Home > Comparison > Technology > LRCX vs ADI

The strategic rivalry between Lam Research Corporation and Analog Devices, Inc. shapes the semiconductor industry’s evolution. Lam Research operates as a capital-intensive equipment manufacturer specializing in wafer fabrication tools. In contrast, Analog Devices focuses on high-margin integrated circuits and mixed-signal processing solutions. This head-to-head highlights a contest between manufacturing scale and product innovation. This analysis aims to identify which company’s trajectory offers superior risk-adjusted returns for a diversified portfolio in technology.

Table of contents

Companies Overview

Lam Research and Analog Devices stand as pivotal players in the semiconductor industry, shaping technology infrastructure worldwide.

Lam Research Corporation: Semiconductor Equipment Specialist

Lam Research dominates semiconductor fabrication equipment, generating revenue primarily from advanced wafer processing tools. Its 2026 strategy focuses on expanding high-precision etching and deposition technologies, underpinning next-gen integrated circuit manufacturing. Core products like ALTUS and SABRE systems sustain its competitive edge in wafer fabrication.

Analog Devices, Inc.: Analog and Mixed-Signal Innovator

Analog Devices leads in integrated circuits and mixed-signal processing, profiting chiefly from data converters and power management ICs. In 2026, it emphasizes enhancing analog signal conditioning and RF technologies for automotive and industrial markets. Its broad portfolio of amplifiers and MEMS sensors supports diverse high-growth sectors.

Strategic Collision: Similarities & Divergences

Both firms excel in semiconductors but diverge fundamentally: Lam Research targets manufacturing equipment, while Analog Devices focuses on component design. Their competition centers on the semiconductor value chain—fabrication tools versus integrated circuits. This split defines distinct investment profiles, with Lam Research tied to capital equipment cycles and Analog Devices linked to end-market product demand.

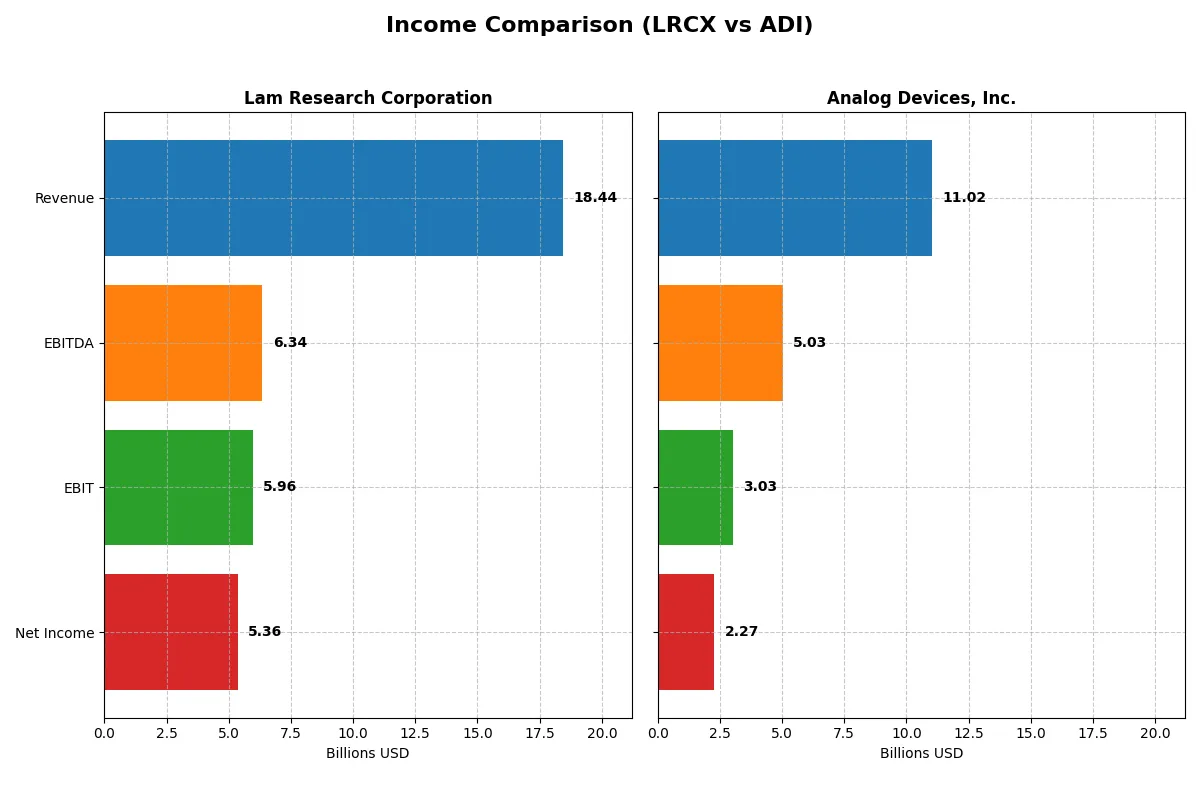

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Lam Research Corporation (LRCX) | Analog Devices, Inc. (ADI) |

|---|---|---|

| Revenue | 18.4B | 11.0B |

| Cost of Revenue | 9.46B | 5.0B |

| Operating Expenses | 3.08B | 3.02B |

| Gross Profit | 9.0B | 6.0B |

| EBITDA | 6.34B | 5.03B |

| EBIT | 5.96B | 3.03B |

| Interest Expense | 178M | 318M |

| Net Income | 5.36B | 2.27B |

| EPS | 4.17 | 4.59 |

| Fiscal Year | 2025 | 2025 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison exposes the true operational efficiency and profit generation of two leading semiconductor equipment and components firms.

Lam Research Corporation Analysis

Lam Research’s revenue surged from $14.9B in 2024 to $18.4B in 2025, a 23.7% jump reflecting strong demand momentum. The company sustains robust margin health with a gross margin near 49% and net margin exceeding 29%, signaling excellent cost control. In 2025, net income rose sharply by 40% to $5.36B, underlining efficient capital allocation and operating leverage.

Analog Devices, Inc. Analysis

Analog Devices grew revenue 17% to $11B in 2025, showing solid but more moderate top-line expansion. It maintains a higher gross margin of 54.7% but a lower net margin at 20.6%, indicating higher operating expenses relative to sales. Despite this, net income jumped 39% to $2.27B, driven by a 44% rise in EBIT, reflecting improving operational efficiency and margin expansion.

Margin Mastery vs. Growth Acceleration

Lam Research excels in translating revenue growth into superior net profitability with a 29% net margin versus Analog’s 21%. Yet, Analog Devices outpaces Lam in overall revenue and net income growth over five years, with 51% and 63% gains respectively. For investors, Lam’s profile suits those prioritizing margin strength and earnings quality. Analog appeals to those focused on faster growth and improving operational leverage.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | Lam Research Corporation (LRCX) | Analog Devices, Inc. (ADI) |

|---|---|---|

| ROE | 54.3% | 6.7% |

| ROIC | 34.0% | 5.5% |

| P/E | 23.4 | 51.1 |

| P/B | 12.7 | 3.4 |

| Current Ratio | 2.21 | 2.19 |

| Quick Ratio | 1.55 | 1.68 |

| D/E (Debt-to-Equity) | 0.48 | 0.26 |

| Debt-to-Assets | 22.3% | 18.1% |

| Interest Coverage | 33.1 | 9.5 |

| Asset Turnover | 0.86 | 0.23 |

| Fixed Asset Turnover | 7.59 | 3.32 |

| Payout ratio | 21.5% | 84.9% |

| Dividend yield | 0.92% | 1.66% |

| Fiscal Year | 2025 | 2025 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios serve as a company’s DNA, uncovering hidden risks and operational strengths shaping investment outcomes.

Lam Research Corporation

Lam Research posts a robust ROE of 54.33% and a strong net margin of 29.06%, signaling outstanding profitability. Its P/E ratio of 23.36 appears fairly valued in a capital-intensive sector. The company returns capital via modest dividends (0.92% yield) while heavily reinvesting in R&D, fueling innovation and growth.

Analog Devices, Inc.

Analog Devices shows a modest ROE of 6.7% and a net margin of 20.58%, indicating lower profitability efficiency. The stock trades at a lofty P/E of 51.05, suggesting stretched valuation. ADI balances shareholder returns with a 1.66% dividend yield but faces challenges in asset turnover, reflecting operational constraints.

Profitability Leadership vs. Valuation Stretch

Lam Research offers superior profitability and a more balanced valuation profile compared to Analog Devices’ stretched multiples and weaker returns. Investors prioritizing operational excellence may favor Lam’s profile, while those seeking yield amid valuation risk might consider Analog’s approach.

Which one offers the Superior Shareholder Reward?

I compare Lam Research Corporation (LRCX) and Analog Devices, Inc. (ADI) on dividends, payout ratios, and buybacks. LRCX yields ~0.9% with a payout ratio near 21-27%, supported by strong free cash flow (FCF) coverage around 3.2x. ADI pays a higher yield of ~1.6-2.1% but with a payout ratio often exceeding 80%, sometimes above 100%, signaling less cushion. Both firms execute share buybacks, but LRCX’s buyback intensity complements its moderate dividends better. LRCX’s balanced distribution and robust FCF yield a more sustainable total return. I favor LRCX for superior shareholder reward in 2026.

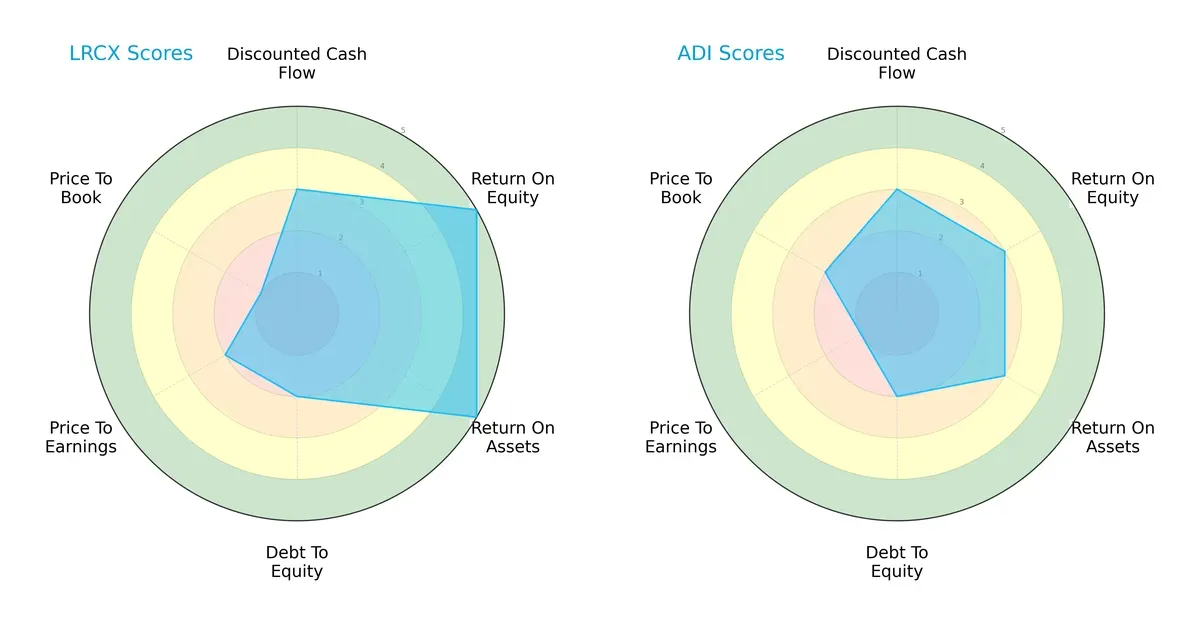

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Lam Research Corporation and Analog Devices, Inc., highlighting their financial strengths and valuation nuances:

Lam Research demonstrates superior efficiency with top ROE and ROA scores (5 each) compared to Analog Devices’ moderate scores (3 each). Both share moderate DCF and debt-to-equity profiles (score 3 and 2, respectively), but Lam faces valuation challenges, scoring poorly on price-to-book (1) and moderately on price-to-earnings (2). Analog Devices offers a more balanced valuation profile, though it lacks Lam’s operational edge. Overall, Lam relies on operational excellence, while Analog Devices maintains steadier valuation metrics.

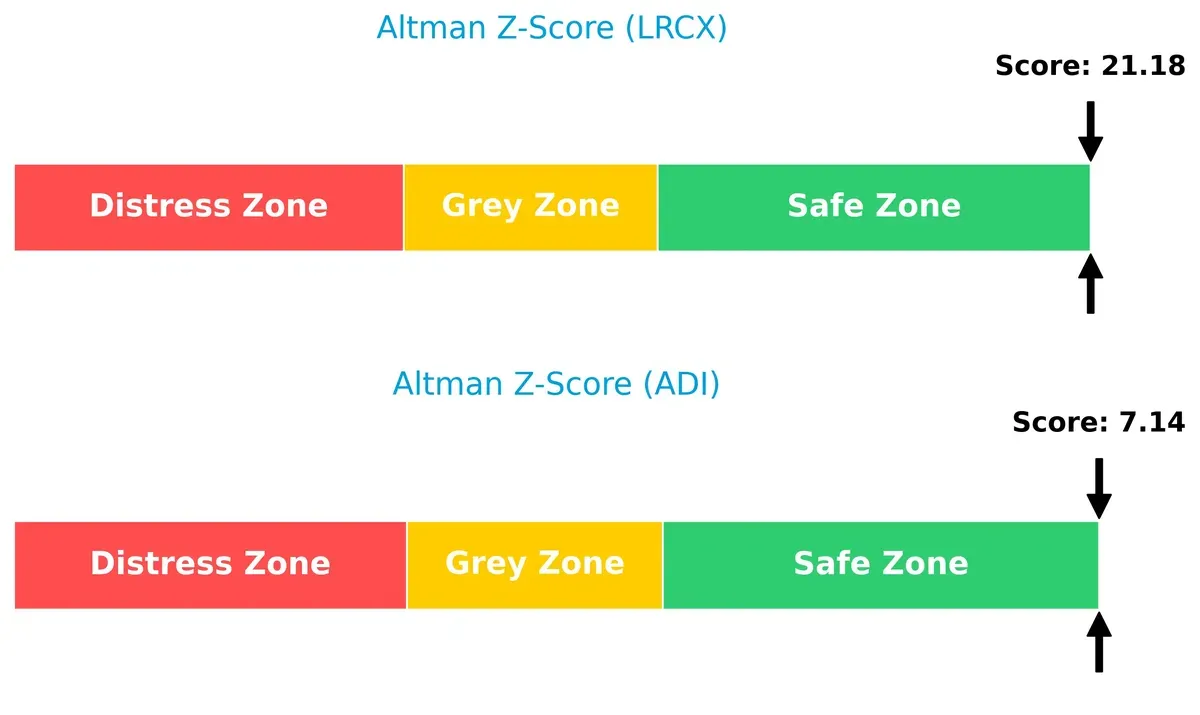

Bankruptcy Risk: Solvency Showdown

Lam Research’s Altman Z-Score (21.18) far exceeds Analog Devices’ (7.14), indicating a vastly stronger solvency position in the current cycle:

Both firms sit comfortably in the safe zone, but Lam’s exceptionally high score signals robust financial resilience and a lower bankruptcy risk.

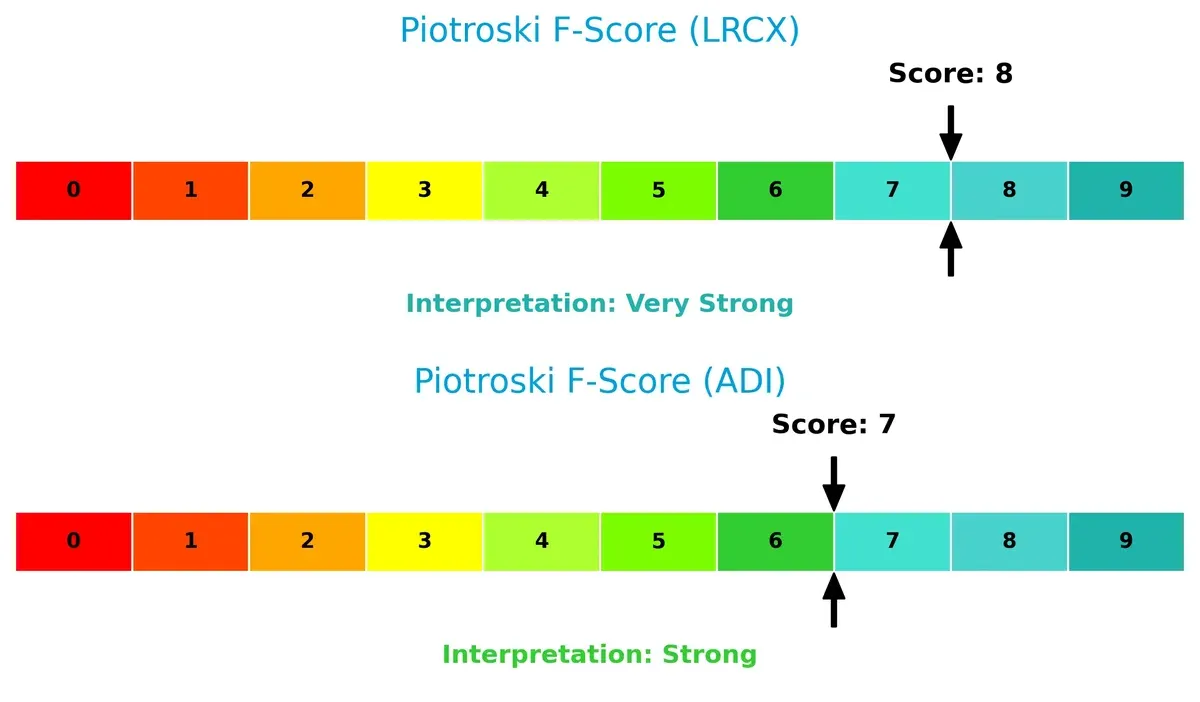

Financial Health: Quality of Operations

Lam Research scores an 8 on the Piotroski F-Score, edging out Analog Devices’ strong 7, reflecting slightly better internal financial health and operational quality:

Lam’s near-peak score signals few red flags, while Analog Devices, though solid, shows marginally weaker financial metrics, suggesting a cautious preference for Lam in terms of quality of operations.

How are the two companies positioned?

This section dissects the operational DNA of Lam Research and Analog Devices by comparing their revenue distribution and internal dynamics. We confront their economic moats to reveal which model ensures the most resilient competitive advantage today.

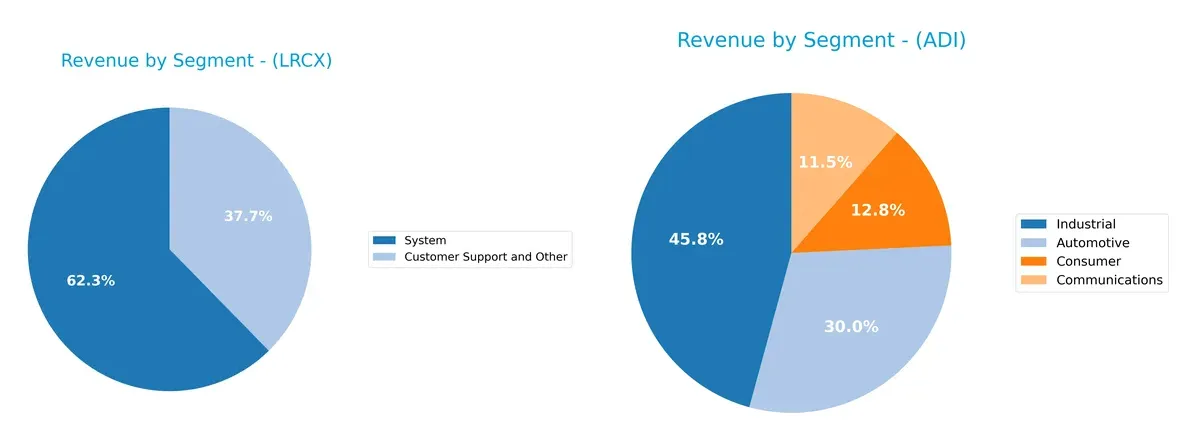

Revenue Segmentation: The Strategic Mix

The following visual comparison dissects how Lam Research Corporation and Analog Devices, Inc. diversify their income streams and where their primary sector bets lie:

Lam Research leans heavily on its System segment, which dwarfs its Customer Support and Other revenue at $11.5B vs. $6.9B in 2025. Analog Devices shows a more balanced portfolio, with Industrial leading at $4.3B but strong contributions from Automotive ($2.8B), Consumer ($1.2B), and Communications ($1.1B). Lam’s concentration signals infrastructure dominance but raises concentration risk. ADI’s diversified mix reduces dependency on any single sector, enhancing resilience.

Strengths and Weaknesses Comparison

This table compares the Strengths and Weaknesses of Lam Research Corporation and Analog Devices, Inc.:

Lam Research Corporation Strengths

- Strong profitability with 29.06% net margin and 54.33% ROE

- Favorable capital efficiency with 34.0% ROIC vs 12.05% WACC

- Solid liquidity ratios: current 2.21 and quick 1.55

- Low leverage and excellent interest coverage

- Diverse revenue from Systems and Customer Support

- Significant market presence in Asia, especially China and Korea

Analog Devices, Inc. Strengths

- Stable net margin of 20.58% and favorable current and quick ratios

- Low debt-to-equity at 0.26 with good interest coverage

- Diversified revenues across Automotive, Communications, Consumer, and Industrial sectors

- Balanced geographic presence with strong US and European sales

- Consistent fixed asset turnover indicating asset utilization

Lam Research Corporation Weaknesses

- High weighted average cost of capital at 12.05% above ROIC

- Unfavorable price-to-book ratio at 12.69

- Relatively low dividend yield of 0.92%

- Neutral asset turnover at 0.86 indicating moderate efficiency

Analog Devices, Inc. Weaknesses

- Low ROE at 6.7% signals poor shareholder returns

- Low ROIC of 5.55% close to WACC of 8.38%, indicating weak value creation

- Unfavorable high P/E at 51.05 and P/B at 3.42

- Unfavorable asset turnover at 0.23 suggests inefficient asset use

Lam Research excels in profitability and capital efficiency but faces valuation and cost of capital challenges. Analog Devices offers diversification and liquidity but struggles with returns and valuation metrics. These contrasting profiles imply different strategic priorities for each company.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat alone protects long-term profits from relentless competitive erosion by rivals and new entrants, ensuring sustainable value creation:

Lam Research Corporation: Precision Engineering and Process Expertise

Lam Research exploits high switching costs and specialized semiconductor equipment. Its very favorable ROIC above WACC signals durable value creation. New plasma and deposition tech in 2026 could deepen this edge.

Analog Devices, Inc.: Innovation in Mixed-Signal Integration

ADI’s moat centers on intangible assets and innovation in analog and mixed-signal ICs, contrasting Lam’s equipment focus. Despite a slightly unfavorable ROIC vs. WACC, ADI’s strong ROIC growth hints at improving profitability and market expansion potential.

Capital Efficiency vs. Innovation Momentum

Lam Research commands a wider, more durable moat through superior capital efficiency and value creation. ADI shows promising momentum but currently struggles to convert innovation into economic profit. Lam is better positioned to defend its market share amid intensifying semiconductor competition.

Which stock offers better returns?

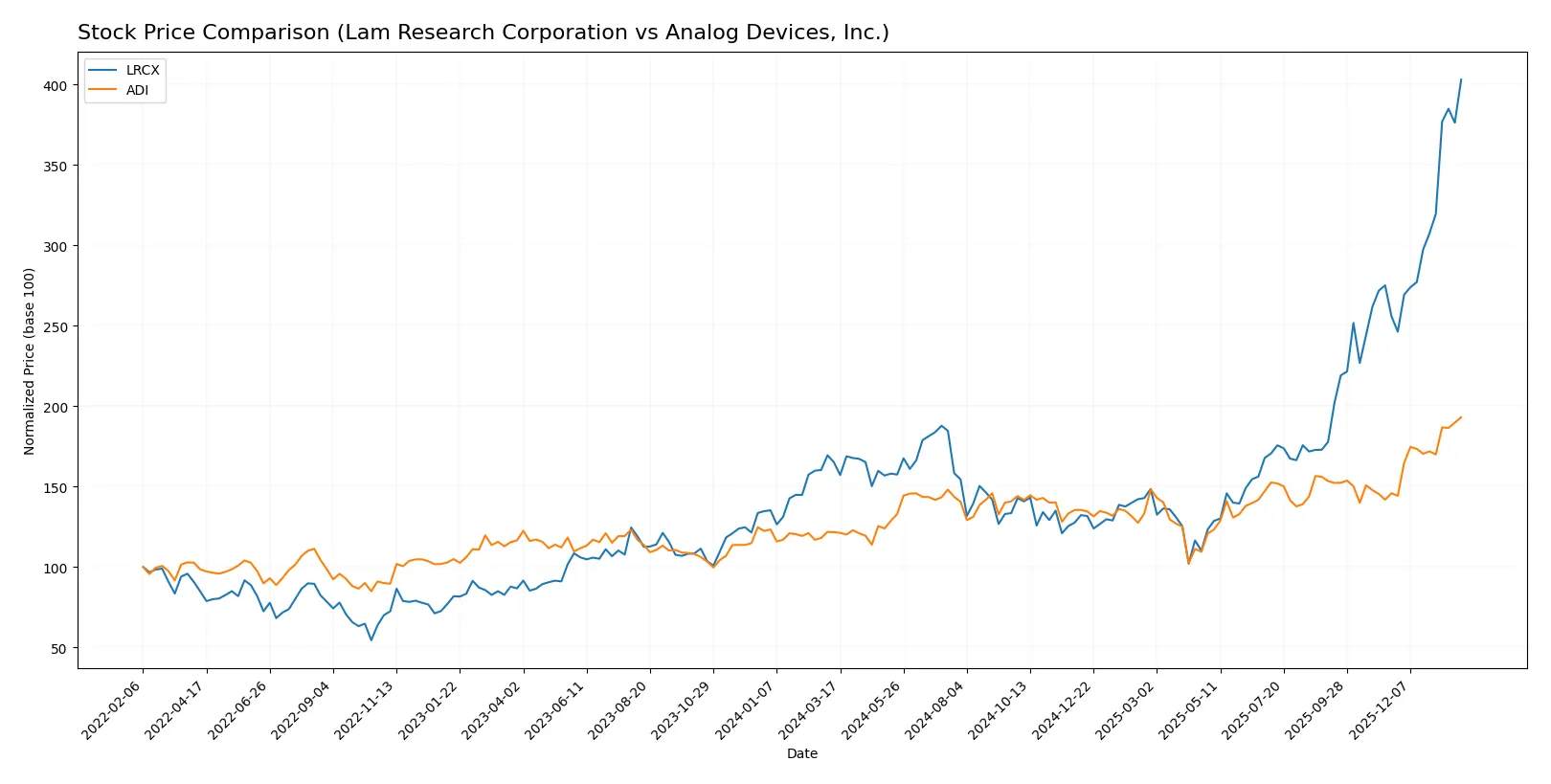

The past year saw Lam Research and Analog Devices both posting strong gains, with Lam Research showing pronounced acceleration and higher volatility compared to Analog Devices.

Trend Comparison

Lam Research’s stock surged 144.03% over the last 12 months, exhibiting a bullish trend with accelerating momentum and a notable high of 233.46. Its volatility, measured by a 36.82 standard deviation, remains elevated.

Analog Devices gained 58.66% during the same period, also bullish with acceleration. It hit a top price of 310.88 and had lower volatility at a 26.38 standard deviation, indicating steadier price movement.

Lam Research outperformed Analog Devices by a wide margin, delivering the highest market returns and stronger momentum over the past year.

Target Prices

Analysts show a positive outlook on both Lam Research Corporation and Analog Devices, Inc.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Lam Research Corporation | 127 | 325 | 266.76 |

| Analog Devices, Inc. | 270 | 375 | 316 |

The consensus target prices exceed current stock prices, signaling expected upside potential for LRCX and ADI. This reflects confidence in their market positions and growth prospects.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

The following tables summarize recent institutional grades for Lam Research Corporation and Analog Devices, Inc.:

Lam Research Corporation Grades

This table shows the most recent grades and actions from leading financial institutions for Lam Research Corporation.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Citigroup | Maintain | Buy | 2026-01-29 |

| RBC Capital | Maintain | Outperform | 2026-01-29 |

| Needham | Maintain | Buy | 2026-01-29 |

| Cantor Fitzgerald | Maintain | Overweight | 2026-01-29 |

| Goldman Sachs | Maintain | Buy | 2026-01-29 |

| Morgan Stanley | Maintain | Equal Weight | 2026-01-29 |

| Wells Fargo | Maintain | Overweight | 2026-01-29 |

| Evercore ISI Group | Maintain | Outperform | 2026-01-29 |

| Susquehanna | Maintain | Positive | 2026-01-29 |

| JP Morgan | Maintain | Overweight | 2026-01-29 |

Analog Devices, Inc. Grades

This table presents the latest institutional grades and rating changes for Analog Devices, Inc.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Susquehanna | Maintain | Positive | 2026-01-22 |

| B of A Securities | Maintain | Buy | 2026-01-21 |

| Stifel | Maintain | Buy | 2026-01-16 |

| Oppenheimer | Maintain | Outperform | 2026-01-16 |

| Wells Fargo | Upgrade | Overweight | 2026-01-15 |

| Citigroup | Maintain | Buy | 2026-01-15 |

| Keybanc | Maintain | Overweight | 2026-01-13 |

| Truist Securities | Maintain | Hold | 2025-12-19 |

| UBS | Maintain | Buy | 2025-12-08 |

| Truist Securities | Maintain | Hold | 2025-11-26 |

Which company has the best grades?

Lam Research holds consistently strong grades, mostly Buy to Outperform, with no downgrades. Analog Devices features a mix of Buy, Outperform, and Hold grades, with a recent upgrade from Wells Fargo. Lam Research’s uniformly positive outlook may signal stronger institutional confidence, potentially influencing investors’ perception of stability and growth prospects.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing Lam Research Corporation and Analog Devices, Inc. in the 2026 market environment:

1. Market & Competition

Lam Research Corporation

- Faces intense rivalry in semiconductor equipment, requiring constant innovation to maintain edge.

Analog Devices, Inc.

- Operates in diverse analog and mixed-signal markets, but slower asset turnover signals competitive pressure.

2. Capital Structure & Debt

Lam Research Corporation

- Maintains moderate debt (D/E 0.48) with strong interest coverage (33.4x), indicating solid debt management.

Analog Devices, Inc.

- Lower leverage (D/E 0.26) and good interest coverage (9.5x) suggest conservative financial risk.

3. Stock Volatility

Lam Research Corporation

- High beta of 1.78 reflects greater price swings and market sensitivity.

Analog Devices, Inc.

- Beta near 1.03 implies relatively stable stock with less volatility risk.

4. Regulatory & Legal

Lam Research Corporation

- Global operations expose it to complex semiconductor export controls and IP regulations.

Analog Devices, Inc.

- Diverse end markets and global footprint increase exposure to evolving tech regulations.

5. Supply Chain & Operations

Lam Research Corporation

- Complex supply chain for specialized semiconductor tools; vulnerable to material shortages.

Analog Devices, Inc.

- Faces supply chain challenges in components for analog and mixed-signal devices but benefits from operational scale.

6. ESG & Climate Transition

Lam Research Corporation

- Pressure to reduce carbon footprint in manufacturing equipment and energy consumption.

Analog Devices, Inc.

- Increasing demand for energy-efficient chips aligns with climate transition trends, offering opportunity and risk.

7. Geopolitical Exposure

Lam Research Corporation

- Significant sales in Asia, especially China, face geopolitical tensions and export restrictions.

Analog Devices, Inc.

- Also exposed to Asia-Pacific risks but with more diversified end markets mitigating concentrated geopolitical threat.

Which company shows a better risk-adjusted profile?

Lam Research’s biggest risk lies in volatile market competition and geopolitical exposure in Asia. Analog Devices faces valuation and operational efficiency challenges but benefits from lower volatility and debt. I see Analog Devices as having a more balanced risk-adjusted profile, supported by its stable beta and conservative leverage. Lam’s high beta and heavy dependency on semiconductor capex cycles heighten its risk. Recent declines in LRCX’s share price (-5.9%) versus ADI’s milder drop (-2.5%) underscore market nervousness about Lam’s cyclical vulnerability.

Final Verdict: Which stock to choose?

Lam Research Corporation (LRCX) excels as a cash-generating powerhouse with a durable competitive moat. Its impressive capital efficiency and robust profitability stand out. The point of vigilance lies in its relatively high price-to-book ratio, which could temper near-term valuation appeal. LRCX suits an aggressive growth portfolio seeking sustained value creation.

Analog Devices, Inc. (ADI) offers a strategic moat rooted in its recurring revenue model and strong R&D investment. It presents a safer balance sheet with lower leverage than LRCX, appealing to more risk-averse investors. ADI fits well within a GARP (Growth at a Reasonable Price) profile, balancing growth potential and capital preservation.

If you prioritize capital efficiency and strong economic moats, LRCX is the compelling choice due to its superior ROIC over WACC and solid free cash flow generation. However, if you seek stability and consistent earnings growth with a defensive tilt, ADI offers better stability through its recurring revenue and manageable debt load. Both names command attention but cater to distinct investor avatars.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Lam Research Corporation and Analog Devices, Inc. to enhance your investment decisions: