Home > Comparison > Healthcare > ABT vs PODD

The strategic rivalry between Abbott Laboratories and Insulet Corporation shapes the healthcare medical devices sector. Abbott operates a diversified, capital-intensive model spanning pharmaceuticals, diagnostics, and devices. In contrast, Insulet focuses on high-growth, niche insulin delivery systems with a leaner operational footprint. This head-to-head pits scale and diversification against innovation and specialization. This analysis will determine which trajectory offers superior risk-adjusted returns for a balanced, diversified portfolio.

Table of contents

Companies Overview

Abbott Laboratories and Insulet Corporation both occupy pivotal roles in the medical devices sector, shaping healthcare innovation and patient care.

Abbott Laboratories: Diversified Medical Innovator

Abbott Laboratories commands a diversified healthcare portfolio spanning pharmaceuticals, diagnostics, nutrition, and medical devices. Its core revenue derives from a mix of generic pharmaceuticals and advanced diagnostic systems. In 2026, Abbott sharpens its strategic focus on expanding cardiovascular and diabetes care device offerings, leveraging its broad product ecosystem to sustain competitive advantage.

Insulet Corporation: Diabetes Device Specialist

Insulet Corporation centers on insulin delivery innovation, primarily through its Omnipod tubeless insulin pump system. Revenue depends heavily on sales of this self-adhesive, wearable device and its wireless management companion. The company’s 2026 strategy targets geographic expansion and channel diversification to capture more market share in insulin-dependent diabetes care globally.

Strategic Collision: Similarities & Divergences

Abbott adopts a broad, integrated healthcare model, while Insulet pursues a focused, specialized device niche. Their primary battleground is diabetes care technology, where Abbott’s scale and product breadth meet Insulet’s innovation and agility. Investors face distinct profiles: Abbott offers stability through diversification; Insulet presents growth potential tied to a concentrated product line.

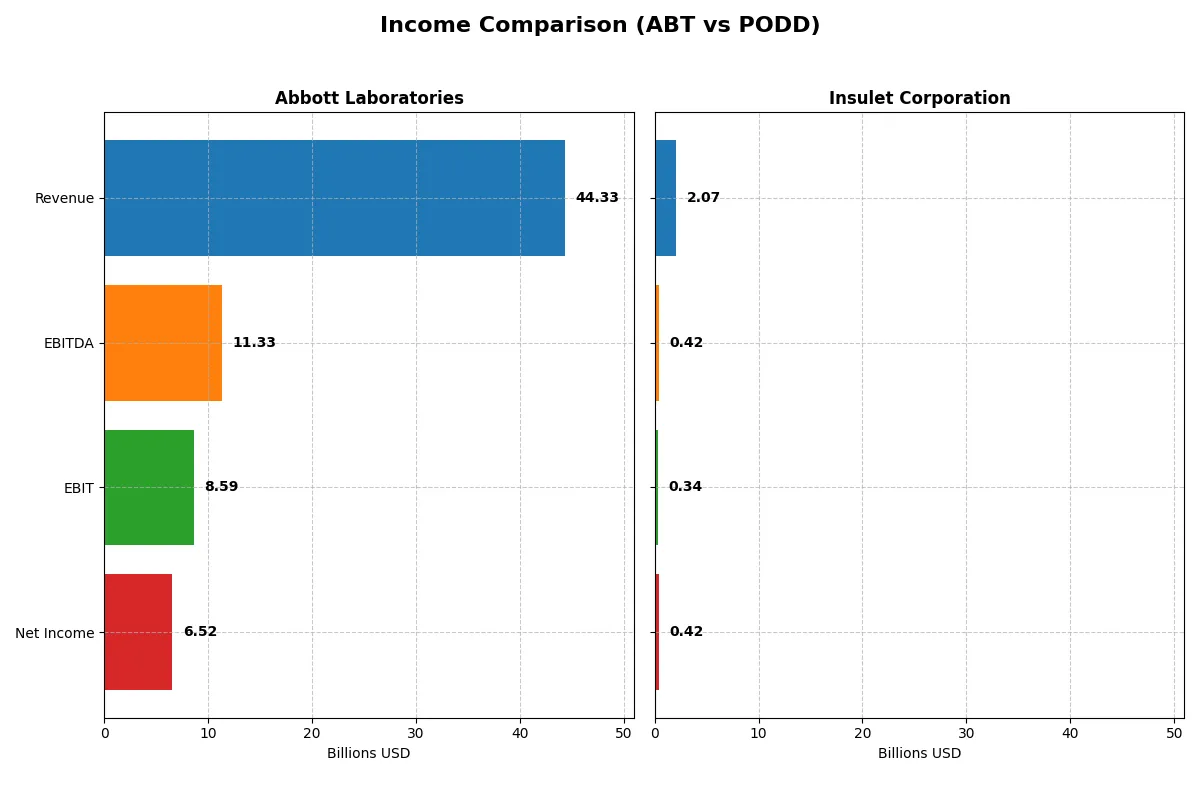

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Abbott Laboratories (ABT) | Insulet Corporation (PODD) |

|---|---|---|

| Revenue | 44.3B | 2.07B |

| Cost of Revenue | 19.7B | 626M |

| Operating Expenses | 16.6B | 1.14B |

| Gross Profit | 24.6B | 1.45B |

| EBITDA | 11.3B | 424M |

| EBIT | 8.59B | 343M |

| Interest Expense | 341M | 43M |

| Net Income | 6.52B | 418M |

| EPS | 3.74 | 5.97 |

| Fiscal Year | 2025 | 2024 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals which company runs a more efficient and profitable business engine over recent years.

Abbott Laboratories Analysis

Abbott’s revenue climbed steadily from $43B in 2021 to $44.3B in 2025, but net income dipped overall, ending at $6.5B in 2025. Gross margin remained solid near 55.5%, while net margin softened to 14.7%. Despite a 5.7% revenue rise in 2025, net income and EPS suffered a sharp decline, signaling margin pressure and cost challenges.

Insulet Corporation Analysis

Insulet surged revenue from $904M in 2020 to $2.07B in 2024, with net income exploding from $6.8M to $418M. Gross margin sustained a healthy 69.8%, and net margin expanded impressively to 20.2%. The latest year showed strong momentum with 22% revenue growth and a near doubling of EPS, reflecting robust operational leverage and margin expansion.

Growth Momentum vs. Margin Resilience

Insulet’s income statement exhibits superior growth and margin expansion, outpacing Abbott’s slower revenue increase and margin erosion. Insulet’s aggressive revenue and profit gains define it as the fundamental winner in efficiency and scalability. Investors seeking dynamic growth and improving profitability will find Insulet’s profile more compelling than Abbott’s steady but pressured results.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | Abbott Laboratories (ABT) | Insulet Corporation (PODD) |

|---|---|---|

| ROE | 28.1% (2024) | 34.5% (2024) |

| ROIC | 9.9% (2024) | 11.7% (2024) |

| P/E | 14.6x (2024) | 43.7x (2024) |

| P/B | 4.1x (2024) | 15.1x (2024) |

| Current Ratio | 1.67 (2024) | 3.54 (2024) |

| Quick Ratio | 1.23 (2024) | 2.73 (2024) |

| D/E | 0.32 (2024) | 1.17 (2024) |

| Debt-to-Assets | 18.8% (2024) | 46.1% (2024) |

| Interest Coverage | 11.3x (2024) | 7.2x (2024) |

| Asset Turnover | 0.52 (2024) | 0.67 (2024) |

| Fixed Asset Turnover | 3.58 (2024) | 2.73 (2024) |

| Payout Ratio | 28.6% (2024) | 0% (2024) |

| Dividend Yield | 1.96% (2024) | 0% (2024) |

| Fiscal Year | 2024 | 2024 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios act as a company’s DNA, revealing hidden risks and operational excellence behind surface numbers.

Abbott Laboratories

Abbott shows a solid net margin of 14.72%, but its ROE and ROIC are missing, signaling potential concerns about capital efficiency. The P/E ratio stands at 33.55, indicating a stretched valuation relative to earnings. Abbott returns 1.88% in dividends, balancing moderate shareholder payouts with ongoing R&D investment.

Insulet Corporation

Insulet exhibits robust profitability with a 20.19% net margin and a strong 34.52% ROE, reflecting efficient capital use. However, its P/E ratio at 43.74 and P/B at 15.1 signal an expensive stock. It pays no dividend, likely reinvesting aggressively into growth and innovation, supported by a favorable quick ratio of 2.73.

Valuation Stretch vs. Profitability Strength

Abbott offers a more conservative valuation with modest dividends but lacks clear capital efficiency. Insulet delivers superior profitability and reinvestment but trades at a high premium. Investors favoring stability may lean toward Abbott, while growth-oriented profiles align better with Insulet’s dynamic metrics.

Which one offers the Superior Shareholder Reward?

Abbott Laboratories (ABT) pays a consistent dividend with a 1.96% yield and a prudent 29% payout ratio, supported by strong free cash flow. Its steady buyback program reinforces shareholder returns sustainably. Insulet Corporation (PODD) offers no dividends but aggressively reinvests in growth, reflected by high leverage and volatile cash flows, with limited buybacks. I see ABT’s balanced dividend and buyback strategy as the superior, more reliable total return profile for 2026 investors.

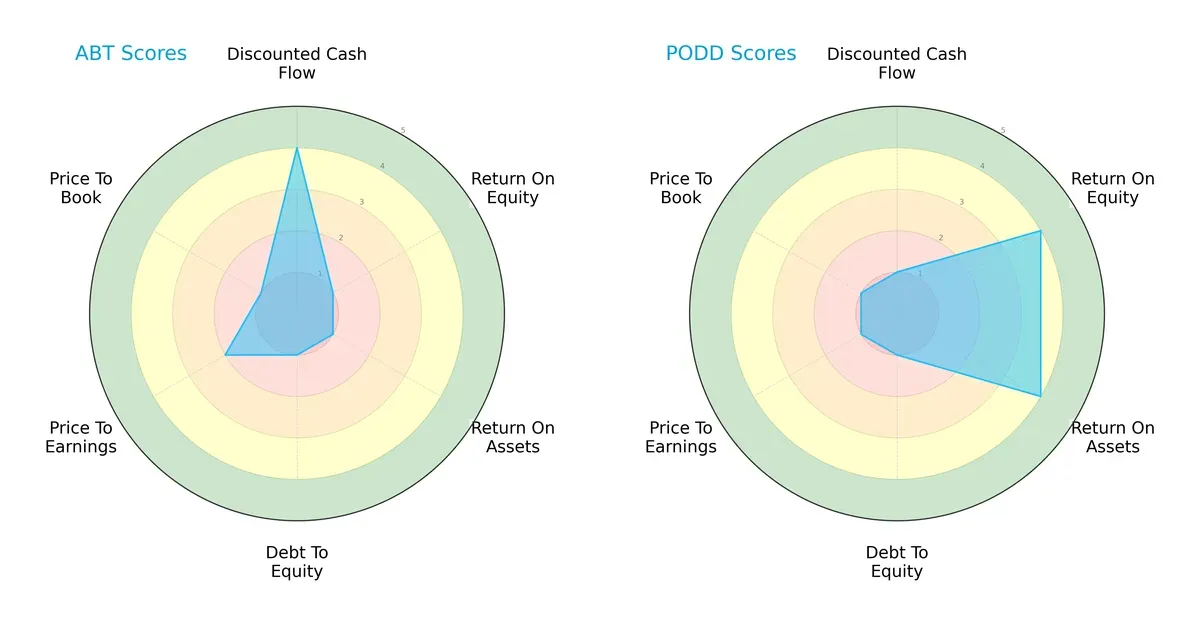

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Abbott Laboratories and Insulet Corporation’s financial profiles:

Abbott leads with a strong Discounted Cash Flow score (4) but struggles in operational efficiency, shown by low ROE (1) and ROA (1). Insulet excels in ROE (4) and ROA (4), signaling superior asset utilization and profitability. Both firms share weak Debt/Equity (1) and Price-to-Book (1) scores, indicating balance sheet risks and potential overvaluation. Abbott’s profile is imbalanced with reliance on cash flow strength, while Insulet leverages operational excellence but faces valuation challenges.

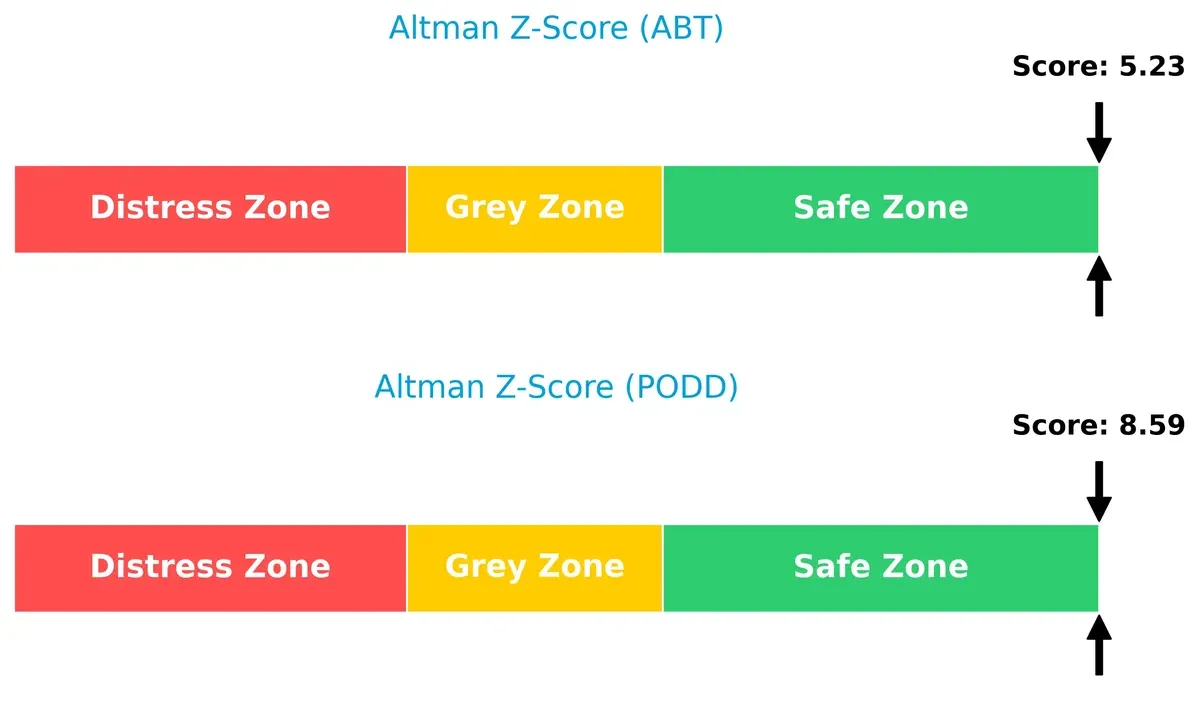

Bankruptcy Risk: Solvency Showdown

Insulet’s Altman Z-Score (8.59) significantly outpaces Abbott’s (5.23), reflecting a safer financial footing for long-term survival in this cycle:

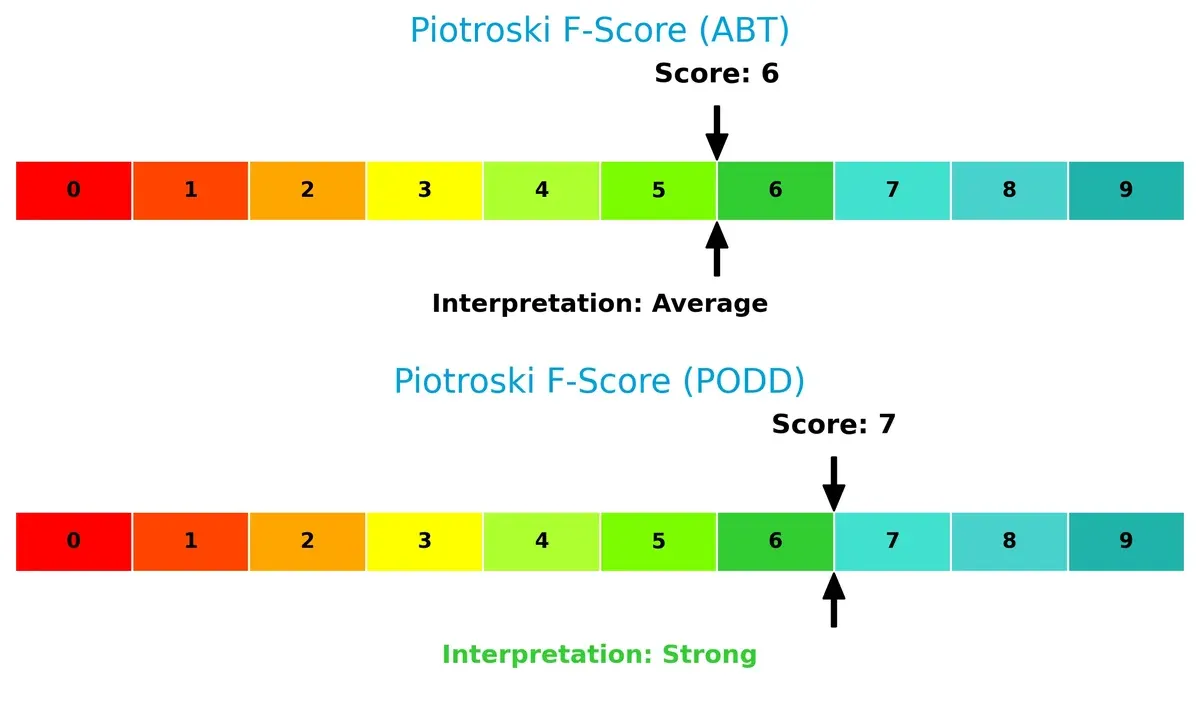

Financial Health: Quality of Operations

Insulet’s Piotroski F-Score of 7 surpasses Abbott’s 6, signaling stronger internal financial health and fewer red flags in operational metrics:

How are the two companies positioned?

This section dissects the operational DNA of Abbott Laboratories and Insulet Corporation by comparing their revenue distribution and internal dynamics. The goal is to confront their economic moats to identify which model offers the most resilient competitive advantage today.

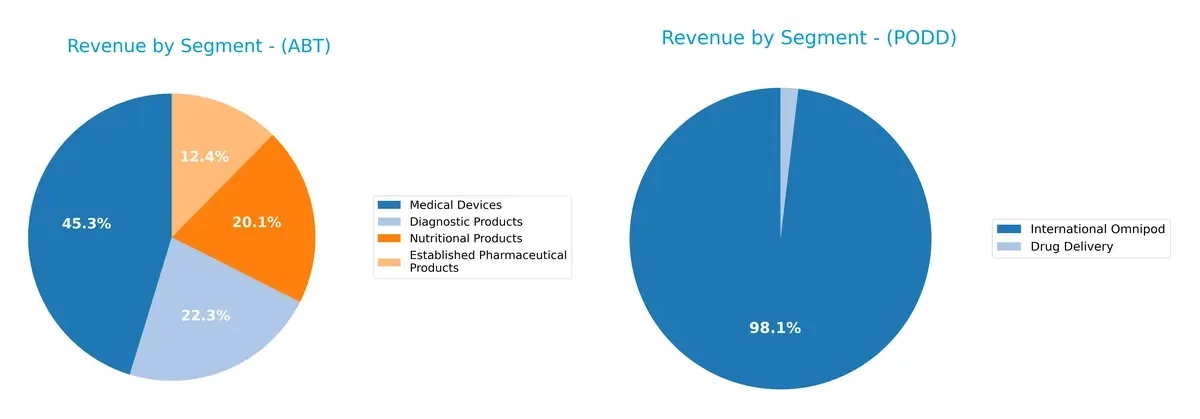

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how Abbott Laboratories and Insulet Corporation diversify their income streams and where their primary sector bets lie:

I observe Abbott Laboratories anchors revenue in Medical Devices at $19B, with strong contributions from Diagnostic Products ($9.3B), Nutritional Products ($8.4B), and Established Pharmaceuticals ($5.2B). This diversified mix cushions Abbott against sector-specific shocks. In contrast, Insulet relies heavily on International Omnipod at $2B, with Drug Delivery trailing at $39M, exposing it to concentration risk but signaling focused dominance in insulin delivery technology.

Strengths and Weaknesses Comparison

This table compares the strengths and weaknesses of Abbott Laboratories and Insulet Corporation based on diversification, profitability, financials, innovation, global presence, and market share:

Abbott Laboratories Strengths

- Broad product diversification across diagnostics, devices, pharma, nutrition

- Strong global presence with significant US and Non-US revenue

- Favorable net margin of 14.72%

- High interest coverage ratio of 25.18 indicating solid debt servicing ability

Insulet Corporation Strengths

- Higher net margin of 20.19% and strong ROE of 34.52% showing superior profitability

- Favorable ROIC of 11.68% above WACC

- Favorable quick ratio and interest coverage

- Focused innovation in drug delivery with growing international sales

Abbott Laboratories Weaknesses

- Unfavorable ROE and ROIC at 0% reflect poor capital efficiency

- Unfavorable current and quick ratios suggest liquidity concerns

- High P/E ratio of 33.55 may imply overvaluation

- Unfavorable asset turnover ratios signal operational inefficiency

Insulet Corporation Weaknesses

- Unfavorable P/E and P/B ratios indicate possible overvaluation

- Debt to equity at 1.17 and moderate debt to assets highlight leverage risk

- Unfavorable current ratio despite favorable quick ratio

- No dividend yield may deter income-focused investors

Abbott’s strengths lie in its diversified portfolio and global revenue base but face capital efficiency and liquidity challenges. Insulet shows strong profitability and innovation focus but carries valuation and leverage risks that merit caution.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only true safeguard protecting long-term profits from the relentless erosion of competition. Let’s examine how Abbott Laboratories and Insulet Corporation defend their turf:

Abbott Laboratories: Diversification and Scale

Abbott’s moat stems from its diversified medical portfolio and global scale. This manifests in stable margins around 19% EBIT and broad geographic reach. However, declining ROIC signals pressure on efficiency, and margin growth faces headwinds in 2026.

Insulet Corporation: Innovation-Driven Network Effects

Insulet’s moat relies on innovative insulin delivery systems and growing user adoption, reflected in strong 70% gross margins and rapid revenue growth of 22%. Its expanding ROIC trend suggests deepening competitive advantages and potential market disruption ahead.

Verdict: Diversification vs. Innovation Momentum

Abbott’s broad diversification offers a wide, but currently pressured, moat. Insulet’s focused innovation delivers a narrower, yet rapidly deepening, moat. I see Insulet as better positioned to defend and expand market share in 2026.

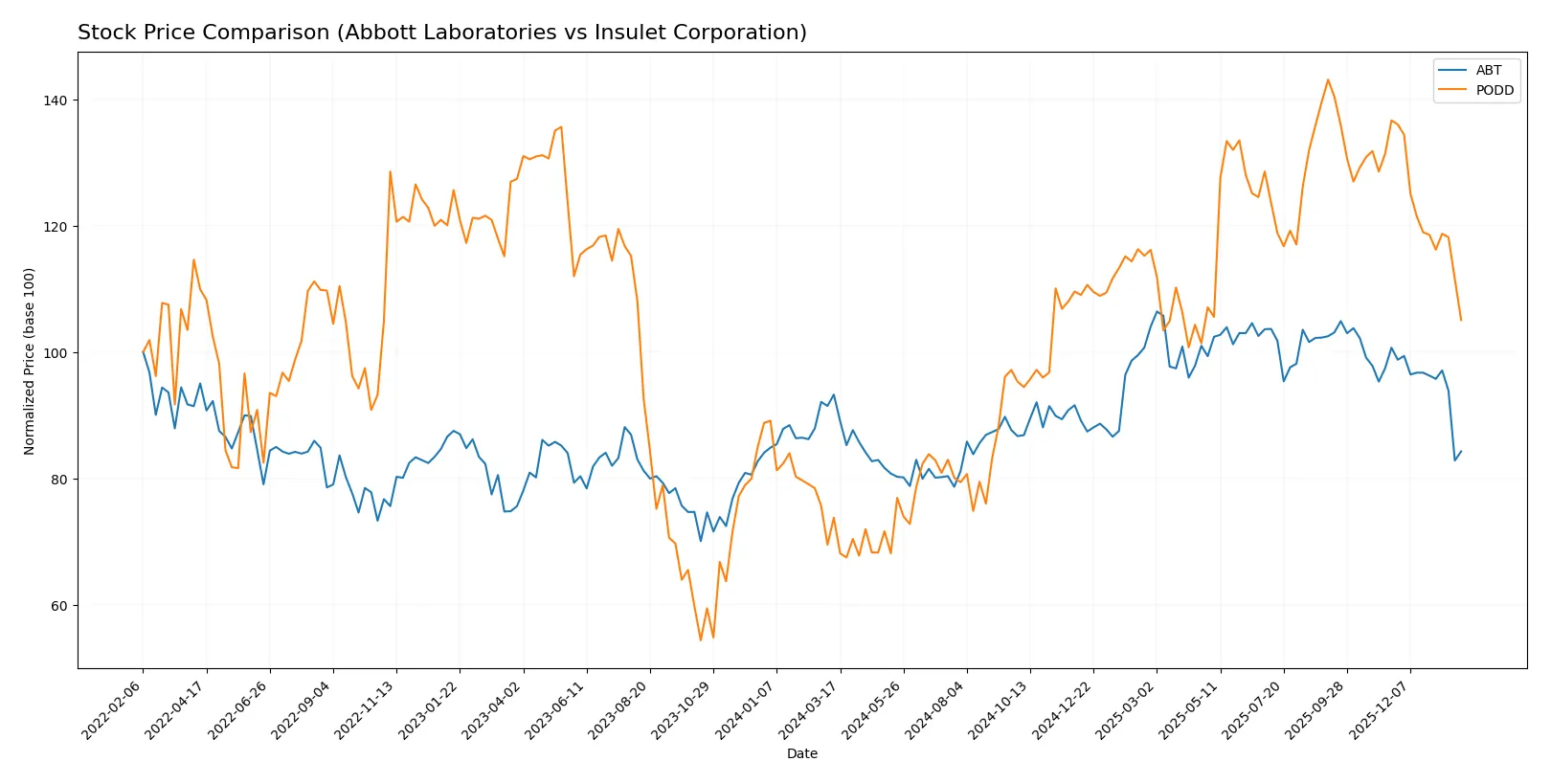

Which stock offers better returns?

The past year reveals stark contrasts: Abbott Laboratories’ shares fell nearly 10%, while Insulet Corporation surged over 40%, each showing distinct momentum shifts and trading volume dynamics.

Trend Comparison

Abbott Laboratories’ stock dropped 9.64% over the past 12 months, marking a bearish trend with decelerating losses and a high volatility of 10.54%. It peaked at 138.01 and troughed at 102.03.

Insulet Corporation’s shares rose 42.44% in the same period, confirming a bullish trend despite deceleration. Volatility is high at 52.54%, with prices ranging between 164.31 and 348.43.

Insulet outpaced Abbott significantly, delivering the highest market performance, though both showed recent short-term declines amid volatile trading conditions.

Target Prices

Analysts show a bullish outlook with strong upside potential for both Abbott Laboratories and Insulet Corporation.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Abbott Laboratories | 120 | 169 | 137.09 |

| Insulet Corporation | 274 | 450 | 378.9 |

Abbott’s consensus target price of 137.09 implies a 25% upside from the current 109.3 price. Insulet’s target consensus at 378.9 suggests a nearly 48% potential gain from 255.81.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Abbott Laboratories Grades

The following table summarizes recent grades issued by major financial institutions for Abbott Laboratories.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Citigroup | Maintain | Buy | 2026-01-23 |

| BTIG | Maintain | Buy | 2026-01-23 |

| Evercore ISI Group | Maintain | Outperform | 2026-01-23 |

| Bernstein | Maintain | Outperform | 2026-01-23 |

| Piper Sandler | Maintain | Overweight | 2026-01-23 |

| Oppenheimer | Maintain | Outperform | 2026-01-23 |

| RBC Capital | Maintain | Outperform | 2026-01-23 |

| Bernstein | Maintain | Outperform | 2026-01-09 |

| Barclays | Maintain | Overweight | 2026-01-05 |

| BTIG | Maintain | Buy | 2025-11-20 |

Insulet Corporation Grades

Below is a table showing recent grades from reputable institutions for Insulet Corporation.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Barclays | Downgrade | Underweight | 2026-01-12 |

| Bernstein | Maintain | Outperform | 2026-01-09 |

| Truist Securities | Maintain | Buy | 2025-12-18 |

| Canaccord Genuity | Maintain | Buy | 2025-12-17 |

| Canaccord Genuity | Maintain | Buy | 2025-11-24 |

| BTIG | Maintain | Buy | 2025-11-21 |

| Truist Securities | Maintain | Buy | 2025-11-21 |

| RBC Capital | Maintain | Outperform | 2025-11-21 |

| UBS | Upgrade | Buy | 2025-11-19 |

| BTIG | Maintain | Buy | 2025-11-13 |

Which company has the best grades?

Abbott Laboratories consistently receives “Buy” and “Outperform” ratings with no downgrades, signaling strong institutional confidence. Insulet Corporation faces a recent downgrade to “Underweight,” despite several “Buy” and “Outperform” ratings. This divergence suggests Abbott holds a steadier analyst endorsement, impacting investor sentiment toward greater stability.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

Abbott Laboratories

- Large diversified healthcare portfolio cushions market shifts but faces intense competition in diagnostics and devices.

Insulet Corporation

- Focused on insulin delivery systems; niche leadership but vulnerable to innovation by larger competitors.

2. Capital Structure & Debt

Abbott Laboratories

- Strong interest coverage at 25.18x and favorable debt-to-assets ratio indicate solid financial stability.

Insulet Corporation

- Moderate debt-to-assets at 46%, interest coverage of 8x; higher leverage increases financial risk.

3. Stock Volatility

Abbott Laboratories

- Beta of 0.72 implies lower volatility than market, appealing for risk-averse investors.

Insulet Corporation

- Beta at 1.4 signals higher price swings, reflecting growth stock risk and market sensitivity.

4. Regulatory & Legal

Abbott Laboratories

- Broad regulatory exposure across pharmaceuticals and devices; compliance costs are significant but manageable.

Insulet Corporation

- Medical device regulatory scrutiny intense; any FDA delays or recalls could disrupt growth trajectory.

5. Supply Chain & Operations

Abbott Laboratories

- Global scale and diversified suppliers reduce supply chain risk but complexity remains high.

Insulet Corporation

- Smaller scale heightens supply chain vulnerability, especially for proprietary Omnipod components.

6. ESG & Climate Transition

Abbott Laboratories

- Larger company with established ESG programs; climate transition risks are integrated into operations.

Insulet Corporation

- Emerging ESG initiatives; limited scale may delay climate adaptation and sustainability investments.

7. Geopolitical Exposure

Abbott Laboratories

- Global footprint exposes it to geopolitical tensions but provides revenue diversification.

Insulet Corporation

- Primarily US and select international markets; geopolitical risks concentrated but less diversified.

Which company shows a better risk-adjusted profile?

Abbott’s most impactful risk is its broad regulatory and competitive pressure across multiple segments, which can strain resources. Insulet faces critical risks in its high leverage and supply chain concentration. Abbott’s lower beta and stronger capital structure provide a more balanced risk-adjusted profile. Notably, Insulet’s higher beta of 1.4 compared to Abbott’s 0.72 confirms its elevated market volatility, justifying cautious positioning despite growth potential.

Final Verdict: Which stock to choose?

Abbott Laboratories’ superpower lies in its established scale and operational resilience, generating steady cash flow in a challenging healthcare landscape. Its declining profitability trends and mixed financial signals are points of vigilance. It suits portfolios seeking defensive exposure with moderate growth expectations.

Insulet Corporation boasts a strategic moat through innovative diabetes management technology and strong top-line momentum. Its rapidly improving profitability and strong cash conversion cycle offer growth upside, though higher leverage and valuation multiples add risk. It fits growth-oriented portfolios willing to tolerate volatility for superior returns.

If you prioritize stability and consistent cash generation, Abbott Laboratories is the compelling choice due to its market presence and operational resilience. However, if you seek aggressive growth and can weather earnings swings, Insulet offers better momentum and expanding profitability, commanding a premium for its innovation-driven potential.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Abbott Laboratories and Insulet Corporation to enhance your investment decisions: