while net income nearly doubled from $1.4B to $2.3B. Its gross margin sustains a healthy 54.7%, with a net margin of 20.6%, reflecting disciplined cost control. The 2025 fiscal year shows robust momentum, with EBIT surging 44% year-over-year and EPS growth of 39%, signaling strong profitability improvement.

Nova Ltd. Analysis

NVMI’s revenue climbed impressively from $269M in 2020 to $672M in 2024, with net income soaring from $48M to $185M. Gross margin stands slightly higher at 57.6%, and net margin at 27.3%, indicating efficient operations at a smaller scale. In 2024, revenue jumped nearly 30%, supported by a 32% gross profit increase, while EPS grew 34%, demonstrating solid expansion and improving earnings quality.

Growth Trajectory vs. Margin Strength

ADI delivers larger absolute profits with a consistent double-digit revenue increase and solid margins, reflecting mature scale and operational excellence. NVMI, while smaller, exhibits explosive growth rates above 29% annually and superior net margins, highlighting rapid scalability and efficiency. For investors, ADI’s stability suits those seeking steady income growth; NVMI appeals to those targeting high-growth potential in a leaner business model.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies analyzed:

| Ratios | Analog Devices, Inc. (ADI) | Nova Ltd. (NVMI) |

|---|---|---|

| ROE | 6.7% | 19.8% |

| ROIC | 5.5% | 13.4% |

| P/E | 51.1 | 31.2 |

| P/B | 3.42 | 6.18 |

| Current Ratio | 2.19 | 2.32 |

| Quick Ratio | 1.68 | 1.92 |

| D/E | 0.26 | 0.25 |

| Debt-to-Assets | 18.1% | 17.0% |

| Interest Coverage | 9.45 | 116.2 |

| Asset Turnover | 0.23 | 0.48 |

| Fixed Asset Turnover | 3.32 | 5.06 |

| Payout ratio | 84.9% | 0% |

| Dividend yield | 1.66% | 0% |

| Fiscal Year | 2025 | 2024 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios serve as a company’s DNA, uncovering hidden risks and operational strengths that numbers alone can’t fully reveal.

Analog Devices, Inc.

ADI posts a solid net margin of 20.58% but a low 6.7% ROE, signaling moderate profitability. Its P/E of 51.05 marks the stock as expensive relative to earnings. ADI maintains a 1.66% dividend yield, reflecting balanced shareholder returns alongside significant reinvestment in R&D at over 16% of revenue.

Nova Ltd.

NVMI delivers superior profitability with a 27.33% net margin and a robust 19.81% ROE. Despite a high P/E of 31.2, the stock appears less stretched than ADI. NVMI pays no dividend, choosing instead to prioritize growth through R&D, which consumes roughly 16% of sales, consistent with its efficiency focus.

Profitability vs. Valuation: Balanced or Premium Risk?

NVMI outshines ADI in core profitability and operational efficiency but trades at a premium with no dividend payout. ADI’s higher valuation and modest returns suggest more conservative income. Growth-seekers may prefer NVMI’s aggressive reinvestment; income-focused investors might lean toward ADI’s dividend and stable metrics.

Which one offers the Superior Shareholder Reward?

I observe Analog Devices, Inc. (ADI) offers consistent dividends with a 1.66% yield and a high payout ratio near 85%, supported by strong free cash flow coverage at 1.96x. ADI also executes steady buybacks, enhancing total shareholder returns. Nova Ltd. (NVMI) pays no dividends but aggressively reinvests all free cash flow into growth and acquisitions, reflecting zero payout ratio and strong free cash flow conversion at 93%. However, NVMI’s buyback activity is limited, focusing more on capital expenditure efficiency. I find ADI’s balanced distribution model more sustainable, combining yield and buybacks, whereas NVMI’s all-in growth approach carries higher execution risk. For 2026 investors prioritizing total return with income and capital gains, ADI offers the superior shareholder reward.

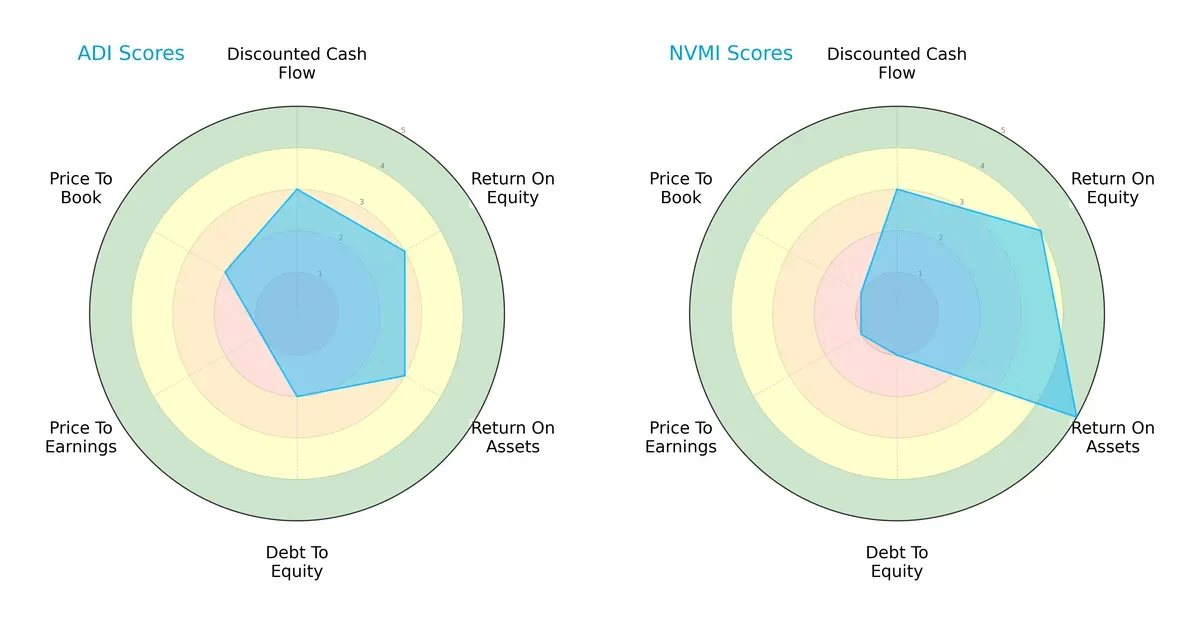

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Analog Devices, Inc. and Nova Ltd., highlighting their core financial strengths and vulnerabilities:

Nova Ltd. excels in return on equity (4 vs. 3) and return on assets (5 vs. 3), showing superior operational efficiency. Analog Devices holds a more balanced debt-to-equity score (2 vs. 1), indicating relatively lower financial risk. Both firms share moderate discounted cash flow scores (3), but Analog Devices edges Nova in price-to-book valuation (2 vs. 1). Nova relies heavily on operational efficiency, while Analog Devices presents a steadier risk profile.

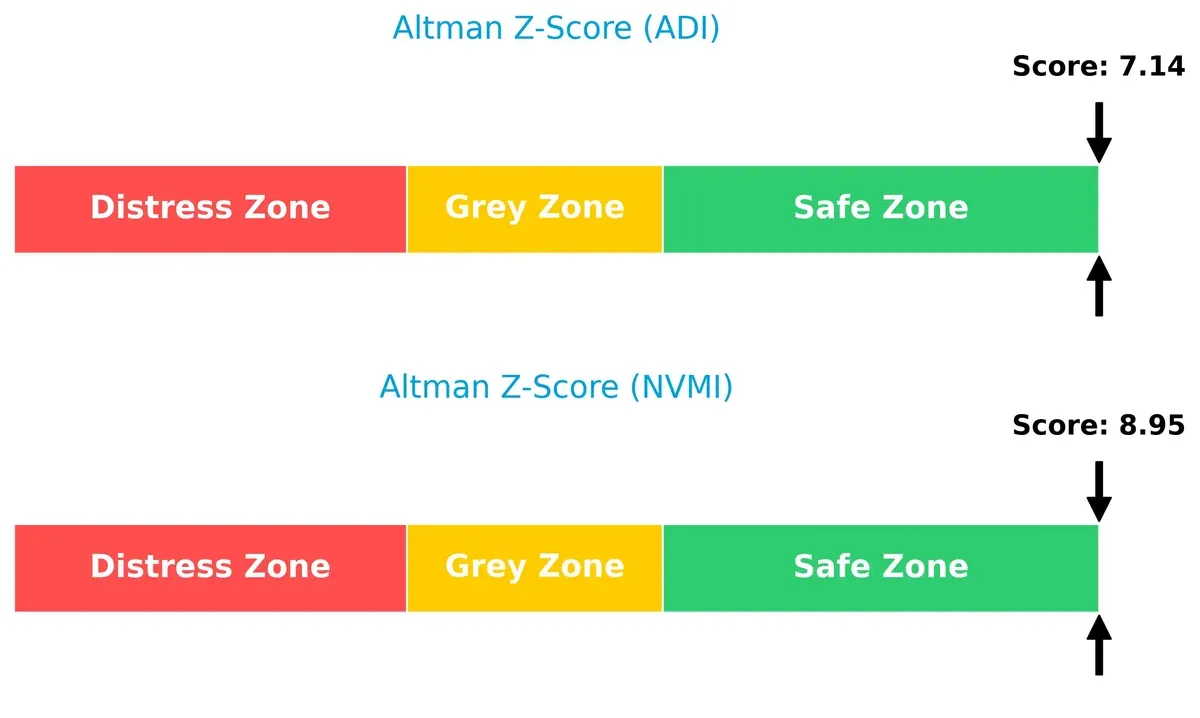

Bankruptcy Risk: Solvency Showdown

The Altman Z-Score comparison underscores both firms’ robust financial stability in this cycle:

Nova Ltd. leads with a higher Z-Score (8.95) versus Analog Devices’ 7.14. Both scores place them firmly in the safe zone, signaling low bankruptcy risk and strong long-term survival prospects.

Financial Health: Quality of Operations

Both companies demonstrate strong operational quality, reflected in identical Piotroski F-Scores:

Analog Devices and Nova Ltd. each score 7, indicating solid financial health. Neither shows red flags in internal metrics, suggesting reliable earnings quality and prudent capital allocation.

How are the two companies positioned?

This section dissects the operational DNA of ADI and NVMI by comparing their revenue distribution and internal dynamics. The goal is to confront their economic moats and reveal which model provides the most resilient competitive advantage today.

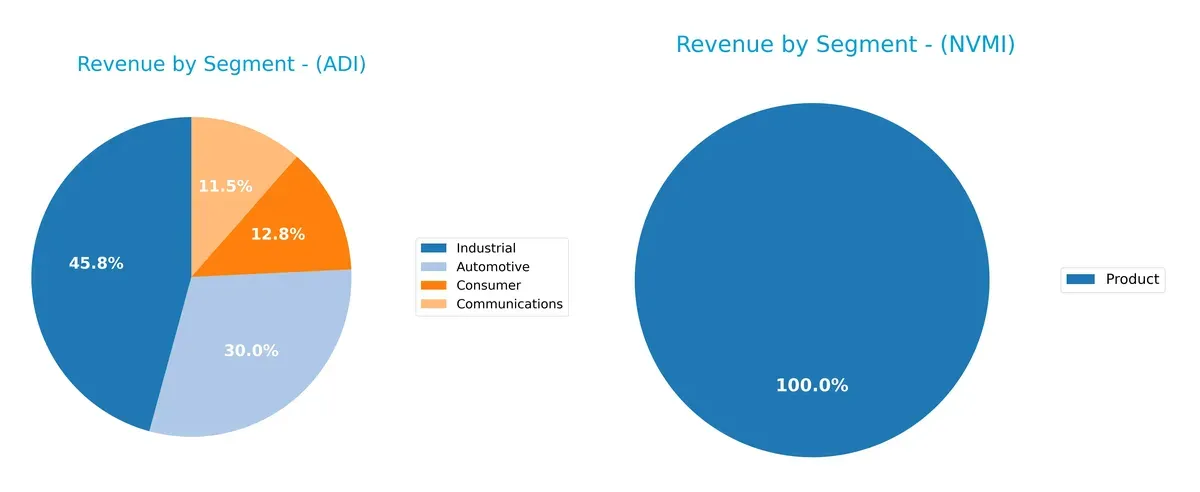

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how Analog Devices, Inc. and Nova Ltd. diversify their income streams and reveals their primary sector bets:

Analog Devices anchors revenue in Industrial with $4.3B in 2024, complemented by strong Automotive ($2.8B) and Consumer ($1.2B) segments, showing solid diversification. Nova Ltd. relies solely on a single Product segment at $538M, exposing it to concentration risk. Analog Devices’ broad mix signals ecosystem lock-in and infrastructure dominance, while Nova’s narrow focus demands cautious monitoring amid market shifts.

Strengths and Weaknesses Comparison

This table compares the Strengths and Weaknesses of Analog Devices, Inc. and Nova Ltd.:

ADI Strengths

- Diversified revenue across Automotive, Communications, Consumer, Industrial segments

- Favorable net margin at 20.58%

- Strong liquidity with current ratio 2.19 and quick ratio 1.68

- Low leverage with debt-to-assets at 18.05%

- Favorable interest coverage at 9.54

NVMI Strengths

- Higher net margin at 27.33% and ROE at 19.81%

- Strong ROIC at 13.39% above WACC

- Favorable liquidity ratios with current 2.32 and quick 1.92

- Very high interest coverage of 116.2

- Higher fixed asset turnover at 5.06

ADI Weaknesses

- Unfavorable ROE at 6.7% below cost of capital

- Unfavorable P/E of 51.05 and P/B of 3.42 indicating high valuation

- Low asset turnover at 0.23 suggests inefficient asset use

- Neutral ROIC vs. WACC relationship

- Dividend yield only 1.66%

NVMI Weaknesses

- Unfavorable WACC at 12.29% indicating higher capital cost

- Unfavorable P/E of 31.2 and high P/B at 6.18 suggest overvaluation

- Asset turnover moderate at 0.48 but still marked unfavorable

- No dividend yield, which may deter income-focused investors

Both companies show solid liquidity and low leverage supporting financial stability. ADI’s broad diversification contrasts with NVMI’s focused product base. NVMI delivers superior profitability and capital returns but faces a higher cost of capital and valuation pressure. ADI’s asset efficiency and valuation metrics require cautious monitoring.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only reliable shield protecting long-term profits from relentless competitive erosion:

Analog Devices, Inc. (ADI): Innovation-Driven Product Ecosystem

ADI’s moat stems from its intangible assets and technological know-how in analog and mixed-signal processing. This manifests in stable margins around 27% EBIT and growing profitability despite value destruction indicated by ROIC below WACC. Expansion into automotive and industrial markets could deepen its moat by 2026, but rising competition poses risks.

Nova Ltd. (NVMI): Precision Metrology Niche with Growth Potential

Nova’s moat is a specialized cost and technology advantage in semiconductor process control, contrasting ADI’s broader analog portfolio. NVMI posts higher margins (27.9% EBIT) and a positive ROIC trend signaling improving capital efficiency. Its strong revenue growth and expanding addressable market in advanced packaging support a widening moat through 2026.

Moat Depth Showdown: Specialized Precision vs. Broad Innovation

Nova exhibits a slightly wider and improving moat with superior ROIC trends and explosive revenue growth. ADI’s broader innovation portfolio faces margin pressure despite growing profitability. NVMI appears better equipped to defend and expand its niche market share by 2026.

Which stock offers better returns?

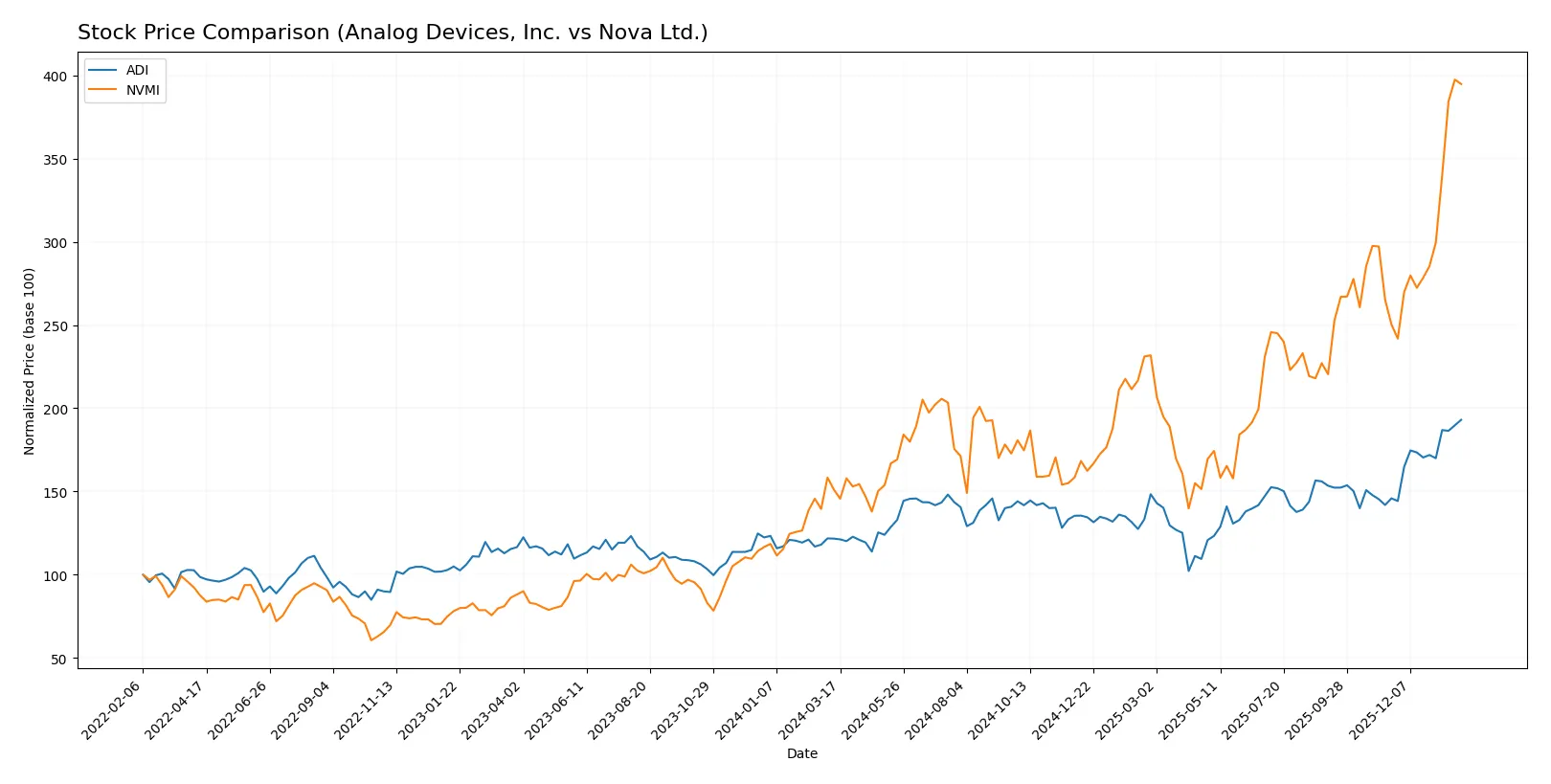

The past year shows strong price advances for both stocks, with notable acceleration and buyer dominance shaping their trading dynamics.

Trend Comparison

Analog Devices, Inc. (ADI) posted a 58.66% price increase over 12 months, confirming a bullish trend with accelerating momentum and a high of 310.88. Volatility remains moderate with a 26.38 standard deviation.

Nova Ltd. (NVMI) surged 161.13% in the same period, exhibiting strong bullish acceleration and a peak at 460.91. Volatility is elevated, reflected by a 63.77 standard deviation.

NVMI clearly outperformed ADI, delivering the highest market performance with more than double the price appreciation and stronger buyer dominance.

Target Prices

Analysts provide a solid consensus on target prices for Analog Devices, Inc. and Nova Ltd., reflecting cautious optimism.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Analog Devices, Inc. | 270 | 375 | 316 |

| Nova Ltd. | 335 | 500 | 408.33 |

The consensus target for Analog Devices sits slightly above the current price of $310.88, suggesting moderate upside potential. Nova Ltd.’s target consensus exceeds its current $457.84 price, indicating room for growth despite recent volatility.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

The following tables summarize recent institutional grades for Analog Devices, Inc. and Nova Ltd.:

Analog Devices, Inc. Grades

This table compiles the latest grades from recognized financial institutions for Analog Devices, Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Susquehanna | maintain | Positive | 2026-01-22 |

| B of A Securities | maintain | Buy | 2026-01-21 |

| Stifel | maintain | Buy | 2026-01-16 |

| Oppenheimer | maintain | Outperform | 2026-01-16 |

| Wells Fargo | upgrade | Overweight | 2026-01-15 |

| Citigroup | maintain | Buy | 2026-01-15 |

| Keybanc | maintain | Overweight | 2026-01-13 |

| Truist Securities | maintain | Hold | 2025-12-19 |

| UBS | maintain | Buy | 2025-12-08 |

| Truist Securities | maintain | Hold | 2025-11-26 |

Nova Ltd. Grades

This table presents recent grades from established financial analysts for Nova Ltd.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Needham | upgrade | Buy | 2026-01-20 |

| B of A Securities | maintain | Buy | 2026-01-13 |

| Jefferies | maintain | Buy | 2025-12-15 |

| Evercore ISI Group | maintain | Outperform | 2025-11-07 |

| Benchmark | maintain | Buy | 2025-11-07 |

| Cantor Fitzgerald | maintain | Overweight | 2025-06-24 |

| B of A Securities | maintain | Buy | 2025-06-24 |

| Citigroup | maintain | Buy | 2025-05-09 |

| Benchmark | maintain | Buy | 2025-05-09 |

| B of A Securities | maintain | Buy | 2025-04-16 |

Which company has the best grades?

Both companies receive predominantly positive ratings, with multiple Buys and Outperforms. Analog Devices shows a recent upgrade from Wells Fargo to Overweight, while Nova Ltd. has a recent Needham upgrade to Buy. The strong consensus Buy ratings suggest favorable institutional sentiment for both stocks, which may support investor confidence.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

Analog Devices, Inc.

- Faces intense rivalry in semiconductors with pressure on margins despite strong market cap and diversified customer base.

Nova Ltd.

- Operates in a niche semiconductor metrology segment but battles higher beta volatility and smaller scale against major industry players.

2. Capital Structure & Debt

Analog Devices, Inc.

- Maintains a conservative debt-to-equity ratio (0.26) with strong interest coverage (9.54), indicating prudent leverage management.

Nova Ltd.

- Also conservative on debt (0.25 D/E) but with exceptional interest coverage (116.2), signaling robust ability to service debt despite higher WACC.

3. Stock Volatility

Analog Devices, Inc.

- Beta near 1.03 suggests stock price moves roughly with the market, offering moderate volatility risk.

Nova Ltd.

- Higher beta at 1.83 indicates greater stock price swings and elevated market risk for investors.

4. Regulatory & Legal

Analog Devices, Inc.

- US-based, exposed to stringent technology export controls and IP regulations that could constrain global sales.

Nova Ltd.

- Israel-based with exposure to complex international trade laws and potential geopolitical sanctions impacting supply chains.

5. Supply Chain & Operations

Analog Devices, Inc.

- Large global footprint mitigates risk but complexity adds vulnerability to raw material cost inflation and logistics disruptions.

Nova Ltd.

- Smaller workforce and high specialization narrow operational risks but increase dependence on key suppliers and contract manufacturers.

6. ESG & Climate Transition

Analog Devices, Inc.

- Increasing pressure to improve sustainability in manufacturing and energy consumption; risk of falling behind peers on ESG standards.

Nova Ltd.

- Limited public ESG data raises transparency concerns; climate transition policies could impose unforeseen compliance costs.

7. Geopolitical Exposure

Analog Devices, Inc.

- Significant sales exposure in China and Asia subjects ADI to US-China tensions and tariffs risks.

Nova Ltd.

- Headquartered in Israel, with operations in Asia and US, faces geopolitical uncertainties including regional conflicts and trade barriers.

Which company shows a better risk-adjusted profile?

Analog Devices’ moderate volatility, strong capital structure, and diversified operations suggest a steadier risk profile. Nova Ltd. delivers higher operational returns but faces amplified volatility and geopolitical risks. Analog Devices’ prudent leverage and broader market presence mitigate systemic shocks better. Nova’s higher beta and concentrated niche expose it to sharper swings and regulatory unpredictability. The distinct risk drivers for each company highlight ADI’s more balanced risk-adjusted position despite slower growth signals.

Final Verdict: Which stock to choose?

Analog Devices, Inc. (ADI) shines with its resilience and strong cash generation, fueling steady innovation. Its main point of vigilance lies in a modest return on invested capital, which currently trails its cost of capital. ADI suits portfolios seeking reliable income with moderate growth — a stable core holding.

Nova Ltd. (NVMI) boasts a strategic moat anchored in robust profitability and expanding returns on capital. Its safety profile appears more volatile compared to ADI, reflecting smaller scale and higher valuation multiples. NVMI fits investors aiming for growth at a reasonable price with a tolerance for cyclicality.

If you prioritize steady cash flow and proven operational efficiency, ADI is the compelling choice due to its consistent income and conservative balance sheet. However, if you seek accelerated growth potential backed by improving capital returns, NVMI offers better upside despite premium valuation and higher volatility. Both demand careful risk management given their distinct profiles.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Analog Devices, Inc. and Nova Ltd. to enhance your investment decisions: