Home > Comparison > Technology > GOOGL vs META

The strategic rivalry between Alphabet Inc. and Meta Platforms defines the current trajectory of the technology sector. Alphabet operates as a diversified tech titan with strong cloud and advertising arms. Meta focuses on social connectivity and immersive reality innovations, blending digital engagement with emerging hardware. This analysis pits Alphabet’s broad platform dominance against Meta’s focused social ecosystem to identify which offers superior risk-adjusted returns for diversified portfolios.

Table of contents

Companies Overview

Alphabet Inc. and Meta Platforms dominate the digital landscape with vast user bases and innovation-driven revenue models.

Alphabet Inc.: The Search and Cloud Giant

Alphabet Inc. defines internet content and information leadership through its Google Services and Cloud segments. Its core revenue stems from advertising across Search, YouTube, and Play Store ecosystems. In 2026, it strategically emphasizes expanding Google Cloud infrastructure and enterprise collaboration tools, driving diversification beyond advertising.

Meta Platforms, Inc.: Social Connectivity Pioneer

Meta Platforms commands the social media and virtual reality arenas with its Family of Apps and Reality Labs. It generates revenue primarily from advertising on Facebook, Instagram, and WhatsApp. Meta’s 2026 strategy centers on immersive experiences through augmented and virtual reality hardware, aiming to redefine social interaction in the metaverse era.

Strategic Collision: Similarities & Divergences

Both companies monetize digital engagement but diverge in approach: Alphabet prioritizes a broad ecosystem with open infrastructure, while Meta focuses on a closed, immersive social environment. Their primary battleground lies in capturing advertising dollars and user attention across platforms. This results in distinct investment profiles—Alphabet balances mature cloud growth with ad dominance; Meta bets heavily on metaverse innovation and user connectivity.

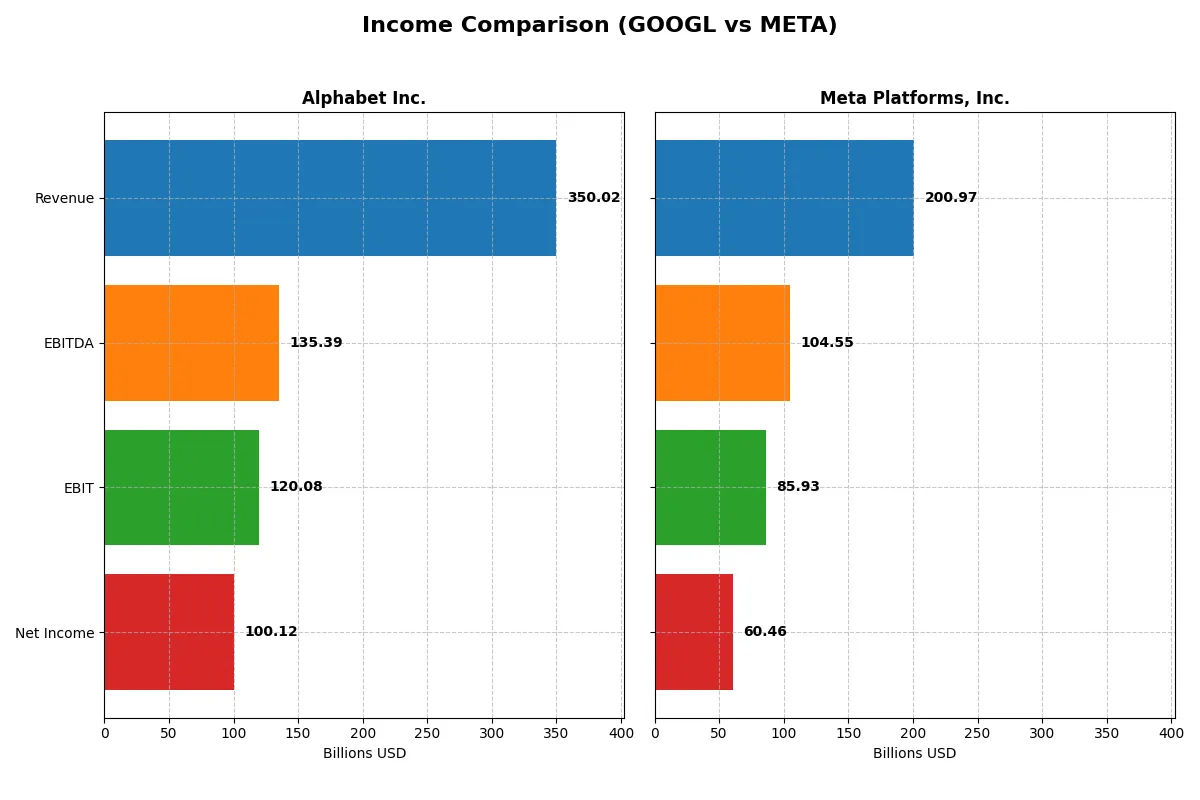

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Alphabet Inc. (GOOGL) | Meta Platforms, Inc. (META) |

|---|---|---|

| Revenue | 350B | 165B |

| Cost of Revenue | 146B | 30B |

| Operating Expenses | 91B | 65B |

| Gross Profit | 204B | 134B |

| EBITDA | 135B | 87B |

| EBIT | 120B | 71B |

| Interest Expense | 268M | 715M |

| Net Income | 100B | 62B |

| EPS | 8.13 | 24.61 |

| Fiscal Year | 2024 | 2024 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison uncovers which company runs its business engine with superior efficiency and profitability.

Alphabet Inc. Analysis

Alphabet steadily grew revenue from $183B in 2020 to $350B in 2024, with net income surging from $40B to $100B. Its gross margin hovers at a strong 58.2%, while net margin expanded to 28.6%. In 2024, Alphabet accelerated growth with a 13.9% revenue increase and a 39.6% EBIT jump, signaling robust operational momentum.

Meta Platforms, Inc. Analysis

Meta lifted revenue from $118B in 2021 to $201B in 2025, with net income rising from $39B to $60B. It commands a higher gross margin of 82.0% and net margin of 30.1%. However, Meta’s net margin declined by 20.6% in the last year despite 22.2% revenue growth, reflecting margin pressure amid rising operating expenses.

Margin Efficiency vs. Growth Dynamics

Alphabet leads with superior margin expansion and net income growth, nearly doubling net profits over five years. Meta boasts higher gross margins and faster revenue growth but struggles with margin contraction recently. For investors seeking steady profitability, Alphabet’s resilient margin profile offers more attractive fundamentals than Meta’s growth-at-all-costs approach.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared:

| Ratios | Alphabet Inc. (GOOGL) | Meta Platforms, Inc. (META) |

|---|---|---|

| ROE | 30.8% | 34.1% |

| ROIC | 25.8% | 25.1% |

| P/E | 23.3 | 23.8 |

| P/B | 7.2 | 8.1 |

| Current Ratio | 1.84 | 2.98 |

| Quick Ratio | 1.84 | 2.98 |

| D/E | 0.08 | 0.27 |

| Debt-to-Assets | 5.7% | 17.8% |

| Interest Coverage | 419x | 97x |

| Asset Turnover | 0.78 | 0.60 |

| Fixed Asset Turnover | 1.90 | 1.21 |

| Payout ratio | 7.4% | 8.1% |

| Dividend yield | 0.32% | 0.34% |

| Fiscal Year | 2024 | 2024 |

Efficiency & Valuation Duel: The Vital Signs

Ratios act as the company’s DNA, revealing hidden risks and operational excellence that drive long-term investor value and market positioning.

Alphabet Inc.

Alphabet shows a robust 30.8% ROE and a strong 28.6% net margin, signaling high profitability and operational efficiency. Its P/E of 23.3 appears fairly valued, though a 7.17 PB hints at premium pricing. Shareholders receive modest 0.32% dividends, while the company reinvests heavily in R&D, fueling growth and innovation.

Meta Platforms, Inc.

Meta posts a solid 27.8% ROE with a 30.1% net margin, reflecting efficient profit generation. However, its P/E of 27.5 and PB of 7.66 mark it as more expensive relative to peers. Meta returns value via a 0.32% dividend but balances this with significant spending on R&D to sustain competitive advantage and future growth.

Premium Valuation vs. Operational Safety

Both firms share a favorable ratio profile, yet Alphabet offers a better risk-reward balance with slightly lower valuation multiples and stronger capital returns. Meta suits investors seeking growth with higher valuation tolerance, while Alphabet appeals more to those favoring operational stability and measured pricing.

Which one offers the Superior Shareholder Reward?

I compare Alphabet and Meta’s shareholder rewards through their dividends, payout ratios, and share buybacks. Alphabet yields 0.32% with a 7.35% payout ratio, reflecting modest dividends fully covered by FCF. Meta yields slightly higher at 0.32% with an 8.8% payout ratio but shows less FCF coverage, indicating a riskier dividend. Alphabet has no recent buybacks, while Meta’s aggressive buybacks enhance total returns. Alphabet’s conservative payout and strong cash flow suggest sustainable rewards. Meta’s mix of dividends and buybacks drives growth but carries leverage risks. For 2026, I favor Alphabet’s disciplined model for steady, sustainable shareholder value.

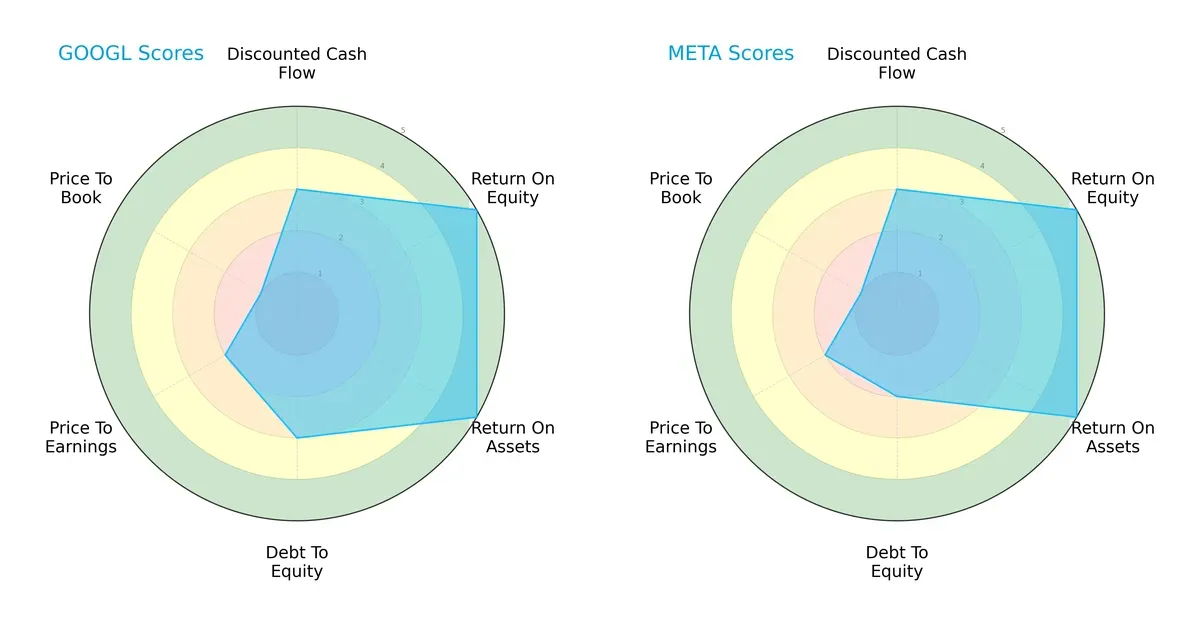

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Alphabet Inc. and Meta Platforms, showing their financial strengths and valuation nuances side by side:

Both firms share identical overall, DCF, ROE, and ROA scores, indicating similar operational efficiency and cash flow expectations. Alphabet holds an edge in debt management with a higher Debt/Equity score (3 vs. 2), reflecting a more balanced leverage position. Valuation scores (P/E and P/B) remain equally moderate to unfavorable, signaling caution on pricing. Alphabet’s profile appears more balanced, while Meta leans slightly on operational efficiency but with higher leverage risk.

Bankruptcy Risk: Solvency Showdown

Alphabet’s Altman Z-Score of 18.8 versus Meta’s 8.8 places both comfortably in the safe zone, but Alphabet’s superior score signals a stronger buffer against bankruptcy risks in this cycle:

Financial Health: Quality of Operations

Both Alphabet and Meta score a 6 on the Piotroski F-Score, indicating average financial health. Neither shows red flags internally, but neither stands out as exceptionally strong:

How are the two companies positioned?

This section dissects the operational DNA of Alphabet and Meta by comparing their revenue distribution and internal dynamics. The goal is to confront their economic moats to identify which model offers the most resilient competitive advantage today.

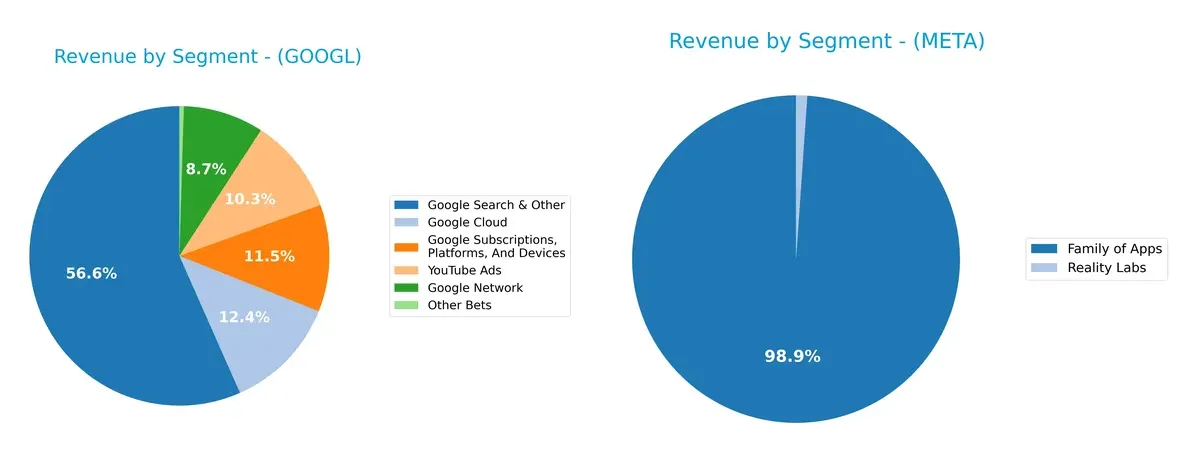

Revenue Segmentation: The Strategic Mix

This comparison dissects how Alphabet Inc. and Meta Platforms diversify their income streams and highlights their primary sector bets:

Alphabet dwarfs Meta in segment breadth, anchoring most revenue in Google Search & Other at $198B. Its Google Cloud and YouTube Ads segments, $43B and $36B respectively, diversify income effectively. Meta relies heavily on its Family of Apps segment at nearly $199B, with Reality Labs contributing a modest $2.2B. Alphabet’s mix reduces concentration risk, while Meta’s dominance in social media advertising increases exposure to platform-specific shifts.

Strengths and Weaknesses Comparison

This table compares the Strengths and Weaknesses of Alphabet Inc. and Meta Platforms, Inc.:

Alphabet Inc. Strengths

- Highly diversified revenue streams across search, ads, cloud, and subscriptions

- Strong profitability with 28.6% net margin and 30.8% ROE

- Solid balance sheet with low debt-to-assets at 5.65%

- Global reach with substantial revenues in Americas, EMEA, and Asia Pacific

- Robust innovation in cloud and platform services

Meta Platforms Strengths

- Strong net margin at 30.08% and favorable ROE at 27.83%

- High liquidity with current ratio of 2.6

- Global presence with significant revenues in US & Canada, Asia Pacific, and Europe

- Focused product segmentation with Family of Apps generating high revenue

- Infinite interest coverage indicating strong debt servicing capacity

Alphabet Inc. Weaknesses

- Unfavorable price-to-book ratio at 7.17 may signal overvaluation

- Neutral asset turnover ratios suggest moderate capital efficiency

- Low dividend yield at 0.32% limits income appeal

- Slightly higher PE ratio relative to sector norms

- Concentrated revenue in Google Search & Other segment

Meta Platforms Weaknesses

- Unfavorable valuation metrics with PE at 27.52 and PB at 7.66

- Lower ROIC at 17.95% versus Alphabet’s 25.8%

- Dividend yield also low at 0.32%

- Moderate asset turnover indicates room for efficiency improvements

- Revenue heavily reliant on Family of Apps with limited diversification

Alphabet leads with broader diversification and stronger capital efficiency, while Meta excels in liquidity and profitability. Both face valuation concerns and limited dividend yields, impacting income-focused investors. These factors shape their strategic positioning in a competitive market.

The Moat Duel: Analyzing Competitive Defensibility

A durable structural moat protects long-term profits from relentless competition and market shifts. Here’s how Alphabet and Meta stand:

Alphabet Inc.: Dominant Network Effects & Intangible Assets

Alphabet thrives on unparalleled network effects from Google’s search dominance and YouTube’s vast user base. Its high ROIC (17% above WACC) confirms efficient capital use and margin stability. Expansion in AI and cloud services in 2026 should deepen this moat.

Meta Platforms, Inc.: Ecosystem Lock-In via Social Networks

Meta’s competitive edge stems from its vast social ecosystem—Facebook, Instagram, WhatsApp—that lock users in. Despite positive ROIC, a declining trend signals margin pressure. Its Reality Labs segment offers growth potential, but rising costs challenge moat durability.

Moat Power Play: Network Effects vs. Ecosystem Lock-In

Alphabet boasts a wider, more durable moat with growing ROIC and diversified revenue streams. Meta creates value but faces margin erosion. Alphabet is better positioned to defend and expand its market share in 2026.

Which stock offers better returns?

The past year shows strong gains for both stocks, with Alphabet’s price rising sharply and Meta also trending upward amid active trading shifts.

Trend Comparison

Alphabet Inc. (GOOGL) posted a 150% gain over 12 months, marking a bullish trend with accelerating momentum. The stock’s price ranged from 135.41 to 338.0, with moderate volatility at a 52.03 standard deviation.

Meta Platforms, Inc. (META) gained 41.6% over the same period, also bullish with acceleration. It showed higher volatility, a standard deviation of 91.27, and price movement between 443.29 and 785.23.

Alphabet’s 12-month return notably outpaced Meta’s. Both stocks accelerated, but Alphabet delivered the highest market performance in this timeframe.

Target Prices

Analysts present a broad but optimistic target price range for Alphabet Inc. and Meta Platforms, reflecting confidence in their growth prospects.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Alphabet Inc. | 190 | 390 | 328.39 |

| Meta Platforms, Inc. | 700 | 1117 | 853 |

The consensus target for Alphabet sits slightly below its current price of 338, implying moderate upside. Meta’s target consensus far exceeds its 716.5 price, signaling stronger expected appreciation.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Here are the latest institutional grades for Alphabet Inc. and Meta Platforms, Inc.:

Alphabet Inc. Grades

This table lists recent grades from recognized institutional analysts for Alphabet Inc.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Roth Capital | Maintain | Buy | 2026-01-27 |

| Needham | Maintain | Buy | 2026-01-26 |

| Keybanc | Maintain | Overweight | 2026-01-26 |

| Stifel | Maintain | Buy | 2026-01-23 |

| UBS | Maintain | Neutral | 2026-01-20 |

| Goldman Sachs | Maintain | Buy | 2026-01-13 |

| B of A Securities | Maintain | Buy | 2026-01-13 |

| Wells Fargo | Maintain | Equal Weight | 2026-01-12 |

| Mizuho | Maintain | Outperform | 2026-01-09 |

| Cantor Fitzgerald | Upgrade | Overweight | 2026-01-08 |

Meta Platforms, Inc. Grades

Below are institutional grades for Meta Platforms, Inc. from verified sources.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Cantor Fitzgerald | Maintain | Overweight | 2024-09-30 |

| Monness, Crespi, Hardt | Maintain | Buy | 2024-09-30 |

| Baird | Maintain | Outperform | 2024-09-26 |

| JMP Securities | Maintain | Market Outperform | 2024-09-26 |

| B of A Securities | Maintain | Buy | 2024-09-26 |

| Rosenblatt | Maintain | Buy | 2024-09-26 |

| Wedbush | Maintain | Outperform | 2024-09-26 |

| JP Morgan | Maintain | Overweight | 2024-09-26 |

| Cantor Fitzgerald | Maintain | Overweight | 2024-09-23 |

| Citigroup | Maintain | Buy | 2024-09-23 |

Which company has the best grades?

Alphabet Inc. holds a slightly more recent consensus with many “Buy” and “Overweight” ratings in early 2026. Meta’s latest grades from 2024 also show strong “Buy” and “Outperform” support. Alphabet’s fresher data may offer investors more current insight.

Risks specific to each company

The following categories identify critical pressure points and systemic threats facing Alphabet Inc. and Meta Platforms, Inc. in the 2026 market environment:

1. Market & Competition

Alphabet Inc.

- Dominates global search and cloud but faces intense cloud competition from AWS and Azure.

Meta Platforms, Inc.

- Leads social networking but battles fierce rivals like TikTok and emerging AI platforms.

2. Capital Structure & Debt

Alphabet Inc.

- Maintains ultra-low debt-to-equity at 0.08, signaling strong financial stability.

Meta Platforms, Inc.

- Higher debt-to-equity at 0.39, increasing leverage risk but manageable with strong interest coverage.

3. Stock Volatility

Alphabet Inc.

- Beta of 1.086 suggests moderate volatility aligned with tech sector norms.

Meta Platforms, Inc.

- Beta of 1.287 indicates higher stock price swings, raising investor risk exposure.

4. Regulatory & Legal

Alphabet Inc.

- Endures ongoing antitrust scrutiny globally, especially in Europe and the US.

Meta Platforms, Inc.

- Faces intensified regulatory challenges over data privacy and content moderation policies.

5. Supply Chain & Operations

Alphabet Inc.

- Diverse hardware supply lines but vulnerable to semiconductor shortages.

Meta Platforms, Inc.

- Heavy reliance on hardware for VR/AR products creates operational complexity and supply risks.

6. ESG & Climate Transition

Alphabet Inc.

- Has strong renewable energy initiatives but must improve social governance metrics.

Meta Platforms, Inc.

- ESG commitments growing; however, faces reputational risk from content impact and energy use of data centers.

7. Geopolitical Exposure

Alphabet Inc.

- Significant revenue from global markets exposes it to trade tensions and regulatory fragmentation.

Meta Platforms, Inc.

- Global user base faces censorship and access restrictions, impacting growth in key regions.

Which company shows a better risk-adjusted profile?

Alphabet’s strongest risk lies in regulatory and antitrust challenges, reflecting its massive market footprint and scrutiny. Meta’s primary risk is competitive pressure and stock volatility driven by evolving social media trends and innovation demands. Alphabet’s ultra-low debt and stable beta deliver a more balanced risk-adjusted profile. Meta’s higher leverage and beta increase its vulnerability despite solid profitability. Notably, Alphabet’s Altman Z-Score of 18.8 versus Meta’s 8.8 confirms superior financial safety. This metric justifies my caution around Meta’s leverage and market sensitivity in 2026.

Final Verdict: Which stock to choose?

Alphabet Inc. demonstrates unmatched capital efficiency and a durable competitive advantage, reflected in its consistently rising ROIC. Its strong cash flow generation powers growth and innovation. A point of vigilance is its rich price-to-book ratio, which may temper upside. It suits portfolios targeting aggressive growth with a tolerance for premium valuation.

Meta Platforms, Inc. boasts a formidable strategic moat through its dominance in social networking and recurring revenue streams. It offers a safer balance sheet profile relative to Alphabet, with solid liquidity and moderate leverage. This makes it attractive for investors seeking Growth at a Reasonable Price (GARP) with exposure to digital advertising expansion.

If you prioritize robust capital returns and innovation leadership, Alphabet outshines due to its superior ROIC and cash flow quality. However, if you seek a blend of growth with relative stability and a proven network effect, Meta offers better safety and resilience despite a declining ROIC trend. Both present compelling but distinct analytical scenarios depending on your risk appetite.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Alphabet Inc. and Meta Platforms, Inc. to enhance your investment decisions: