Home > Comparison > Technology > AMD vs SWKS

The strategic rivalry between Advanced Micro Devices, Inc. (AMD) and Skyworks Solutions, Inc. shapes the semiconductor sector’s evolution. AMD operates as a diversified semiconductor powerhouse with a focus on high-performance computing and graphics. Skyworks, by contrast, specializes in analog and mixed-signal semiconductors serving wireless and connectivity markets. This analysis pits AMD’s growth-oriented model against Skyworks’ niche expertise to identify which offers a superior risk-adjusted profile for diversified investors.

Table of contents

Companies Overview

Advanced Micro Devices and Skyworks Solutions shape critical facets of the semiconductor industry, influencing computing and wireless communications.

Advanced Micro Devices, Inc.: Computing and Graphics Powerhouse

Advanced Micro Devices dominates as a semiconductor innovator specializing in x86 microprocessors, GPUs, and server processors. Its core revenue stems from Computing and Graphics and Enterprise segments, powering desktops, notebooks, and data centers. In 2026, AMD focuses strategically on expanding its high-performance computing portfolio and semi-custom SoCs for gaming consoles, striving to outpace competitors with cutting-edge technology.

Skyworks Solutions, Inc.: Wireless Semiconductor Specialist

Skyworks Solutions leads in proprietary semiconductor components for wireless connectivity. It generates revenue through amplifiers, filters, front-end modules, and analog system-on-chip products, serving diverse markets from smartphones to automotive systems. In 2026, Skyworks centers its strategy on broadening its product portfolio for 5G infrastructure and connected devices, aiming to capitalize on the expanding wireless ecosystem.

Strategic Collision: Similarities & Divergences

Both companies thrive in semiconductors but diverge in approach: AMD pushes a computing-centric, integrated platform model, while Skyworks embraces a component-level, wireless connectivity focus. Their primary battleground lies in mobile and data infrastructure, where high performance meets seamless connectivity. Investors face distinct profiles: AMD offers high-growth exposure to CPUs and GPUs, whereas Skyworks provides steadier returns tied to wireless hardware evolution.

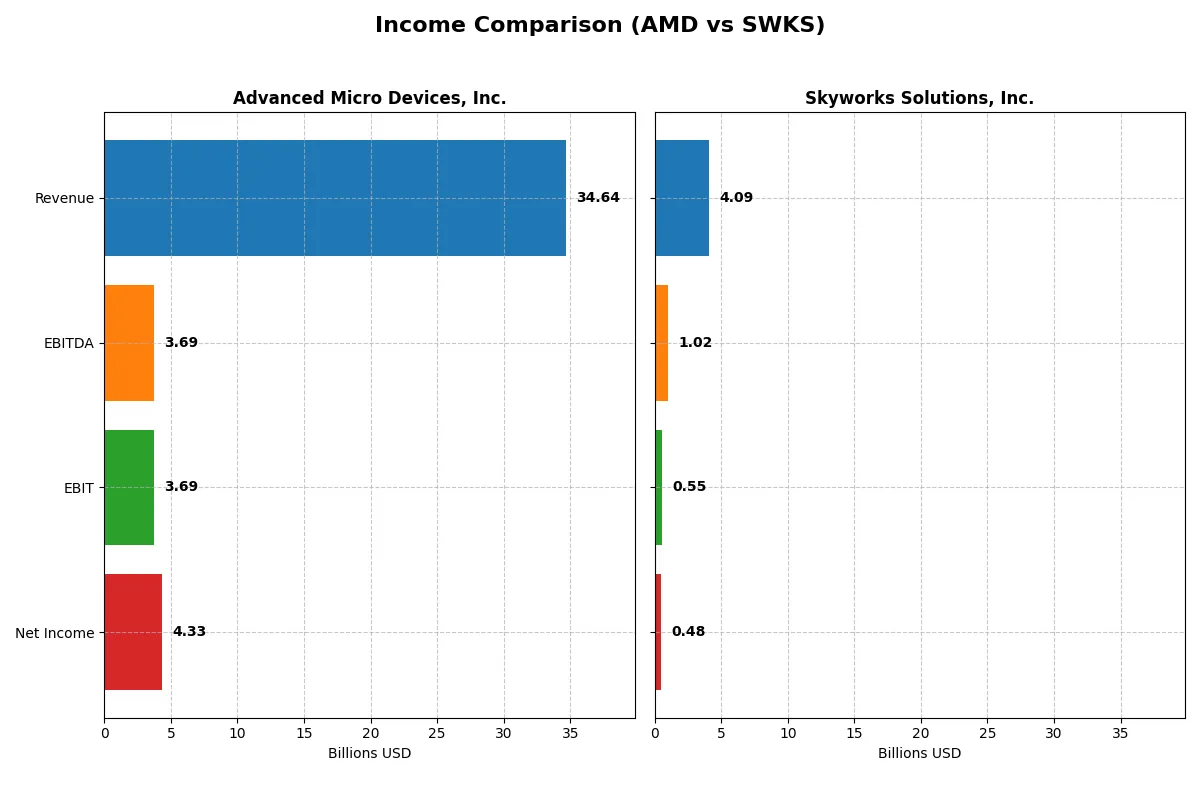

Income Statement Comparison

This table dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Advanced Micro Devices, Inc. (AMD) | Skyworks Solutions, Inc. (SWKS) |

|---|---|---|

| Revenue | 34.6B | 4.1B |

| Cost of Revenue | 17.5B | 2.4B |

| Operating Expenses | 13.5B | 1.2B |

| Gross Profit | 17.2B | 1.7B |

| EBITDA | 3.7B | 1.0B |

| EBIT | 3.7B | 554M |

| Interest Expense | 131M | 27M |

| Net Income | 4.3B | 477M |

| EPS | 2.67 | 3.09 |

| Fiscal Year | 2025 | 2025 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals which company leverages its revenue and costs most efficiently to generate shareholder value.

Advanced Micro Devices, Inc. Analysis

AMD’s revenue surged to $34.6B in 2025, up 34% year-over-year, with net income climbing sharply to $4.3B. The company maintains a robust gross margin of 49.5% and a healthy net margin of 12.5%, signaling strong operational discipline. Momentum accelerated in 2025, driven by substantial EBIT growth of 77.5%, showcasing improved profitability and cost management.

Skyworks Solutions, Inc. Analysis

Skyworks generated $4.1B in revenue for 2025, marking a 2.2% decline from the previous year. Net income fell to $477M, reflecting margin pressure with a gross margin of 41.2% and net margin at 11.7%. EBIT contracted nearly 17%, indicating weakened operational efficiency and declining profitability momentum compared to prior years.

Margin Strength vs. Revenue Growth

AMD decisively outperforms Skyworks in revenue expansion and net income growth, demonstrating superior margin management and operational leverage. Skyworks’ shrinking top line and falling profitability highlight structural challenges. For investors, AMD’s profile offers a compelling mix of revenue scale and margin improvement, while Skyworks shows signs of stagnation.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | Advanced Micro Devices, Inc. (AMD) | Skyworks Solutions, Inc. (SWKS) |

|---|---|---|

| ROE | 2.85% (2024) | 8.29% (2025) |

| ROIC | 2.49% (2024) | 6.35% (2025) |

| P/E | 124 (2024) | 25 (2025) |

| P/B | 3.52 (2024) | 2.07 (2025) |

| Current Ratio | 2.62 (2024) | 2.33 (2025) |

| Quick Ratio | 1.83 (2024) | 1.76 (2025) |

| D/E | 0.04 (2024) | 0.21 (2025) |

| Debt-to-Assets | 3.20% (2024) | 15.20% (2025) |

| Interest Coverage | 20.7 (2024) | 18.5 (2025) |

| Asset Turnover | 0.37 (2024) | 0.52 (2025) |

| Fixed Asset Turnover | 10.63 (2024) | 2.95 (2025) |

| Payout ratio | 0% (2024) | 90.7% (2025) |

| Dividend yield | 0% (2024) | 3.63% (2025) |

| Fiscal Year | 2024 | 2025 |

Efficiency & Valuation Duel: The Vital Signs

Ratios act as a company’s DNA, revealing hidden risks and operational excellence that shape investment outcomes.

Advanced Micro Devices, Inc.

AMD shows a favorable net margin of 12.51% but suffers from zero return on equity and invested capital. Its P/E ratio at 80.54 signals an expensive stock. The company does not pay dividends, focusing on heavy R&D reinvestment, indicating a growth-driven shareholder return strategy.

Skyworks Solutions, Inc.

Skyworks posts an 11.67% net margin with an 8.29% return on equity, reflecting moderate profitability. Its P/E of 24.95 suggests a fairly valued stock. The 3.63% dividend yield complements solid cash flow, providing balanced shareholder returns through income and operational efficiency.

Premium Valuation vs. Balanced Profitability

AMD’s stretched valuation and lack of returns highlight risk despite strong margins and growth focus. Skyworks offers better risk-reward balance with stable profitability and dividends. Growth investors may prefer AMD’s profile, while income-focused investors might favor Skyworks.

Which one offers the Superior Shareholder Reward?

I see Skyworks (SWKS) offers a more balanced and sustainable shareholder reward in 2026. Skyworks pays a solid 3.63% dividend yield with a 91% payout ratio, supported by strong free cash flow (7.16B per share) coverage. Its share buybacks are steady, complementing dividends for total return. AMD (Advanced Micro Devices) pays no dividend and reinvests heavily into growth, reflected in its high P/E (80.5) and price-to-FCF (63.3) ratios. AMD’s buybacks are less emphasized, raising questions on near-term shareholder cash returns. For investors prioritizing income and capital return, SWKS’s disciplined distribution beats AMD’s growth-only approach.

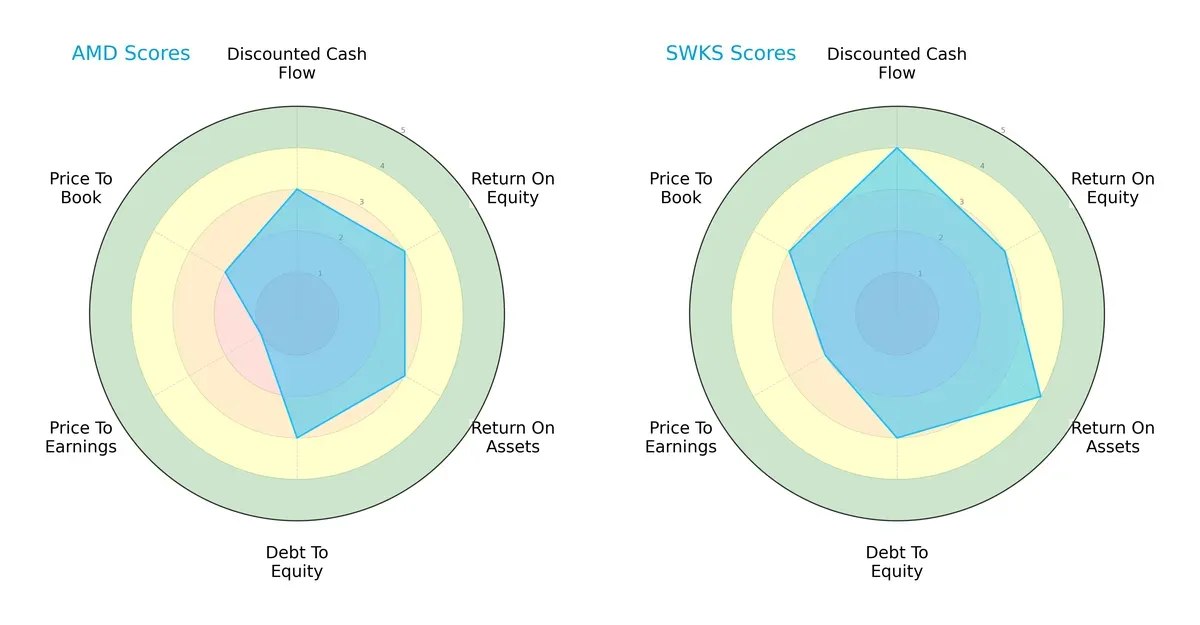

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Advanced Micro Devices, Inc. and Skyworks Solutions, Inc., highlighting their financial strengths and valuation contrasts:

Skyworks edges AMD in discounted cash flow and return on assets, reflecting superior asset utilization and cash flow projections. Both firms show balanced return on equity and debt-to-equity scores, indicating comparable capital efficiency and leverage management. However, AMD’s valuation scores (P/E and P/B) lag significantly, suggesting market skepticism or overvaluation risks. Overall, Skyworks presents a more balanced financial profile, while AMD relies more heavily on operational metrics despite valuation concerns.

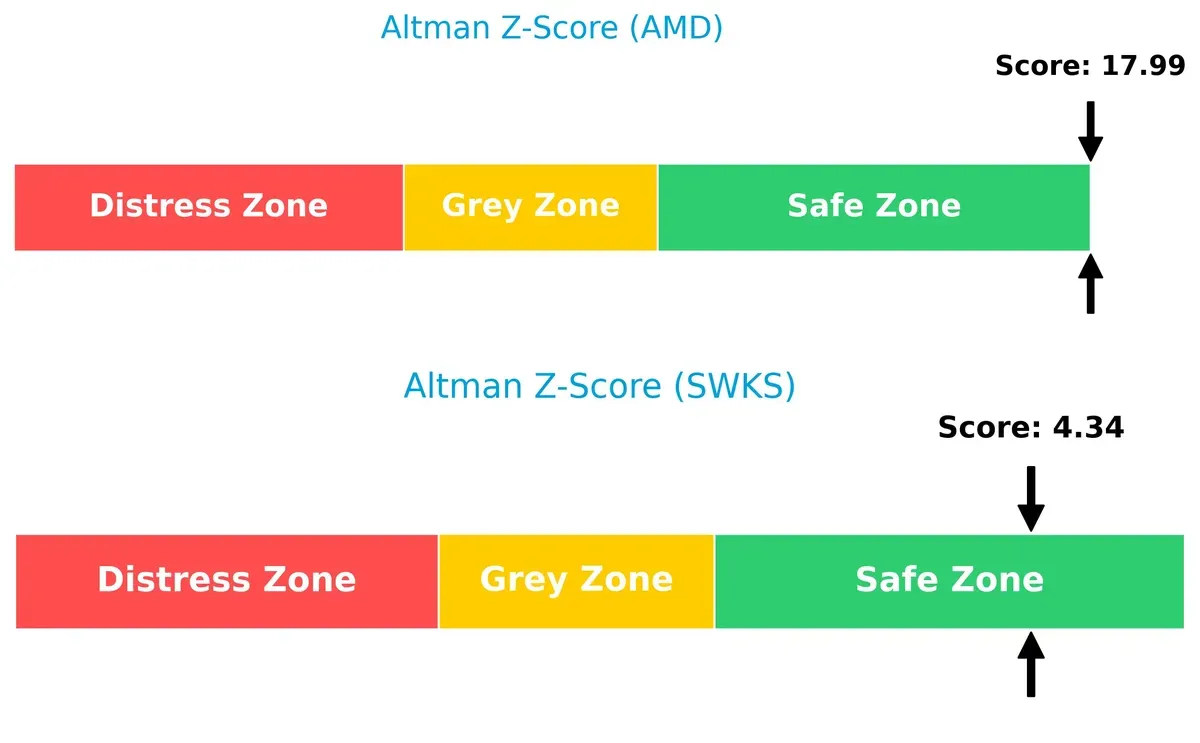

Bankruptcy Risk: Solvency Showdown

The Altman Z-Score difference strongly favors AMD, with both companies comfortably in the safe zone:

AMD’s exceptionally high Z-Score near 18 signals robust financial stability and minimal bankruptcy risk. Skyworks, with a score above 4, also maintains solid solvency but with less margin. In this cycle, AMD’s balance sheet strength provides a clear survival advantage, underscoring prudent capital allocation and risk management.

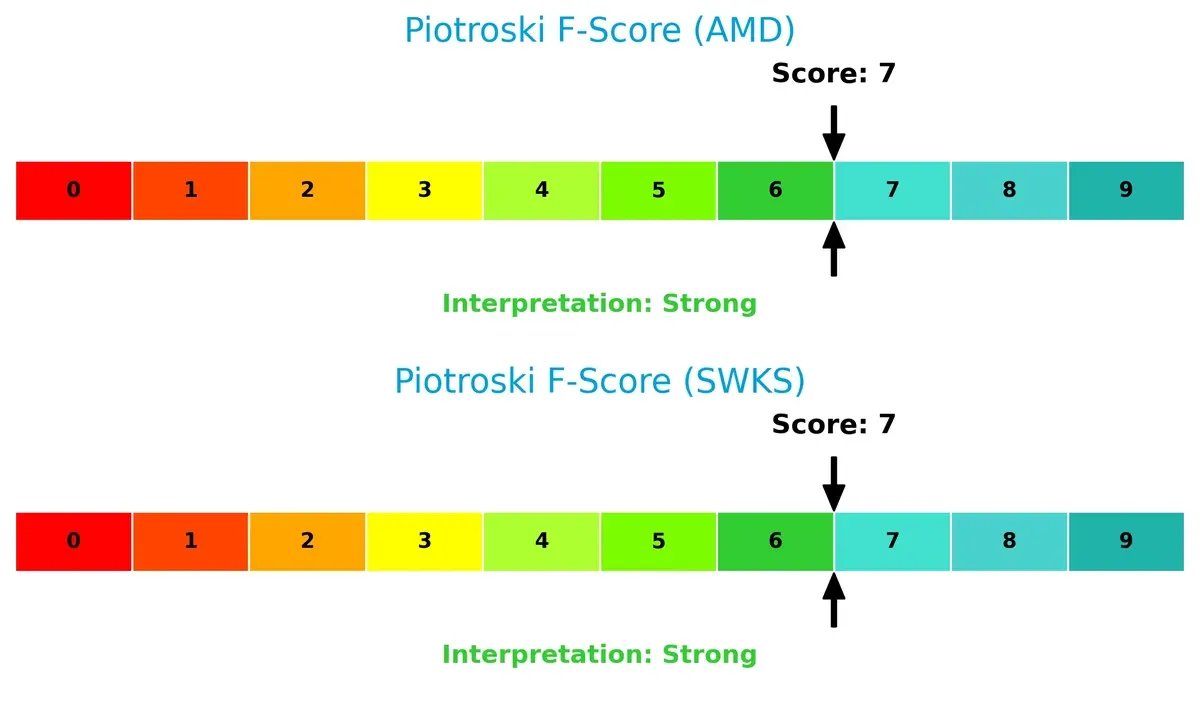

Financial Health: Quality of Operations

Both firms score 7 on the Piotroski F-Score, reflecting strong operational quality and financial health:

This parity suggests that both companies maintain sound internal metrics across profitability, leverage, and liquidity. Neither shows red flags in their financial operations, positioning them well for sustainable performance. Investors can regard both as fundamentally solid with effective management of financial risks.

How are the two companies positioned?

This section dissects the operational DNA of AMD and SWKS by comparing their revenue distribution and internal dynamics. The goal is to confront their economic moats to identify which model offers the most resilient and sustainable competitive advantage today.

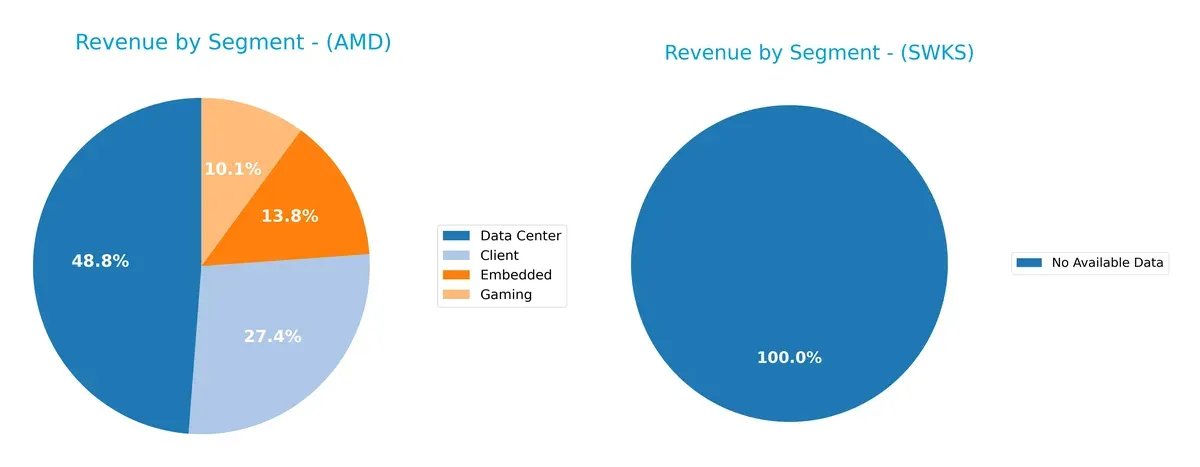

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how Advanced Micro Devices, Inc. and Skyworks Solutions, Inc. diversify their income streams and where their primary sector bets lie:

AMD reveals a diversified portfolio with a heavy tilt toward Data Center at $12.6B in 2024, dwarfing Gaming at $2.6B and Embedded at $3.6B. This mix anchors AMD’s ecosystem lock-in in cloud infrastructure and high-performance computing. Skyworks lacks available segment data, limiting direct comparison. AMD’s strategy shows less concentration risk, balancing fast-growing data centers with steady client and embedded revenues.

Strengths and Weaknesses Comparison

This table compares the strengths and weaknesses of AMD and SWKS based on diversification, profitability, financials, innovation, global presence, and market share:

AMD Strengths

- Diversified revenue streams across Client, Data Center, Embedded, and Gaming segments

- Strong net margin at 12.51%

- Favorable debt metrics and high interest coverage ratio

- Significant global presence with large sales in the US and China

SWKS Strengths

- Favorable net margin at 11.67%

- Healthy liquidity ratios: current ratio 2.33 and quick ratio 1.76

- Moderate leverage with favorable debt-to-assets and interest coverage

- Global presence with dominant US sales and diversified Asia exposure

AMD Weaknesses

- Zero ROE and ROIC indicating poor capital returns

- WACC higher than ROIC, signaling value destruction

- Unfavorable liquidity ratios (current and quick ratios)

- High P/E ratio at 80.54, implying expensive valuation

- Low asset turnover ratios

SWKS Weaknesses

- ROE below industry average at 8.29%

- Neutral ROIC and WACC suggest average capital efficiency

- Moderate P/E ratio at 24.95 limits growth upside

- No significant product diversification disclosed

- Geographic revenue more concentrated in US

Overall, AMD shows broad product diversification and strong margin with sound debt management but struggles with capital efficiency and liquidity. SWKS presents a more balanced financial profile with solid liquidity and moderate profitability but less product diversification and a more concentrated geographic footprint. These factors shape each firm’s strategic focus on operational efficiency versus market expansion.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only true defense against profit erosion in competitive markets. It ensures sustainable long-term profitability through:

Advanced Micro Devices, Inc. (AMD): Innovation-Driven Technology Moat

AMD’s primary moat lies in its cutting-edge chip design and semi-custom SoC products, driving strong revenue growth and margin stability. However, its declining ROIC trend signals challenges sustaining this advantage in 2026 amid fierce industry competition.

Skyworks Solutions, Inc. (SWKS): Niche Component Supplier Moat

SWKS relies on specialized analog semiconductor products, contrasting AMD’s broader market reach. Despite steady margins, its shrinking revenue and negative ROIC spread highlight weakening competitive positioning and pressure on future profitability.

Innovation Scale vs. Specialized Component Focus

Both firms show very unfavorable ROIC trends, but AMD’s expansive product ecosystem offers a wider moat. AMD is better positioned to defend market share, provided it reverses its profitability decline.

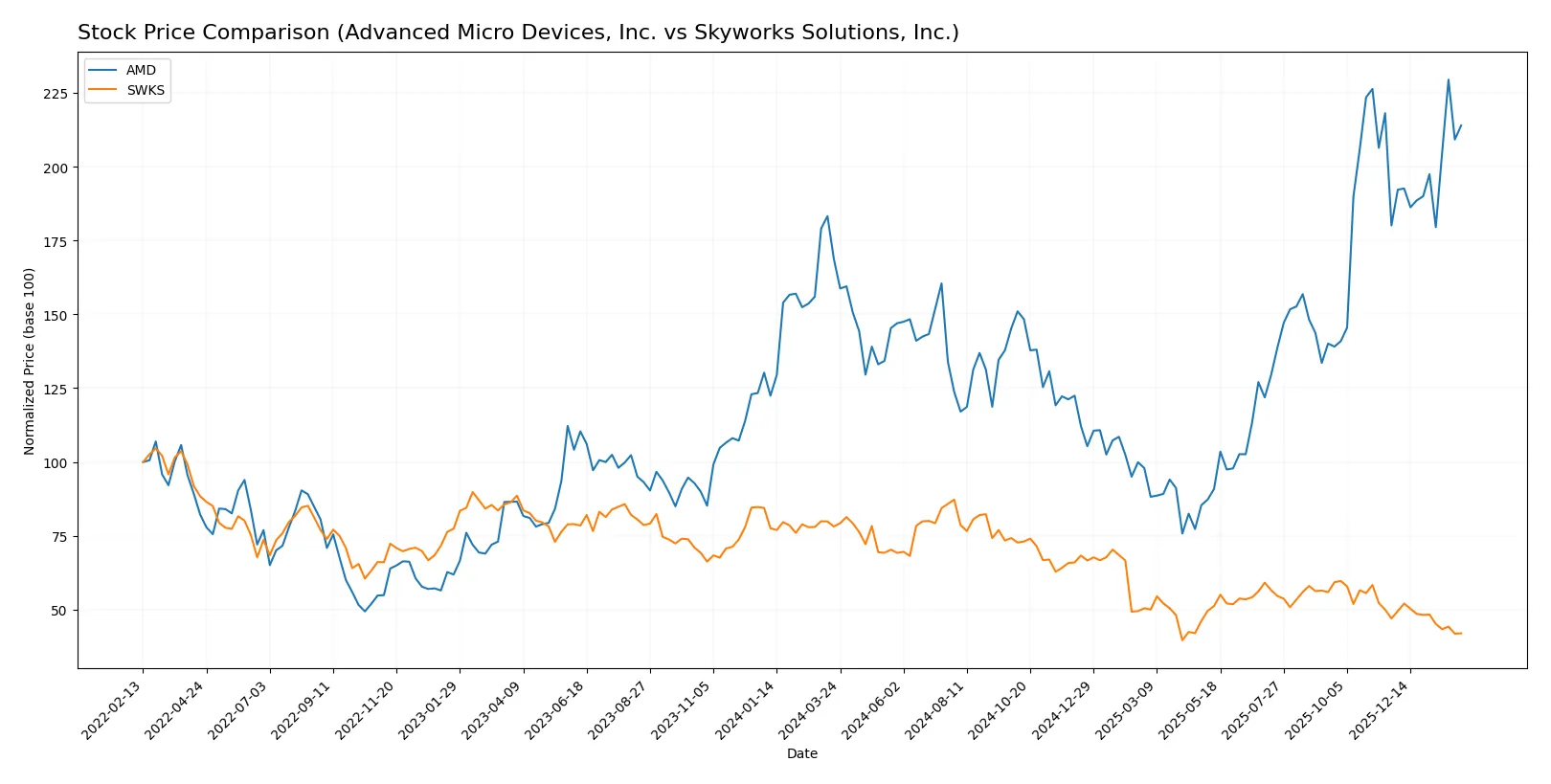

Which stock offers better returns?

The past year saw contrasting price dynamics between Advanced Micro Devices, Inc. and Skyworks Solutions, Inc., with AMD gaining significant ground while SWKS declined sharply.

Trend Comparison

Advanced Micro Devices, Inc. shows a strong bullish trend over the last 12 months, with a 26.72% price increase and accelerating momentum. The stock ranged from 85.76 to 259.68.

Skyworks Solutions, Inc. exhibits a bearish trend with a 46.26% price decline and deceleration. The stock’s price fluctuated between 52.78 and 116.18 during the same period.

AMD delivered the highest market performance, outperforming SWKS by over 70 percentage points with a clear upward trajectory versus SWKS’s persistent downward trend.

Target Prices

Analysts present a mixed but generally optimistic target consensus for these semiconductor companies.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Advanced Micro Devices, Inc. | 225 | 380 | 291.56 |

| Skyworks Solutions, Inc. | 60 | 140 | 78.8 |

The consensus target for AMD sits about 20% above its current price of $242, signaling bullish analyst expectations. Skyworks’ consensus target of $78.8 exceeds its $55.93 market price by over 40%, indicating room for upside despite recent weakness.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

The following tables summarize recent institutional grades for Advanced Micro Devices, Inc. and Skyworks Solutions, Inc.:

Advanced Micro Devices, Inc. Grades

Here are the latest grades from reputable institutions for AMD:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Wells Fargo | Maintain | Overweight | 2026-01-30 |

| Piper Sandler | Maintain | Overweight | 2026-01-26 |

| UBS | Maintain | Buy | 2026-01-26 |

| Bernstein | Maintain | Market Perform | 2026-01-21 |

| Keybanc | Upgrade | Overweight | 2026-01-13 |

| Truist Securities | Maintain | Buy | 2025-12-19 |

| Cantor Fitzgerald | Maintain | Overweight | 2025-12-16 |

| Morgan Stanley | Maintain | Equal Weight | 2025-11-12 |

| Wedbush | Maintain | Outperform | 2025-11-12 |

| Rosenblatt | Maintain | Buy | 2025-11-12 |

Skyworks Solutions, Inc. Grades

Here are the latest grades from reputable institutions for SWKS:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Morgan Stanley | Maintain | Equal Weight | 2026-02-02 |

| Mizuho | Maintain | Neutral | 2026-01-26 |

| B. Riley Securities | Maintain | Neutral | 2026-01-26 |

| Susquehanna | Maintain | Neutral | 2026-01-22 |

| UBS | Maintain | Neutral | 2026-01-20 |

| Mizuho | Upgrade | Neutral | 2025-11-11 |

| JP Morgan | Maintain | Neutral | 2025-11-05 |

| UBS | Maintain | Neutral | 2025-11-05 |

| UBS | Maintain | Neutral | 2025-10-29 |

| Piper Sandler | Upgrade | Overweight | 2025-10-29 |

Which company has the best grades?

AMD consistently receives higher grades such as Buy and Overweight from several top institutions. SWKS mostly holds Neutral or Equal Weight ratings with fewer upgrades. This suggests AMD is viewed as having stronger growth or value potential by analysts, which may influence investor confidence.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

Advanced Micro Devices, Inc.

- Faces intense competition from larger players like Intel and Nvidia, pressuring margins and market share.

Skyworks Solutions, Inc.

- Competes in niche analog and mixed-signal semiconductors, with steady demand but exposure to smartphone market cycles.

2. Capital Structure & Debt

Advanced Micro Devices, Inc.

- Maintains a favorable debt-to-equity profile with strong interest coverage, limiting financial risk.

Skyworks Solutions, Inc.

- Leverages moderate debt with favorable ratios, supporting stable operations and flexibility.

3. Stock Volatility

Advanced Micro Devices, Inc.

- Exhibits high beta (1.95), indicating above-market volatility and sensitivity to tech sector swings.

Skyworks Solutions, Inc.

- Shows moderate beta (1.32), reflecting lower volatility and steadier price movements.

4. Regulatory & Legal

Advanced Micro Devices, Inc.

- Faces regulatory scrutiny related to global trade tensions and intellectual property challenges.

Skyworks Solutions, Inc.

- Navigates regulatory risks tied to export controls and supply chain compliance in multiple jurisdictions.

5. Supply Chain & Operations

Advanced Micro Devices, Inc.

- Vulnerable to semiconductor supply constraints and geopolitical disruptions impacting manufacturing.

Skyworks Solutions, Inc.

- Exposed to component shortages and supplier concentration risks but benefits from diversified product lines.

6. ESG & Climate Transition

Advanced Micro Devices, Inc.

- Invests in sustainability initiatives but faces pressure to reduce carbon footprint across complex supply chains.

Skyworks Solutions, Inc.

- Advances ESG efforts with energy-efficient products but must address emissions from manufacturing processes.

7. Geopolitical Exposure

Advanced Micro Devices, Inc.

- Significant exposure to US-China tensions affecting production and sales in Asia-Pacific markets.

Skyworks Solutions, Inc.

- Moderately exposed to geopolitical risks, with diversified global sales mitigating some impact.

Which company shows a better risk-adjusted profile?

Skyworks Solutions faces fewer systemic risks and demonstrates a stronger risk-adjusted profile than Advanced Micro Devices. AMD’s highest risk lies in volatile market competition and aggressive valuation, while Skyworks benefits from stable financials and lower stock volatility. Notably, AMD’s elevated beta of 1.95 signals sharp price swings, amplifying risk in turbulent markets.

Final Verdict: Which stock to choose?

Advanced Micro Devices, Inc. (AMD) excels through its unmatched ability to drive revenue and earnings growth in a highly competitive semiconductor landscape. Its superpower lies in innovation-driven expansion, though investors should watch its declining capital efficiency carefully. AMD suits aggressive growth portfolios willing to tolerate volatility for outsized returns.

Skyworks Solutions, Inc. (SWKS) offers a strategic moat with steady recurring revenue and solid free cash flow generation, reflecting operational resilience. It presents a more conservative profile than AMD, with a favorable balance sheet and dividend yield. SWKS fits well in GARP portfolios seeking reasonable growth blended with income and stability.

If you prioritize rapid growth and market share expansion, AMD outshines with its innovation engine and bullish momentum despite risks in profitability metrics. However, if you seek better stability and income with a moderate valuation, SWKS offers a safer harbor amid market turbulence. Both stocks face challenges in sustaining long-term value creation, urging cautious allocation aligned with investor risk tolerance.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Advanced Micro Devices, Inc. and Skyworks Solutions, Inc. to enhance your investment decisions: