Home > Comparison > Technology > ACN vs GLOB

The strategic rivalry between Accenture plc and Globant S.A. defines the current trajectory of the global technology services sector. Accenture operates as a capital-intensive industrial giant offering comprehensive consulting and digital transformation services. In contrast, Globant is a nimble, high-growth technology innovator specializing in digital product development and agile delivery. This analysis will clarify which corporate strategy delivers superior risk-adjusted returns for a diversified portfolio amid evolving market demands.

Table of contents

Companies Overview

Accenture and Globant stand as pivotal players in the global technology services sector, shaping digital transformation trends.

Accenture plc: Global Professional Services Powerhouse

Accenture dominates as a professional services titan, generating revenue through consulting, technology, and operations services worldwide. Its 2026 strategy emphasizes digital transformation, intelligent automation, and cloud infrastructure, leveraging a vast workforce of 801K employees. The company’s broad service portfolio, including cybersecurity and AI, underpins its robust market position and client retention.

Globant S.A.: Innovation-Driven Digital Services

Globant operates as a dynamic technology services provider focused on digital reinvention and agile delivery. It drives revenue through specialized services like cloud transformation, AI, blockchain, and digital experience platforms. In 2026, Globant concentrates on expanding its offerings in metaverse, sustainable business solutions, and precision medicine, supported by a leaner team of 31K employees and a strong emphasis on innovation.

Strategic Collision: Similarities & Divergences

Accenture and Globant share a commitment to digital transformation but differ in scale and approach. Accenture’s strategy favors a comprehensive, integrated ecosystem, while Globant pursues niche, innovation-led solutions. Their primary battleground lies in cloud services and AI-driven business reinvention. Investors face contrasting profiles: Accenture offers scale and stability, Globant emphasizes growth potential through specialized digital innovation.

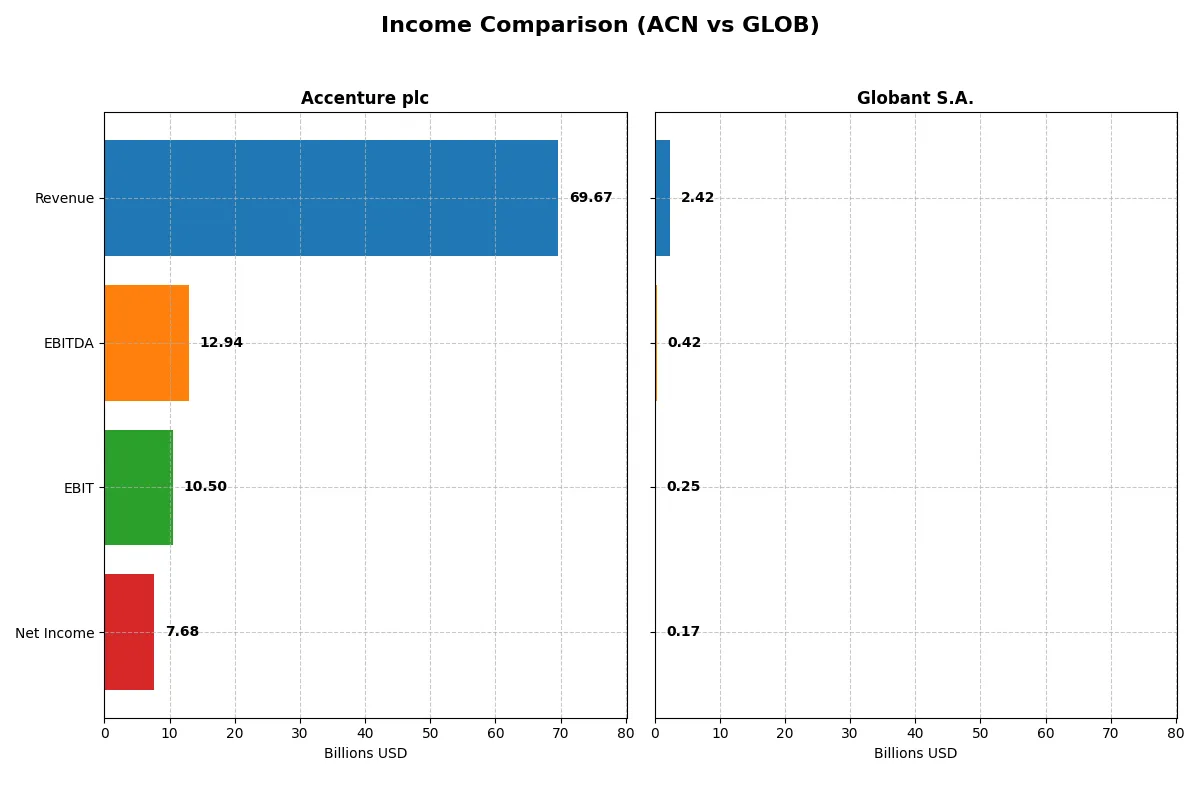

Income Statement Comparison

The following data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Accenture plc (ACN) | Globant S.A. (GLOB) |

|---|---|---|

| Revenue | 69.7B | 2.42B |

| Cost of Revenue | 47.4B | 1.55B |

| Operating Expenses | 12.0B | 638M |

| Gross Profit | 22.2B | 863M |

| EBITDA | 12.9B | 417M |

| EBIT | 10.5B | 254M |

| Interest Expense | 229M | 29M |

| Net Income | 7.68B | 166M |

| EPS | 12.29 | 3.82 |

| Fiscal Year | 2025 | 2024 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison unveils the true efficiency and profitability of each company’s core business engine over recent years.

Accenture plc Analysis

Accenture’s revenue climbs steadily from 50.5B in 2021 to nearly 70B in 2025, reflecting solid growth momentum. Net income rises from 5.9B to 7.7B, though net margin slightly contracts to 11.0%. Gross margin holds firm near 32%, while EBIT margin remains strong at 15%. Efficiency gains manifest in a favorable 7.6% EBIT growth year-over-year, underscoring disciplined cost control and robust operating leverage.

Globant S.A. Analysis

Globant expands revenues sharply from 814M in 2020 to 2.4B in 2024, nearly tripling top-line scale. Net income follows suit, surging from 54M to 166M, with a modest net margin of 6.9%. Gross margin peaks at 35.7%, evidencing strong product pricing power. EBIT margin at 10.5% supports healthy operating profitability. Despite a recent 9.3% dip in net margin, overall revenue and net income growth rates exceed 15%, signaling high operational momentum.

Scale and Margin: Steady Growth vs. Rapid Expansion

Accenture delivers consistent margin strength with steady revenue and net income growth, exemplifying efficiency and scale. Globant impresses with rapid top-line expansion and accelerating net income, though with thinner margins. The clear fundamental winner in absolute profitability is Accenture, thanks to its larger scale and superior margins. Investors favoring stability and margin resilience will find Accenture’s profile more attractive, while those seeking high growth might lean towards Globant’s dynamic trajectory.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies analyzed:

| Ratios | Accenture plc (ACN) | Globant S.A. (GLOB) |

|---|---|---|

| ROE | 24.6% | 8.4% |

| ROIC | 17.0% | 6.8% |

| P/E | 21.2 | 57.6 |

| P/B | 5.21 | 4.86 |

| Current Ratio | 1.42 | 1.54 |

| Quick Ratio | 1.42 | 1.54 |

| D/E | 0.26 | 0.21 |

| Debt-to-Assets | 12.5% | 13.0% |

| Interest Coverage | 44.7 | 7.87 |

| Asset Turnover | 1.07 | 0.76 |

| Fixed Asset Turnover | 16.18 | 8.70 |

| Payout Ratio | 48.2% | 0% |

| Dividend Yield | 2.28% | 0% |

| Fiscal Year | 2025 | 2024 |

Efficiency & Valuation Duel: The Vital Signs

Ratios serve as a company’s DNA, unveiling hidden risks and highlighting operational excellence beyond surface-level metrics.

Accenture plc

Accenture delivers strong profitability with a 24.6% ROE and a solid 11% net margin, signaling efficient operations. Its P/E of 21.2 suggests a fairly valued stock, while a high P/B at 5.2 raises caution. The company rewards shareholders with a 2.3% dividend, reflecting balanced capital allocation.

Globant S.A.

Globant’s profitability lags with an 8.4% ROE and a moderate 6.9% net margin, indicating operational challenges. The stock trades at a steep P/E of 57.6, signaling expensive valuation. It lacks dividends, reinvesting capital for growth, but carries elevated valuation risks amid moderate operational efficiency.

Premium Valuation vs. Operational Safety

Accenture offers a better balance of profitability and valuation discipline with consistent shareholder returns. Globant’s high valuation and lower returns imply higher risk. Investors seeking stability may favor Accenture’s profile, while those targeting growth face greater risk with Globant.

Which one offers the Superior Shareholder Reward?

I compare Accenture plc (ACN) and Globant S.A. (GLOB) on shareholder rewards through dividends and buybacks. ACN yields 2.28% with a sustainable payout ratio near 48%. It supports this with strong free cash flow coverage (~95%) and consistent buybacks adding to total returns. GLOB pays no dividend, reinvesting heavily in growth and capex, limiting free cash flow conversion (~89%) and buyback scale. While GLOB targets expansion, ACN’s balanced distribution model offers a more reliable and attractive total return profile in 2026, blending income and capital appreciation. I favor ACN for superior shareholder reward sustainability.

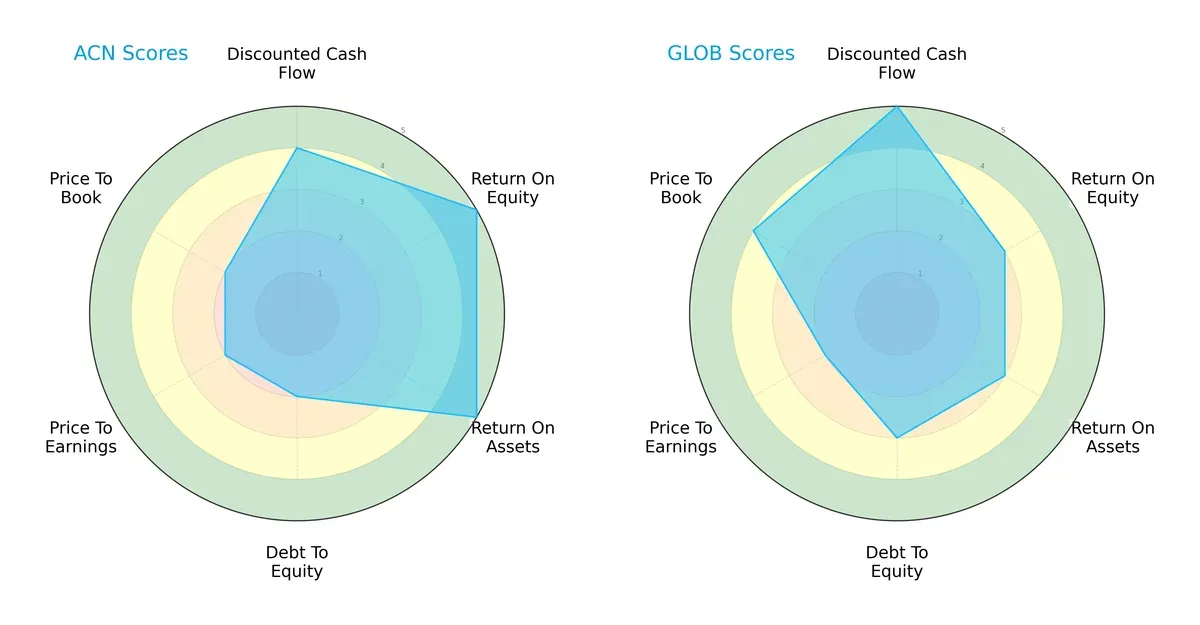

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and strategic trade-offs of Accenture plc and Globant S.A., highlighting their financial strengths and valuation nuances:

Accenture shows superior efficiency with top ROE and ROA scores (5 each), but weaker valuation scores (PE and PB at 2). Globant excels in discounted cash flow (5) and price-to-book (4), indicating better perceived value. Accenture’s debt management lags (score 2) compared to Globant’s moderate 3. Overall, Accenture delivers a more balanced operational profile; Globant leans on valuation and cash flow advantages.

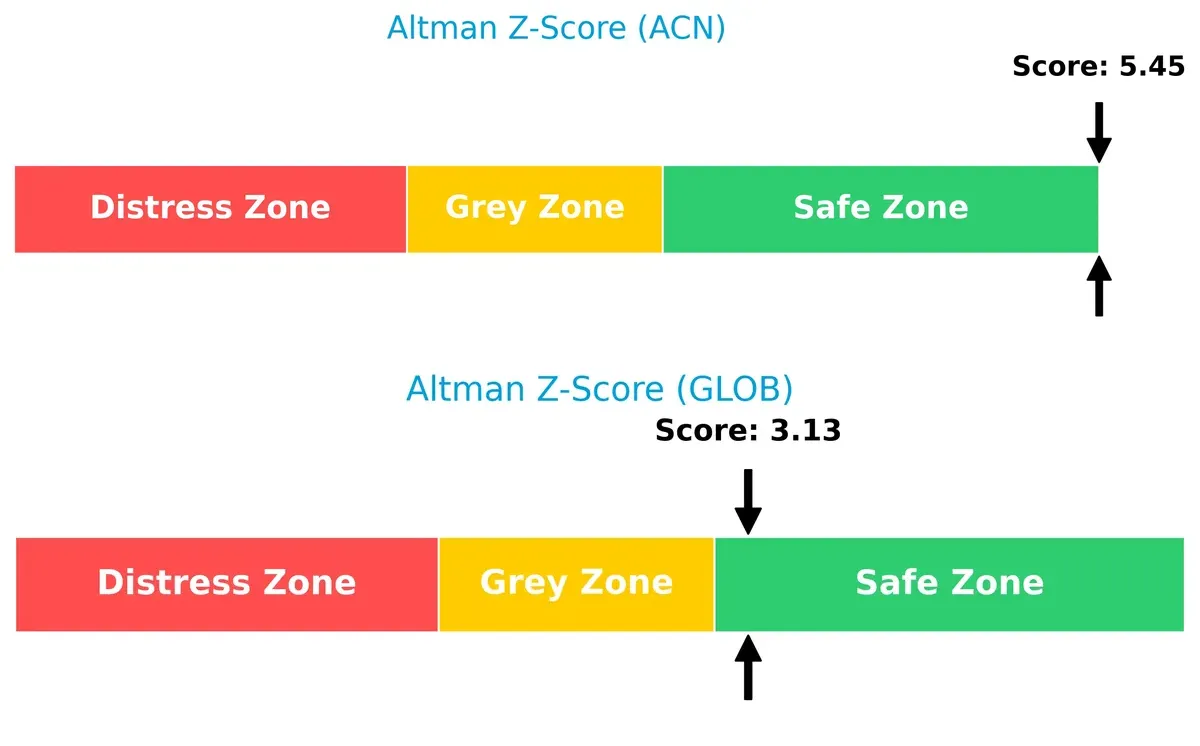

Bankruptcy Risk: Solvency Showdown

Accenture’s Altman Z-Score of 5.45 far exceeds Globant’s 3.13, both safely above the distress threshold, signaling robust solvency but greater cushioning for Accenture in volatile cycles:

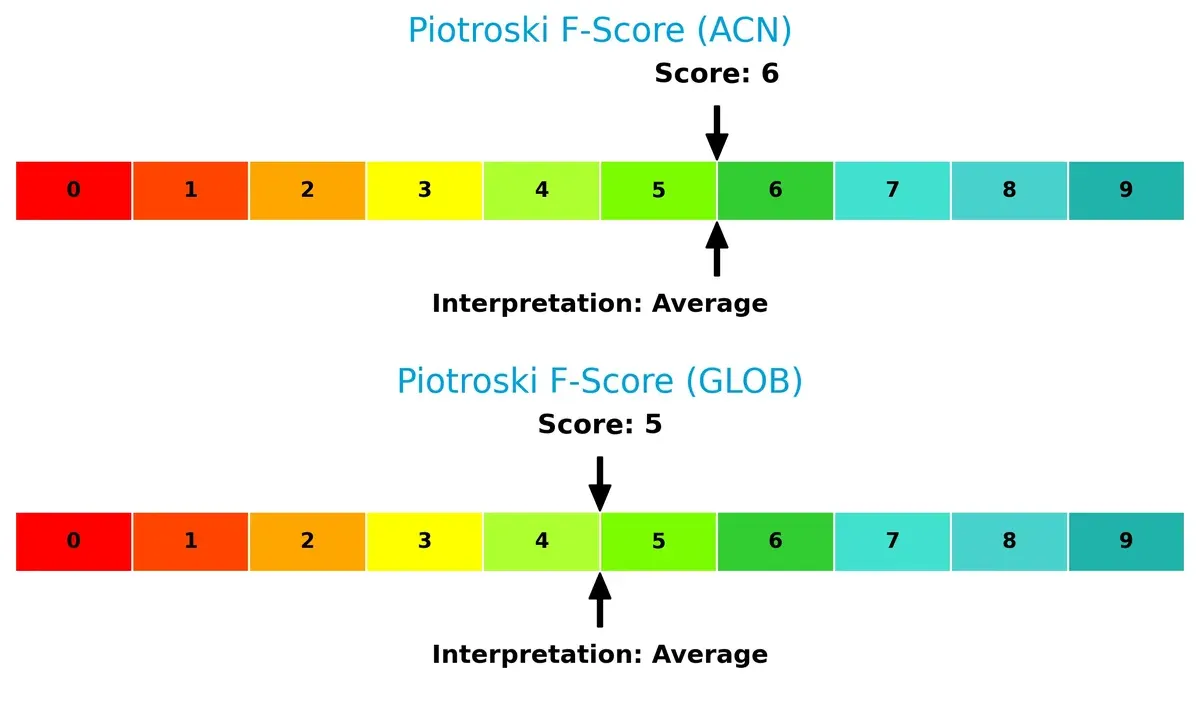

Financial Health: Quality of Operations

Both firms score in the “average” range on the Piotroski F-Score, with Accenture at 6 and Globant at 5, indicating decent but not peak internal financial health. Neither shows immediate red flags, yet Accenture edges ahead slightly:

How are the two companies positioned?

This section dissects the operational DNA of Accenture and Globant by comparing their revenue distribution and internal dynamics. The goal is to confront their economic moats and identify which model delivers the most resilient, sustainable competitive advantage today.

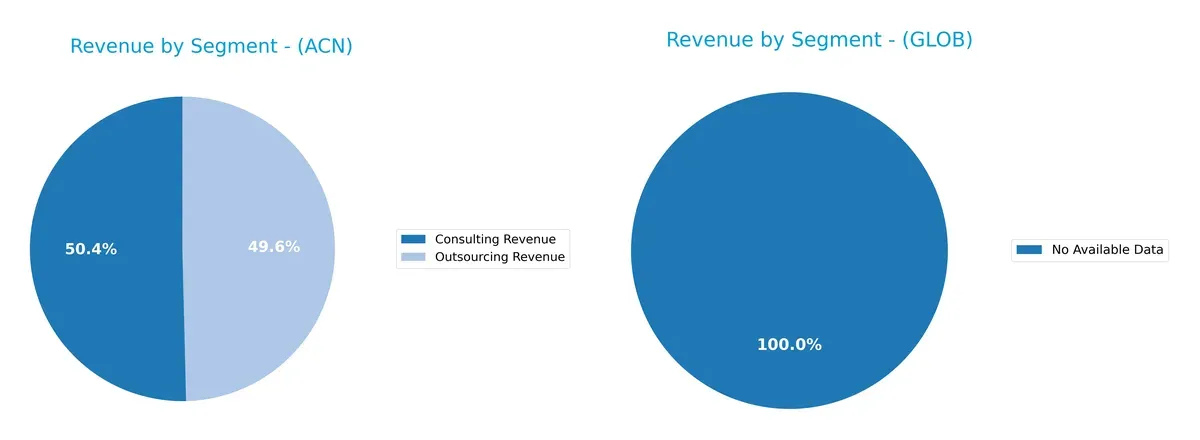

Revenue Segmentation: The Strategic Mix

This comparison dissects how Accenture plc and Globant S.A. diversify their income streams and where their primary sector bets lie:

Accenture anchors its revenue in two massive segments: Consulting at $35.1B and Outsourcing at $34.6B, showing a clear dual focus. In contrast, Globant lacks available segment data, preventing a direct comparison. Accenture’s balanced mix between consulting and outsourcing reduces concentration risk and builds a strong ecosystem lock-in, leveraging infrastructure dominance across industries. This dual strategy enhances resilience through diversified client engagements and service offerings.

Strengths and Weaknesses Comparison

This table compares the Strengths and Weaknesses of Accenture plc and Globant S.A.:

Accenture plc Strengths

- High profitability with 11.02% net margin and 24.61% ROE

- Strong capital allocation, ROIC 16.99% above WACC 9.37%

- Favorable leverage metrics and interest coverage

- Diversified revenue streams across consulting, outsourcing, and multiple sectors

- Broad global presence with significant revenue in North America and Europe

Globant S.A. Strengths

- Favorable liquidity with current and quick ratios at 1.54

- Conservative leverage with low debt-to-assets and favorable interest coverage

- Geographic diversification with presence in North America, Latin America, Europe, and Asia

- Favorable fixed asset turnover indicating efficient asset use

- Growing global footprint in multiple emerging and developed markets

Accenture plc Weaknesses

- Unfavorable high price-to-book ratio at 5.21

- Neutral valuation metrics with PE at 21.16

- Limited product revenue diversification compared to total revenue

- Moderate current ratio at 1.42, neutral status

- Relatively high PB compared to sector benchmarks

Globant S.A. Weaknesses

- Low profitability metrics with 6.86% net margin and 8.44% ROE marked unfavorable

- High PE ratio at 57.64 indicates possible overvaluation

- Absence of dividend yield, unfavorable for income investors

- Asset turnover at 0.76 is neutral, below Accenture’s efficiency

- Higher proportion of unfavorable ratios at 28.57% compared to peer

Accenture demonstrates stronger profitability and capital efficiency, supported by diversified revenues and a robust global presence. Globant shows solid liquidity and geographic reach but faces challenges in profitability and valuation metrics. These factors shape each company’s strategic focus in market positioning and financial management.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat shields long-term profits from relentless competition erosion. Let’s dissect the unique moats of these tech services firms:

Accenture plc: Scale and Intangible Asset Moat

Accenture’s moat arises from vast scale and deep intangible assets like brand and client relationships. It sustains high ROIC at 7.6%, well above WACC, despite a recent decline. Expansion in cloud and AI services in 2026 could reinforce this position.

Globant S.A.: Innovation and Growth-Oriented Moat

Globant’s moat leans on innovation and rapid growth, reflected in improving ROIC trends but still below WACC by 2.2%. Unlike Accenture, Globant excels in digital transformation niches, with 196% revenue growth over five years, signaling potential market disruption.

Verdict: Scale and Intangibles vs. Innovation Velocity

Accenture holds the deeper moat with consistent value creation through scale and client lock-in. Globant’s rising profitability shows promise but lacks the durable economic profit. Accenture is better equipped to defend its market share long term.

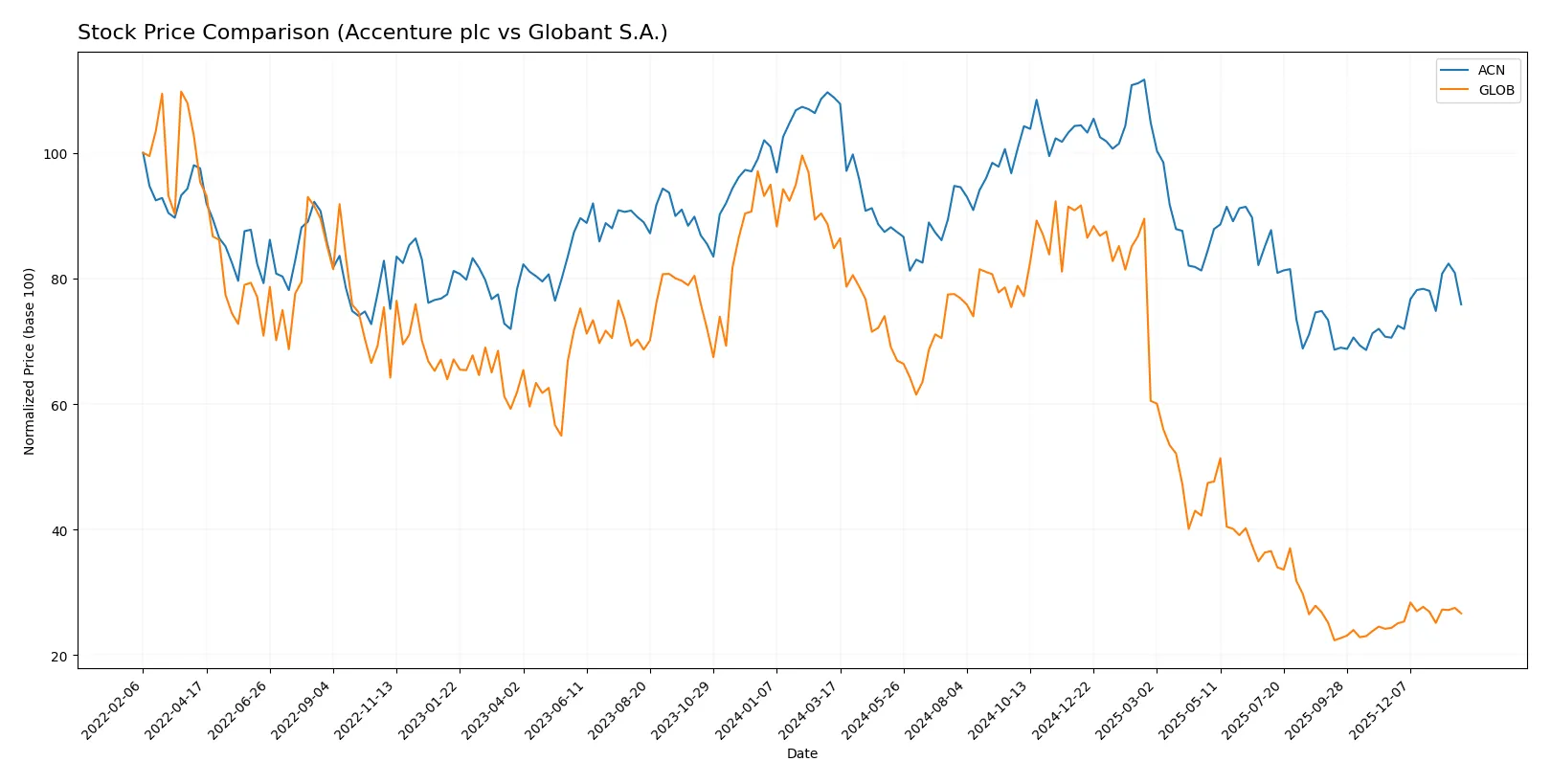

Which stock offers better returns?

The past year shows both Accenture plc and Globant S.A. enduring significant price declines with recent positive momentum emerging in late 2025, reflecting shifting trading dynamics and acceleration in their trends.

Trend Comparison

Accenture plc’s stock fell 30.29% over the past 12 months, marking a bearish trend with accelerating decline. The price ranged from $388 to $238, with recent gains of 7.52% signaling a short-term recovery.

Globant S.A. experienced a sharper 68.54% drop, also bearish and accelerating. The stock fluctuated between $231 and $56, but recent gains of 9.51% indicate a modest rebound despite high volatility.

Comparing both, Accenture delivered a less severe decline than Globant, resulting in relatively better market performance over the year despite recent positive shifts in both stocks.

Target Prices

Analysts present a confident target price consensus for Accenture plc and Globant S.A.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Accenture plc | 265 | 330 | 302.93 |

| Globant S.A. | 68 | 80 | 73.75 |

The target consensus for Accenture exceeds its current price of 264, signaling upside potential. Globant’s consensus also sits above its current 67 price, reflecting modest bullish expectations.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Accenture plc Grades

Below are recent institutional grades for Accenture plc from notable firms:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Wells Fargo | Maintain | Equal Weight | 2026-01-14 |

| UBS | Maintain | Buy | 2025-12-19 |

| Susquehanna | Maintain | Neutral | 2025-12-19 |

| RBC Capital | Maintain | Outperform | 2025-12-19 |

| Morgan Stanley | Upgrade | Overweight | 2025-12-16 |

| Mizuho | Maintain | Outperform | 2025-09-29 |

| Evercore ISI Group | Maintain | Outperform | 2025-09-26 |

| BMO Capital | Maintain | Market Perform | 2025-09-26 |

| TD Cowen | Maintain | Buy | 2025-09-26 |

| Goldman Sachs | Maintain | Buy | 2025-09-26 |

Globant S.A. Grades

Institutional grades for Globant S.A. from recognized analysts are summarized below:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Wells Fargo | Maintain | Equal Weight | 2026-01-14 |

| Jefferies | Downgrade | Hold | 2025-11-20 |

| UBS | Maintain | Neutral | 2025-11-18 |

| Needham | Maintain | Buy | 2025-11-14 |

| Canaccord Genuity | Maintain | Hold | 2025-11-14 |

| JP Morgan | Maintain | Neutral | 2025-11-14 |

| Goldman Sachs | Maintain | Neutral | 2025-10-09 |

| UBS | Maintain | Neutral | 2025-08-20 |

| Goldman Sachs | Maintain | Neutral | 2025-08-18 |

| Needham | Maintain | Buy | 2025-08-15 |

Which company has the best grades?

Accenture plc consistently receives stronger grades, including multiple “Buy,” “Outperform,” and an upgrade to “Overweight.” Globant’s ratings cluster around “Neutral” and “Hold,” with fewer “Buy” recommendations. Investors could interpret Accenture’s superior ratings as greater institutional confidence.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

Accenture plc

- Dominates large enterprise consulting with strong global presence but faces pressure from digital disruptors.

Globant S.A.

- Smaller scale with niche digital services; high competition in tech innovation limits market share growth.

2. Capital Structure & Debt

Accenture plc

- Maintains low debt-to-equity (0.26) and strong interest coverage (45.94), indicating robust financial stability.

Globant S.A.

- Also low leverage (D/E 0.21) but significantly lower interest coverage (8.87) signals less cushion against rising rates.

3. Stock Volatility

Accenture plc

- Beta at 1.249 reflects moderate volatility typical of tech consulting leaders, with stable market cap of $163B.

Globant S.A.

- Beta slightly lower at 1.204 but price range is wide ($54-$229), indicating episodic high volatility and speculative swings.

4. Regulatory & Legal

Accenture plc

- Faces complex global compliance in data privacy and labor laws due to scale and multinational operations.

Globant S.A.

- Exposed to regulatory risks in emerging digital sectors and multiple jurisdictions, especially EU and US tech regulations.

5. Supply Chain & Operations

Accenture plc

- Extensive global delivery model mitigates risks but depends on talent availability and operational efficiency.

Globant S.A.

- Smaller workforce (31K vs 801K) creates agility but increases vulnerability to operational disruptions and talent shortages.

6. ESG & Climate Transition

Accenture plc

- Demonstrates strong ESG focus with sustainability consulting and zero-based budgeting services supporting climate goals.

Globant S.A.

- Emerging ESG initiatives but less mature framework and lower public visibility may impact client acquisition in green sectors.

7. Geopolitical Exposure

Accenture plc

- Broad geographic footprint exposes it to global geopolitical tensions but also diversifies risk.

Globant S.A.

- Concentrated in fewer regions, increasing vulnerability to localized geopolitical instability and trade disruptions.

Which company shows a better risk-adjusted profile?

Accenture’s strongest risk lies in intense market competition amid rapid tech shifts. Globant’s biggest risk is stock volatility tied to its smaller scale and speculative valuation. Accenture’s robust capital structure and diversified operations provide a superior risk-adjusted profile. Recent data show Globant’s high P/E ratio (57.64) amplifies downside risk, while Accenture balances growth with financial strength.

Final Verdict: Which stock to choose?

Accenture plc’s superpower lies in its robust capital efficiency and consistent value creation. Its ability to generate strong returns well above its cost of capital sets it apart. A point of vigilance remains its slightly declining ROIC trend, signaling the need for careful monitoring. It suits portfolios aiming for stable, long-term growth with moderate risk tolerance.

Globant S.A. boasts a strategic moat rooted in its accelerating profitability and improving capital returns, despite currently shedding value. Its higher growth potential comes with more volatility and a weaker financial cushion than Accenture. This profile fits investors seeking Growth at a Reasonable Price (GARP) exposure with a tolerance for cyclical swings.

If you prioritize reliable value creation and operational resilience, Accenture outshines as the compelling choice due to its proven track record and financial stability. However, if you seek dynamic growth with an improving profitability trajectory, Globant offers superior upside potential, albeit with elevated risk. Both represent distinct analytical scenarios tailored to differing investor appetites.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Accenture plc and Globant S.A. to enhance your investment decisions: