Home > Comparison > Industrials > AME vs SYM

The strategic rivalry between AMETEK, Inc. and Symbotic Inc. shapes the future of industrial machinery. AMETEK operates as a diversified industrial giant with broad electromechanical solutions, while Symbotic focuses on high-tech warehouse automation. This head-to-head highlights a clash between established industrial scale and innovative automation growth. This analysis aims to identify which corporate path presents the superior risk-adjusted opportunity for a diversified investor in the evolving industrial sector.

Table of contents

Companies Overview

AMETEK and Symbotic represent two powerful forces in the industrial machinery sector shaping automation and instrumentation markets.

AMETEK, Inc.: Industrial Instrumentation Leader

AMETEK dominates with a diversified portfolio in electronic instruments and electromechanical devices. Its core revenue derives from advanced instruments serving aerospace, process, and industrial markets. In 2026, AMETEK emphasizes innovation across Electronic Instruments and Electromechanical segments, targeting aerospace sensors and precision motion controls as strategic growth drivers.

Symbotic Inc.: Warehouse Automation Pioneer

Symbotic specializes in robotics and automation technology, focusing on enhancing efficiency for US retailers and wholesalers. Its revenue engine is The Symbotic System, an integrated warehouse automation platform that cuts costs and optimizes inventory. In 2026, Symbotic prioritizes scaling its full-service automation solutions to capture more logistics and supply chain market share.

Strategic Collision: Similarities & Divergences

AMETEK and Symbotic share a commitment to industrial machinery but differ fundamentally. AMETEK relies on a broad, product-diverse model with deep instrumentation expertise. Symbotic pursues a focused, technology-driven approach with a closed automation ecosystem. Their main battleground is operational efficiency in manufacturing and logistics. These contrasts create distinct investment profiles: AMETEK as a stable, diversified industrial giant, Symbotic as a high-growth automation disruptor.

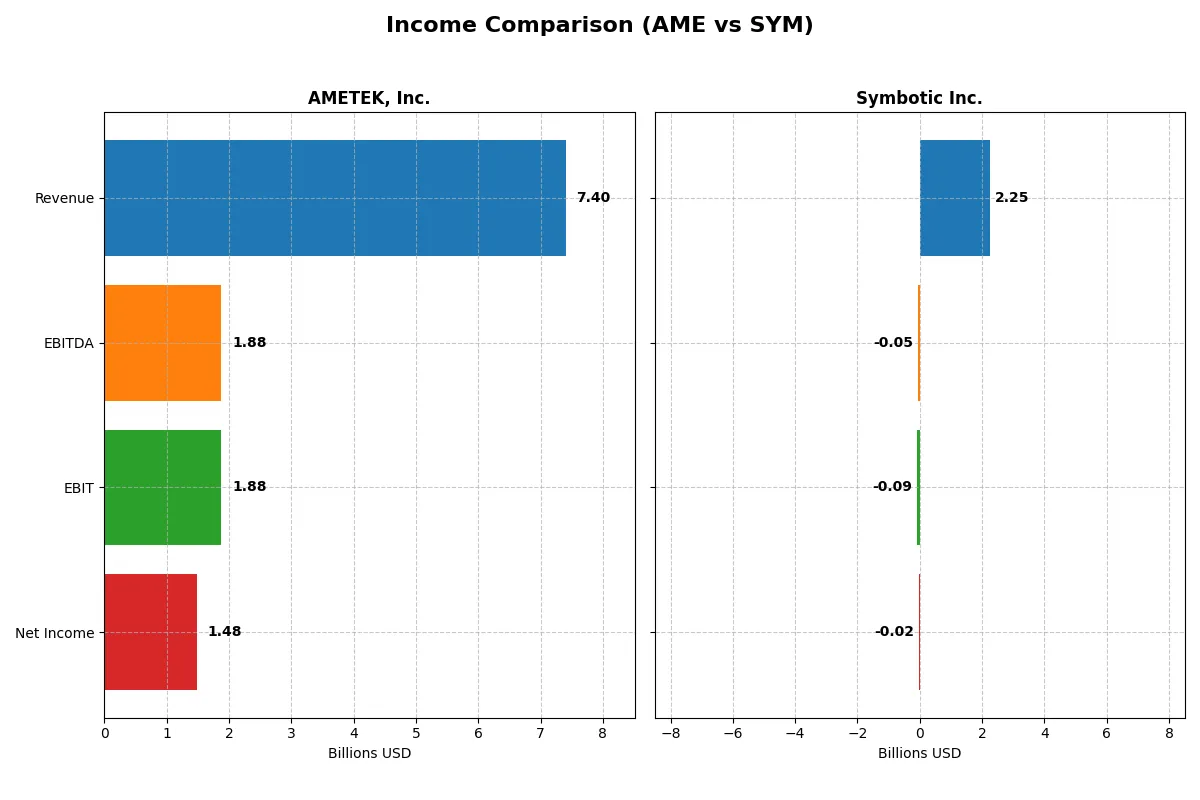

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | AMETEK, Inc. (AME) | Symbotic Inc. (SYM) |

|---|---|---|

| Revenue | 7.4B | 2.2B |

| Cost of Revenue | 4.7B | 1.8B |

| Operating Expenses | 757M | 538M |

| Gross Profit | 2.7B | 423M |

| EBITDA | 1.9B | -48M |

| EBIT | 1.9B | -92M |

| Interest Expense | 81M | 0 |

| Net Income | 1.5B | -17M |

| EPS | 6.42 | -0.16 |

| Fiscal Year | 2025 | 2025 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals each company’s core efficiency in turning revenue into profit over recent years.

AMETEK, Inc. Analysis

AMETEK’s revenue grew steadily from 5.5B in 2021 to 7.4B in 2025, with net income rising from 990M to 1.48B. Its gross margin holds at a strong 36.4%, while net margin sits at a healthy 20%. In 2025, AMETEK maintained momentum with favorable EBIT and EPS growth, reflecting disciplined cost control despite rising operating expenses.

Symbotic Inc. Analysis

Symbotic expanded revenue sharply from 250M in 2021 to 2.25B in 2025, yet it reported a net loss of 17M in 2025. Its gross margin improved to 18.8%, but EBIT and net margins remain negative, signaling ongoing operational inefficiencies. Despite strong top-line growth, Symbotic’s profitability struggles, with deteriorating EBIT and EPS in the latest year.

Margin Strength vs. Growth Scale

AMETEK delivers consistent profitability and margin expansion, backed by solid revenue and net income growth. In contrast, Symbotic boasts impressive revenue scale but remains unprofitable with negative margins. For investors prioritizing fundamental earnings quality, AMETEK’s stable profit profile offers a more attractive risk-return balance than Symbotic’s high-growth yet loss-making model.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies analyzed:

| Ratios | AMETEK, Inc. (AME) | Symbotic Inc. (SYM) |

|---|---|---|

| ROE | 13.93% | -7.65% |

| ROIC | 11.04% | -16.63% |

| P/E | 31.97 | -334.54 |

| P/B | 4.45 | 25.60 |

| Current Ratio | 1.06 | 1.08 |

| Quick Ratio | 0.67 | 0.99 |

| D/E | 0.21 | 0.14 |

| Debt-to-Assets | 14.21% | 1.32% |

| Interest Coverage | 23.82 | 0 |

| Asset Turnover | 0.46 | 0.94 |

| Fixed Asset Turnover | 6.56 | 15.92 |

| Payout ratio | 19.31% | 0 |

| Dividend yield | 0.60% | 0 |

| Fiscal Year | 2025 | 2025 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios act as a company’s DNA, revealing hidden risks and operational excellence behind headline numbers.

AMETEK, Inc.

AMETEK posts a solid 20% net margin and decent 13.9% ROE, signaling steady profitability. Its P/E of 31.97 marks the stock as expensive relative to earnings. Despite this, AMETEK maintains a disciplined capital structure with favorable debt ratios and a modest 0.6% dividend yield, balancing shareholder returns with reinvestment in growth.

Symbotic Inc.

Symbotic shows negative profitability with a -0.75% net margin and -7.65% ROE, reflecting operational challenges. The stock’s P/E is negative but the high P/B of 25.6 suggests a stretched valuation. Symbotic pays no dividend, focusing instead on heavy R&D spending to fuel future growth, though this carries significant execution risk.

Premium Valuation vs. Operational Safety

AMETEK offers a more balanced risk-reward profile with favorable profitability and conservative leverage despite a rich valuation. Symbotic’s valuation appears stretched and profitability weak, implying higher risk. AMETEK suits investors prioritizing operational stability, while Symbotic fits those seeking high-growth speculative plays.

Which one offers the Superior Shareholder Reward?

I see AMETEK, Inc. (AME) offers a modest 0.62% dividend yield with a sustainable payout ratio near 19%. Its steady buyback program complements this, boosting total returns. Symbotic Inc. (SYM) pays no dividends but aggressively reinvests in growth, reflected in its negative margins and high free cash flow reinvestment. AME’s balanced distribution through dividends and buybacks provides a more reliable, long-term shareholder reward in 2026 compared to SYM’s riskier growth bet.

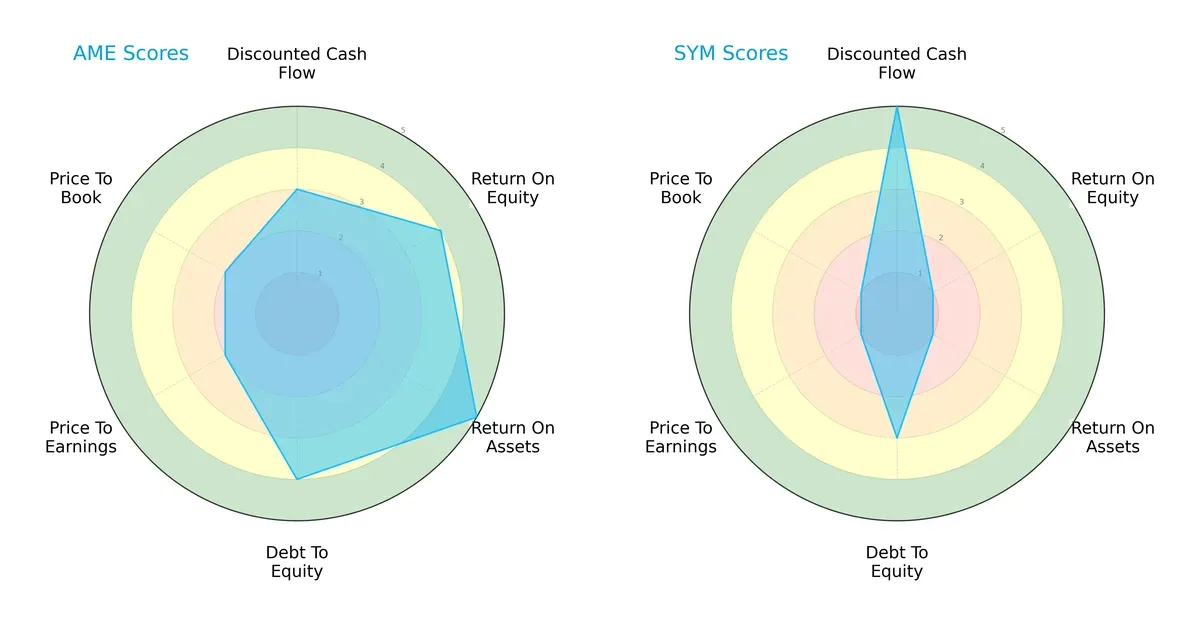

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of AMETEK, Inc. and Symbotic Inc., highlighting their core financial strengths and weaknesses:

AMETEK delivers a balanced profile with solid ROE (4) and ROA (5) scores, reflecting efficient asset use and profitability. It maintains prudent leverage (Debt/Equity score 4) but shows moderate valuation scores (P/E and P/B at 2). Symbotic leans heavily on its strong discounted cash flow (5) but struggles to generate returns, indicated by very low ROE and ROA scores (1 each). Its weaker valuation metrics and moderate debt profile reveal a company reliant on future growth rather than current profitability.

Bankruptcy Risk: Solvency Showdown

AMETEK’s Altman Z-Score of 8.15 versus Symbotic’s 10.83 places both firms well within the safe zone, underscoring robust financial stability and low bankruptcy risk in this cycle:

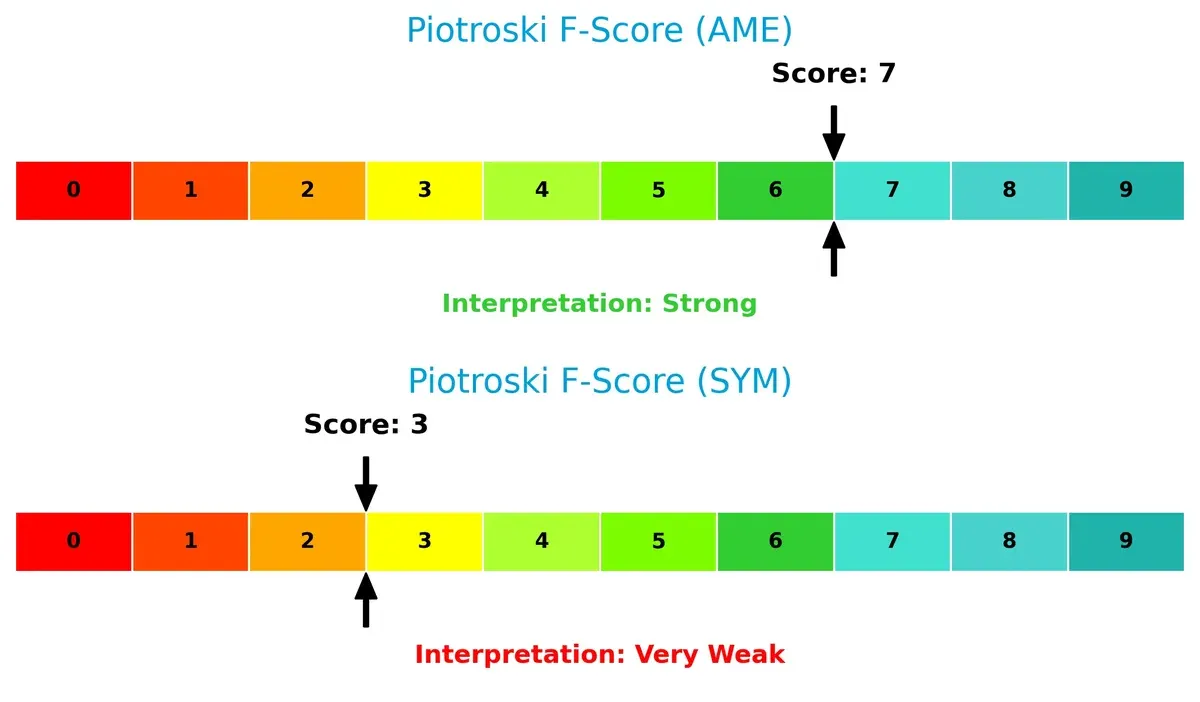

Financial Health: Quality of Operations

AMETEK’s strong Piotroski F-Score of 7 signifies solid operational health and financial quality. Symbotic’s score of 3 raises red flags, highlighting weaker profitability and internal metrics:

How are the two companies positioned?

This section dissects the operational DNA of AMETEK and Symbotic by comparing their revenue distribution and internal dynamics. The goal is to confront their economic moats and identify which model offers the most resilient competitive advantage today.

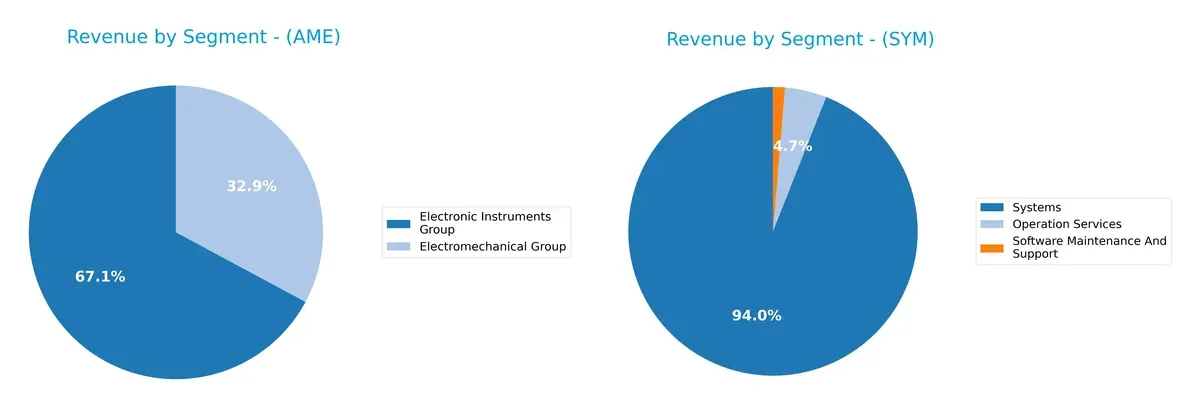

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how AMETEK, Inc. and Symbotic Inc. diversify their income streams and where their primary sector bets lie:

AMETEK displays a balanced revenue mix between its Electromechanical Group ($2.28B) and Electronic Instruments Group ($4.66B), reflecting strong dual-segment dominance. Symbotic, however, pivots heavily on its Systems segment ($2.12B), with smaller contributions from Operation Services ($105M) and Software Maintenance ($30M). AMETEK’s diversification reduces concentration risk, while Symbotic leans on infrastructure dominance, exposing it to sector-specific volatility.

Strengths and Weaknesses Comparison

This table compares the Strengths and Weaknesses of AMETEK, Inc. and Symbotic Inc.:

AMETEK, Inc. Strengths

- Diverse revenue streams from Electromechanical and Electronic Instruments groups

- Strong net margin at 20%

- ROIC above WACC at 11.04% indicates efficient capital use

- Low debt-to-assets ratio at 14.21%

- High fixed asset turnover at 6.56

- Established global presence with significant US, EU, and Asia sales

Symbotic Inc. Strengths

- Growing revenue in Systems segment reaching $2.1B in 2025

- Low debt-to-assets at 1.32%

- Favorable P/E ratio due to negative earnings

- Higher fixed asset turnover at 15.92

- Neutral current and quick ratios near 1

- Concentrated US market presence with expanding Non-US sales

AMETEK, Inc. Weaknesses

- Unfavorable valuation multiples: high P/E at 31.97 and P/B at 4.45

- Quick ratio at 0.67 signals liquidity risk

- Asset turnover low at 0.46, below sector norms

- Dividend yield low at 0.6%

- Moderate ROE at 13.93% with neutral WACC

- Heavy reliance on US and Asian markets

Symbotic Inc. Weaknesses

- Negative profitability metrics: net margin -0.75%, ROE -7.65%, ROIC -16.63%

- High WACC at 13.93% undermines returns

- Zero interest coverage suggests high risk

- Unfavorable P/B at 25.6

- No dividend yield

- Revenue heavily concentrated in US with limited geographic diversification

AMETEK shows a balanced profile with solid profitability and global diversification but faces valuation and liquidity challenges. Symbotic struggles with profitability and financial stability despite operational efficiency and growth focus in the US market. These contrasts shape each company’s strategic priorities moving forward.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only barrier protecting long-term profits from relentless competitive erosion. Let’s dissect two distinct moats in 2026:

AMETEK, Inc.: Diversified Industrial Powerhouse with Operational Excellence

AME’s primary moat stems from its diverse product portfolio and strong operational efficiency, driving a high ROIC above WACC by 2.5%. Stable 36% gross margins and 20% net margins confirm durable profitability. Expansion in aerospace and industrial instrumentation markets should deepen this moat further.

Symbotic Inc.: Cutting-Edge Automation with Emerging Scale Challenges

SYM relies on technology-driven cost advantages and network effects in warehouse automation. However, it currently operates at a negative EBIT margin, reflecting scale and execution risks. Despite rapid revenue growth (+25% last year), its declining ROIC signals a fragile moat. Future gains depend on scaling operations and market penetration.

Moat Strength Showdown: Diversification and Operational Efficiency vs. Innovation Growth

AME exhibits a wider and deeper moat with consistent value creation and growing profitability. SYM’s innovative technology faces steep scaling hurdles, eroding returns. AMETEK is better positioned to defend market share amid industrial competition.

Which stock offers better returns?

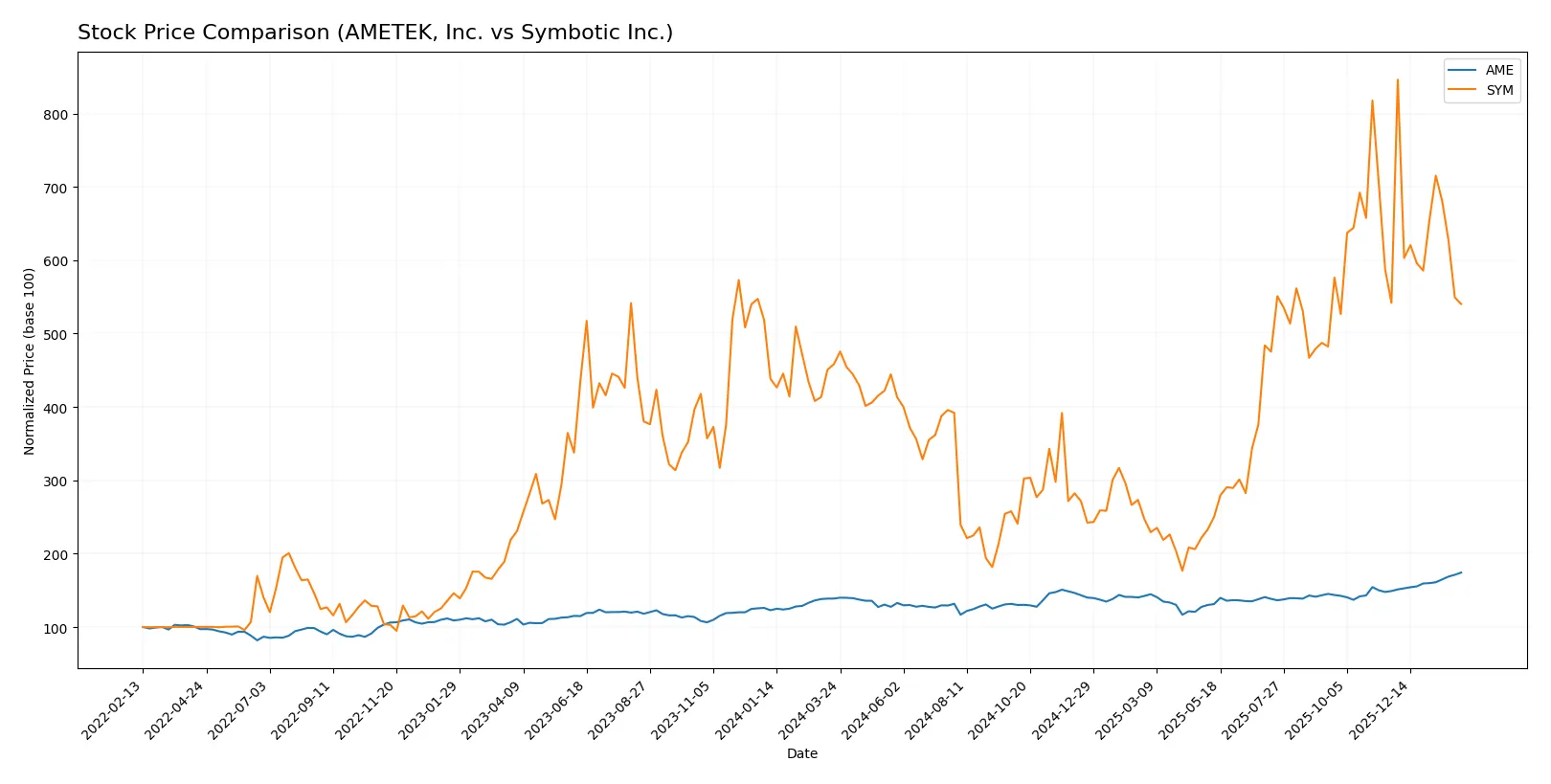

The past 12 months reveal AMETEK’s sharp 25.5% price gain with accelerating momentum, while Symbotic’s 17.9% rise slowed, showing recent slight weakness in trading dynamics.

Trend Comparison

AMETEK’s stock advanced 25.5% over the last year, marking a bullish trend with accelerating gains and a high volatility level of 14.42%. It reached a peak of 227.83 and a low of 152.66.

Symbotic’s stock gained 17.9% overall, maintaining a bullish but decelerating trend. Its recent period showed a slight price decline of 0.3%. Volatility stands at 15.71%, with a high of 83.77 and a low of 17.5.

AMETEK outperformed Symbotic with stronger price appreciation and accelerating momentum, delivering the highest market performance over the past year.

Target Prices

Analysts present a positive target price consensus for both AMETEK, Inc. and Symbotic Inc., indicating potential upside from current levels.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| AMETEK, Inc. | 204 | 271 | 237.91 |

| Symbotic Inc. | 42 | 83 | 65.56 |

The consensus target for AMETEK at $237.91 suggests modest upside from its $227.83 price. Symbotic’s $65.56 consensus implies significant potential above its $53.48 trading price.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

This section compares recent institutional grades assigned to AMETEK, Inc. and Symbotic Inc.:

AMETEK, Inc. Grades

The table below shows AMETEK’s latest grades from major financial institutions.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Keybanc | maintain | Overweight | 2026-02-04 |

| DA Davidson | maintain | Buy | 2026-02-04 |

| Barclays | maintain | Equal Weight | 2026-02-04 |

| Oppenheimer | downgrade | Perform | 2026-01-27 |

| Morgan Stanley | maintain | Equal Weight | 2026-01-12 |

| Barclays | maintain | Equal Weight | 2026-01-07 |

| Keybanc | maintain | Overweight | 2026-01-07 |

| Keybanc | maintain | Overweight | 2026-01-06 |

| Mizuho | maintain | Outperform | 2026-01-05 |

| TD Cowen | upgrade | Buy | 2025-12-23 |

Symbotic Inc. Grades

Below are recent grades from major institutions for Symbotic Inc.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Needham | maintain | Buy | 2026-02-05 |

| Barclays | maintain | Underweight | 2026-01-12 |

| Goldman Sachs | downgrade | Sell | 2025-12-02 |

| Barclays | maintain | Underweight | 2025-11-26 |

| Baird | maintain | Neutral | 2025-11-26 |

| Needham | maintain | Buy | 2025-11-25 |

| Cantor Fitzgerald | maintain | Overweight | 2025-11-25 |

| Northland Capital Markets | maintain | Outperform | 2025-11-25 |

| Craig-Hallum | upgrade | Buy | 2025-11-25 |

| DA Davidson | maintain | Neutral | 2025-11-25 |

Which company has the best grades?

AMETEK holds predominantly positive grades with multiple “Buy” and “Overweight” ratings. Symbotic shows mixed signals, including a recent “Sell” downgrade. Investors may see AMETEK’s grades as more favorable and consistent.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

AMETEK, Inc.

- Established player with diverse product lines in industrial machinery; faces steady competition but benefits from scale and legacy relationships.

Symbotic Inc.

- Emerging automation technology firm with innovative robotics; faces intense competition and pressure to scale rapidly in a dynamic market.

2. Capital Structure & Debt

AMETEK, Inc.

- Conservative leverage with 0.21 debt-to-equity ratio; strong interest coverage at 23.13x reduces financial risk.

Symbotic Inc.

- Very low debt-to-equity at 0.14 but zero interest coverage indicates operational losses and potential liquidity concerns.

3. Stock Volatility

AMETEK, Inc.

- Beta near 1.04 suggests stock moves roughly with the market; moderate volatility.

Symbotic Inc.

- High beta of 2.14 signals significant share price swings; elevated risk for traders and investors.

4. Regulatory & Legal

AMETEK, Inc.

- Operates globally with compliance in industrial sectors; typical regulatory risks but no major legal red flags.

Symbotic Inc.

- Robotics automation sector faces evolving regulations; exposure to compliance risk as technology develops and scales.

5. Supply Chain & Operations

AMETEK, Inc.

- Diversified supply chain with legacy operational stability; potential bottlenecks from global industrial supply constraints.

Symbotic Inc.

- Dependent on cutting-edge components; supply chain disruptions could severely impact technology deployment and growth.

6. ESG & Climate Transition

AMETEK, Inc.

- Mid-sized industrial firm with growing ESG initiatives; faces pressure to improve sustainability metrics amidst sector transition.

Symbotic Inc.

- Innovative tech company with opportunity to lead on ESG but must navigate carbon footprint of robotics manufacturing.

7. Geopolitical Exposure

AMETEK, Inc.

- Global footprint includes aerospace and defense sectors; exposed to trade tensions and international regulatory shifts.

Symbotic Inc.

- Primarily US-focused but reliant on global supply chains; geopolitical disruptions could impact access to key components.

Which company shows a better risk-adjusted profile?

AMETEK’s strongest risk is moderate market competition and operational complexity, but it maintains robust financial health and stable capital structure. Symbotic faces the most impactful risk in operational losses and high stock volatility, undermining financial stability despite a promising innovation profile. AMETEK’s Altman Z-score of 8.15 and solid Piotroski score of 7 contrast sharply with Symbotic’s weaker Piotroski of 3, reflecting greater financial resilience. The recent sharp 4.7% share price drop in Symbotic underscores heightened market volatility and investor concern. Overall, AMETEK presents a superior risk-adjusted profile for cautious investors focused on financial strength and stability.

Final Verdict: Which stock to choose?

AMETEK, Inc. leverages its unmatched capital efficiency and a proven ability to generate increasing returns on invested capital. Its strong economic moat signals a durable competitive advantage. A point of vigilance is its moderate liquidity position, which could pressure short-term flexibility. This stock fits well in an Aggressive Growth portfolio focused on stability and steady value creation.

Symbotic Inc. offers a strategic moat rooted in high free cash flow yield and rapid revenue growth, driven by innovation in automation. However, it currently destroys value and faces profitability challenges, indicating higher risk. Compared to AMETEK, Symbotic presents a more speculative profile suited for Growth at a Reasonable Price (GARP) investors willing to tolerate volatility.

If you prioritize consistent value creation and a strong financial fortress, AMETEK outshines as the compelling choice due to its sustainable moat and favorable profitability metrics. However, if you seek high-growth potential with a tolerance for operational risks, Symbotic offers superior upside through technological innovation and expanding market presence, albeit with a premium risk profile.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of AMETEK, Inc. and Symbotic Inc. to enhance your investment decisions: