Home > Analyses > Consumer Cyclical > Chipotle Mexican Grill, Inc.

Chipotle revolutionizes fast casual dining by blending speed with fresh, customizable Mexican cuisine. It commands a leading position in the restaurant industry, known for high-quality ingredients and strong brand loyalty. With around 3,000 locations across North America and Europe, Chipotle drives innovation in menu offerings and digital ordering. As competition intensifies, I question whether its current fundamentals justify its market valuation and growth prospects heading into 2026.

Table of contents

Business Model & Company Overview

Chipotle Mexican Grill, Inc., founded in 1993 and headquartered in Newport Beach, CA, commands a prominent position in the global restaurant industry. With approximately 3,000 locations across the United States, Canada, and Europe, it offers a cohesive ecosystem centered on customizable Mexican cuisine that blends quality ingredients with fast casual convenience. This approach resonates with evolving consumer preferences and drives brand loyalty.

The company’s revenue engine balances in-restaurant sales with expanding digital orders and catering services, fueling growth across the Americas and Europe. Its strategic footprint in diverse markets enhances resilience against regional volatility. Chipotle’s ability to consistently innovate menu offerings while scaling operations underpins its durable competitive advantage in a fragmented sector, positioning it as a key influencer in the fast-casual dining landscape.

Financial Performance & Fundamental Metrics

I will analyze Chipotle Mexican Grill, Inc.’s income statement, key financial ratios, and dividend payout policy to assess its core financial health and shareholder returns.

Income Statement

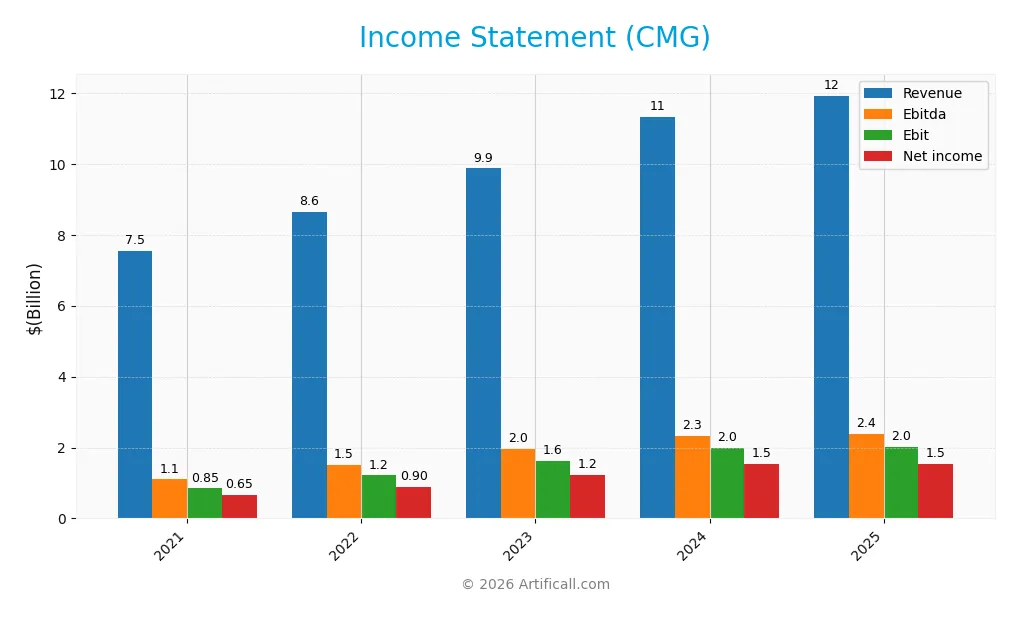

This table summarizes Chipotle Mexican Grill, Inc.’s key income statement figures for fiscal years 2021 through 2025, reflecting revenue, expenses, and profitability.

| 2021 | 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|---|

| Revenue | 7.55B | 8.63B | 9.87B | 11.31B | 11.93B |

| Cost of Revenue | 5.84B | 6.57B | 7.29B | 8.30B | 9.26B |

| Operating Expenses | 902M | 902M | 1.03B | 1.10B | 656M |

| Gross Profit | 1.71B | 2.06B | 2.59B | 3.02B | 2.66B |

| EBITDA | 1.10B | 1.50B | 1.95B | 2.32B | 2.37B |

| EBIT | 845M | 1.21B | 1.63B | 1.99B | 2.01B |

| Interest Expense | 0 | 0 | 0 | 0 | 0 |

| Net Income | 653M | 899M | 1.23B | 1.53B | 1.54B |

| EPS | 0.46 | 0.65 | 0.89 | 1.12 | 1.15 |

| Filing Date | 2022-02-11 | 2023-02-09 | 2024-02-08 | 2025-02-05 | 2026-02-04 |

Income Statement Evolution

From 2021 to 2025, Chipotle’s revenue grew 58%, reflecting solid expansion. Net income more than doubled, up 135%, driving strong margin improvement. Gross margin stabilized near 22%, while EBIT margin held favorably at 16.9%. However, year-over-year gross profit fell 11.7%, slightly pressuring profitability despite modest revenue gains. Net margin contracted 5%, signaling margin volatility.

Is the Income Statement Favorable?

In 2025, fundamentals remain generally favorable. Revenue rose 5.4% with consistent operating expense control, supporting a steady EBIT increase of 1.2%. Net margin of 12.9% and absence of interest expense enhance profitability. EPS grew 2.7%, reflecting shareholder value gains. Still, the recent gross profit decline and net margin dip warrant monitoring for sustained margin strength.

Financial Ratios

The following table presents key financial ratios for Chipotle Mexican Grill, Inc. over the last five fiscal years, providing insight into profitability, liquidity, leverage, and efficiency:

| Ratios | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Net Margin | 8.7% | 10.4% | 12.4% | 13.6% | 12.9% |

| ROE | 28.4% | 38.0% | 40.1% | 41.9% | 54.3% |

| ROIC | 10.8% | 14.1% | 16.3% | 17.0% | 18.9% |

| P/E | 75.3 | 43.0 | 51.3 | 53.8 | 32.2 |

| P/B | 21.4 | 16.3 | 20.6 | 22.6 | 17.5 |

| Current Ratio | 1.58 | 1.28 | 1.57 | 1.52 | 1.23 |

| Quick Ratio | 1.54 | 1.24 | 1.53 | 1.48 | 1.19 |

| D/E | 1.53 | 1.58 | 1.32 | 1.24 | 3.48 |

| Debt-to-Assets | 53.0% | 53.9% | 50.4% | 49.3% | 109.5% |

| Interest Coverage | 0 | 0 | 0 | 0 | 0 |

| Asset Turnover | 1.13 | 1.25 | 1.23 | 1.23 | 1.33 |

| Fixed Asset Turnover | 1.54 | 1.64 | 1.72 | 1.77 | 1.67 |

| Dividend Yield | 0% | 0% | 0% | 0% | 0% |

Evolution of Financial Ratios

Return on Equity (ROE) improved significantly from 28.4% in 2021 to 54.3% in 2025, reflecting stronger profitability. The Current Ratio declined from 1.58 in 2021 to 1.23 in 2025, indicating reduced liquidity. The Debt-to-Equity ratio surged from 1.53 to 3.48, suggesting increased leverage and financial risk over the period.

Are the Financial Ratios Favorable?

Profitability metrics like net margin (12.9%) and ROE (54.3%) are favorable, supported by ROIC (18.9%) exceeding WACC (7.6%). Liquidity shows mixed signals: a neutral current ratio (1.23) but a favorable quick ratio (1.19). Leverage is unfavorable with a high debt-to-equity ratio (3.48) and excessive debt-to-assets (109.5%). Market valuation ratios such as P/E (32.2) and P/B (17.5) are also unfavorable, indicating potential overvaluation. Overall, the financial ratios appear slightly favorable.

Shareholder Return Policy

Chipotle Mexican Grill, Inc. (CMG) does not pay dividends, reflecting a reinvestment strategy likely aimed at supporting growth and operational expansion. The company’s free cash flow remains positive, but no share buyback programs are evident in the recent fiscal years.

This approach aligns with CMG’s high growth phase, prioritizing capital allocation toward business development rather than immediate shareholder payouts. While this can support long-term value creation, it places emphasis on management’s execution and growth prospects to deliver returns to shareholders sustainably.

Score analysis

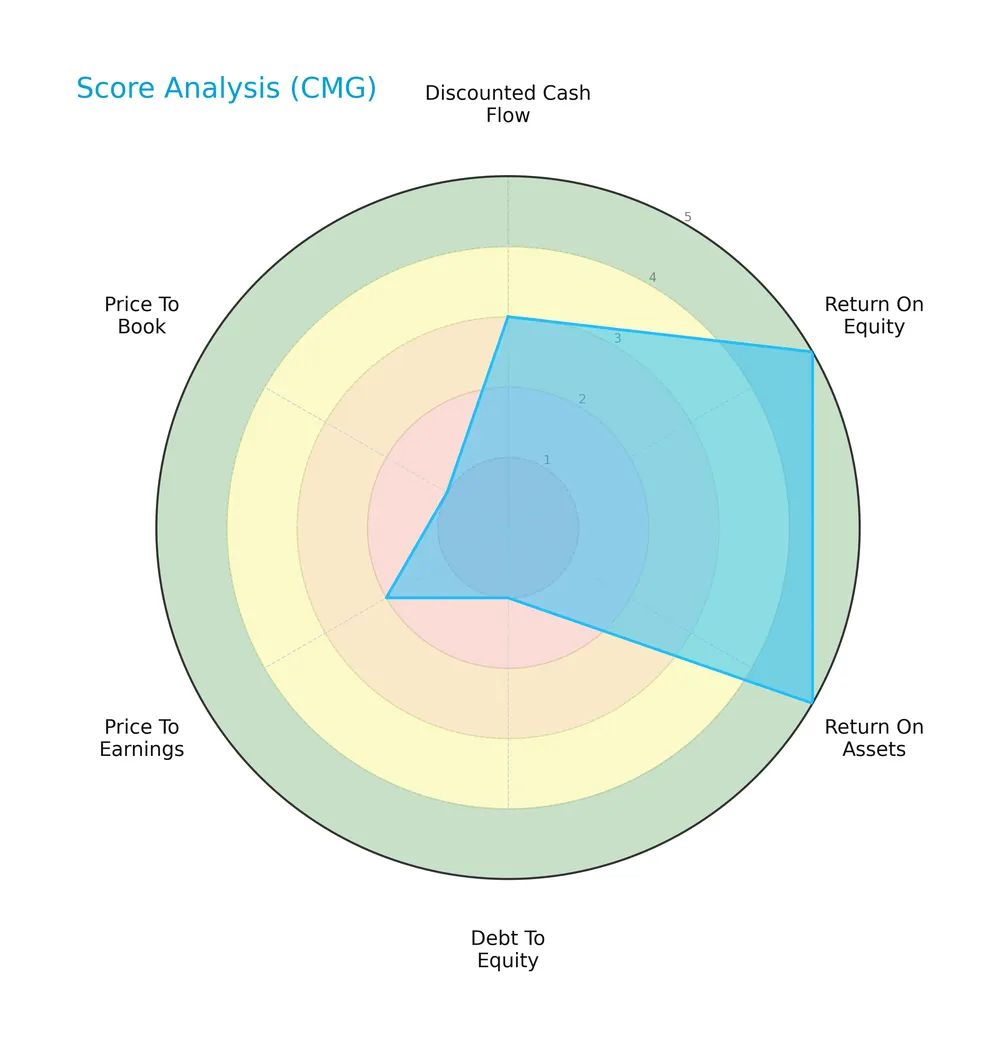

The following radar chart illustrates Chipotle Mexican Grill’s key financial metric scores for a comprehensive view:

Chipotle scores very favorably on return on equity and assets, indicating strong profitability and asset efficiency. However, it faces challenges with debt-to-equity and price-to-book ratios, reflecting leverage concerns and valuation risks. Other scores such as discounted cash flow and price-to-earnings are moderate.

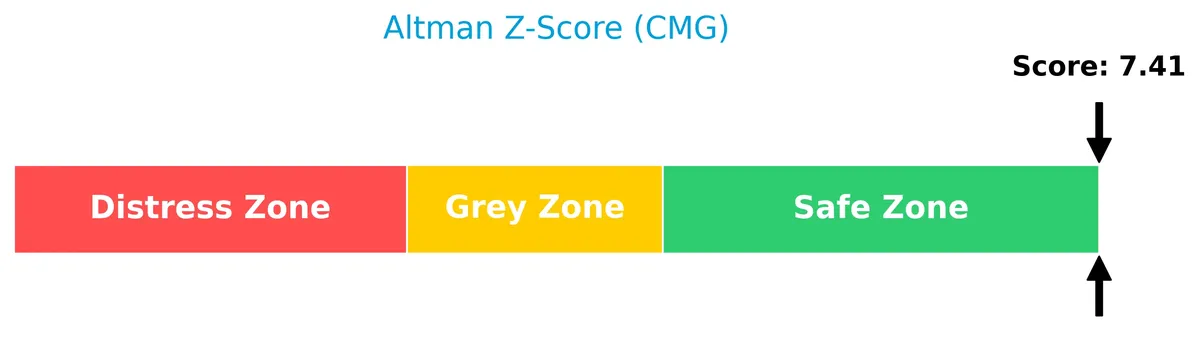

Analysis of the company’s bankruptcy risk

Chipotle’s Altman Z-Score places it firmly in the safe zone, indicating a very low risk of bankruptcy and strong financial stability:

Is the company in good financial health?

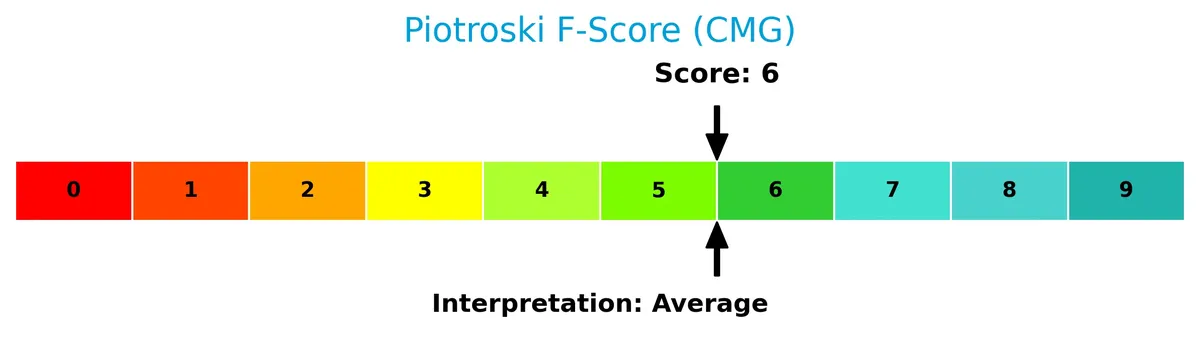

The Piotroski Score diagram provides insights into Chipotle’s financial strength based on multiple accounting criteria:

With a Piotroski Score of 6, the company demonstrates average financial health, suggesting solid but not exceptional fundamental strength. This score indicates decent profitability and operational efficiency with room for improvement.

Competitive Landscape & Sector Positioning

This sector analysis examines Chipotle Mexican Grill’s strategic positioning, revenue segments, key products, and main competitors. I will assess whether Chipotle holds a competitive advantage over its industry peers.

Strategic Positioning

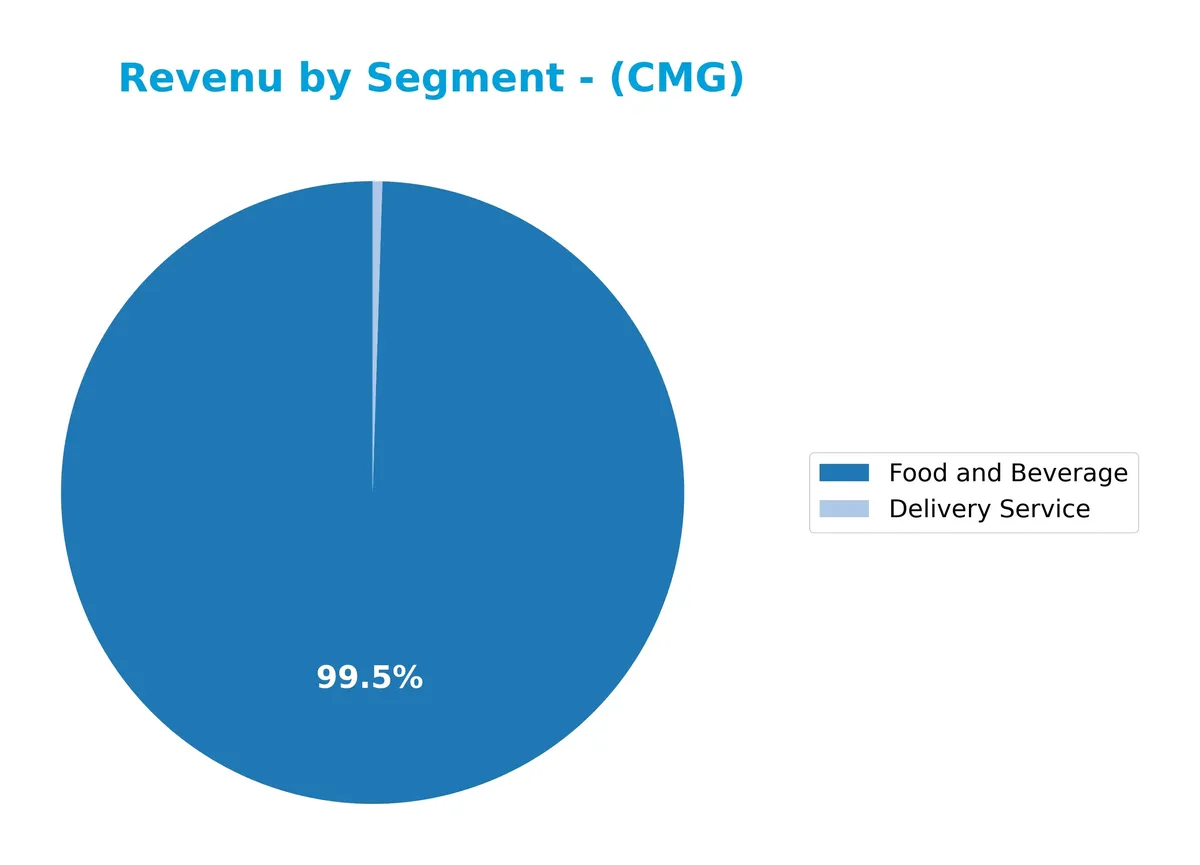

Chipotle Mexican Grill, Inc. concentrates its revenue predominantly on Food and Beverage, totaling $11.87B in 2025, with Delivery Service contributing $60M. Geographically, the company focuses almost entirely on the U.S. market, generating $11.68B in 2025, reflecting a concentrated product and geographic strategy.

Revenue by Segment

This pie chart illustrates Chipotle Mexican Grill’s revenue breakdown by segment for fiscal year 2025, highlighting the company’s core business sources over the period.

Chipotle’s revenue remains heavily concentrated in Food and Beverage, generating $11.87B in 2025, sustaining its role as the main growth driver. Delivery Service contributes a smaller $59.6M, showing a recent decline from prior years, signaling potential challenges or shifts in consumer ordering behavior. The company’s focus clearly lies in expanding core dining sales, with delivery revenue not yet scaling comparably, which suggests concentration risk but a strong moat in its restaurant operations.

Key Products & Brands

Chipotle generates revenue primarily through these key products and services:

| Product | Description |

|---|---|

| Food and Beverage | Core offering of freshly prepared Mexican-style meals served in restaurants worldwide. |

| Delivery Service | Revenue from meals ordered online or via app, delivered to customers’ locations. |

| Chipotle Rewards | Loyalty program driving customer engagement and repeat purchases (reported in 2019). |

| Gift Card | Prepaid cards usable at Chipotle locations, contributing to sales and customer retention (2018). |

Chipotle’s revenue base centers on its Food and Beverage segment, supplemented by growing Delivery Service sales. Loyalty and gift card programs support customer retention and incremental revenue.

Main Competitors

There are 6 main competitors in the Consumer Cyclical sector; the table below lists the top 6 leaders by market capitalization:

| Competitor | Market Cap. |

|---|---|

| McDonald’s Corporation | 217B |

| Starbucks Corporation | 95.5B |

| Chipotle Mexican Grill, Inc. | 50.6B |

| Yum! Brands, Inc. | 41.8B |

| Darden Restaurants, Inc. | 21.8B |

| Domino’s Pizza, Inc. | 14.4B |

Chipotle Mexican Grill ranks 3rd among its competitors with a market cap just 24% the size of McDonald’s, the sector leader. It stands below the 73.5B average market cap of the top 10 but above the 46.2B median for the sector. The company maintains a significant 85.65% gap over its closest rival, Starbucks.

Comparisons with competitors

Check out how we compare the company to its competitors:

Does CMG have a competitive advantage?

Chipotle Mexican Grill, Inc. presents a clear competitive advantage, demonstrated by its very favorable moat status. The company generates returns on invested capital (ROIC) well above its weighted average cost of capital (WACC), with ROIC increasing 75.6% over 2021-2025, signaling efficient capital use and sustained value creation.

Looking ahead, Chipotle’s expansion in the U.S. market, where it generated $11.7B revenue in 2025, offers growth opportunities. Continued innovation in its restaurant operations and potential new market entries support a positive outlook, reinforcing its ability to maintain and strengthen its competitive position.

SWOT Analysis

This analysis highlights Chipotle Mexican Grill’s key internal and external factors affecting its strategic position.

Strengths

- Strong brand recognition

- High ROIC of 18.9% exceeding WACC

- Expanding U.S. revenue base

Weaknesses

- Elevated debt-to-equity ratio of 3.48

- High price-to-book ratio of 17.48

- Negative gross profit growth in last year

Opportunities

- International market expansion

- Menu innovation and digital sales growth

- Rising demand for fast-casual dining

Threats

- Intense competition in restaurant sector

- Volatile food commodity prices

- Economic downturns impacting consumer spending

Chipotle’s robust profitability and moat create a durable competitive advantage. However, its leverage and valuation warrant caution. Strategic focus on international growth and innovation can mitigate competitive and economic risks.

Stock Price Action Analysis

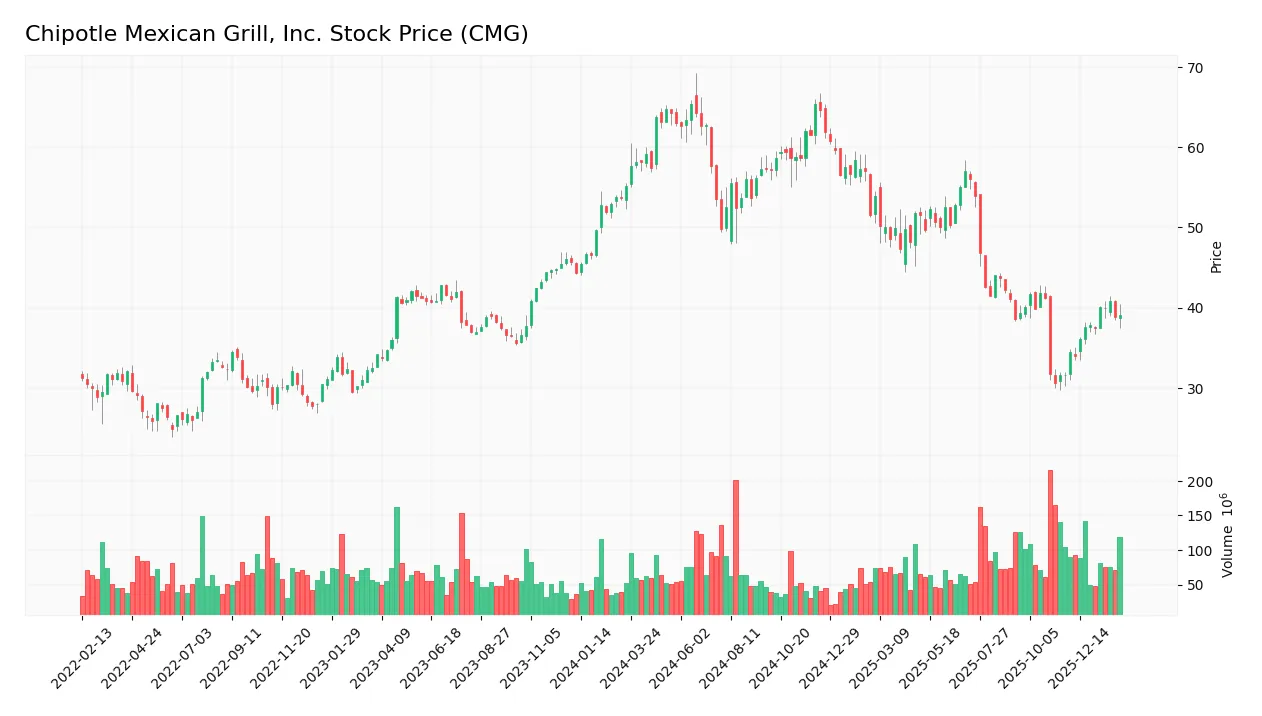

The following weekly chart illustrates Chipotle Mexican Grill, Inc.’s stock price movements over the last 100 weeks, highlighting key levels and recent volatility trends:

Trend Analysis

Over the past 12 months, CMG’s stock price declined sharply by 29.22%, confirming a bearish trend with accelerating downward momentum. The stock reached a high of 65.43 and a low of 30.59, exhibiting significant volatility with a standard deviation of 9.32. Notably, recent weeks show a partial recovery with a 23.36% gain since late November 2025.

Volume Analysis

Trading volumes have increased overall, totaling 8.5B shares exchanged. Buyer and seller volumes are nearly balanced historically, but the last three months show strong buyer dominance at 72.3%. This surge in buyer activity suggests heightened investor interest and potential accumulation during the recent price rebound.

Target Prices

Analysts set a clear target price consensus for Chipotle Mexican Grill, indicating moderate upside potential.

| Target Low | Target High | Consensus |

|---|---|---|

| 35 | 52 | 44.35 |

The target range spans from 35 to 52, with a consensus near 44.35, reflecting cautious optimism among analysts.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Analyst & Consumer Opinions

This section examines Chipotle Mexican Grill, Inc.’s analyst ratings alongside consumer feedback to provide a balanced perspective.

Stock Grades

Here are the latest verified stock grades from recognized research firms for Chipotle Mexican Grill, Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Argus Research | Maintain | Hold | 2026-02-05 |

| Telsey Advisory Group | Maintain | Outperform | 2026-02-04 |

| Morgan Stanley | Maintain | Overweight | 2026-02-04 |

| TD Cowen | Maintain | Buy | 2026-02-04 |

| Barclays | Maintain | Equal Weight | 2026-02-04 |

| Stephens & Co. | Maintain | Equal Weight | 2026-02-04 |

| Wells Fargo | Maintain | Overweight | 2026-02-04 |

| Mizuho | Maintain | Neutral | 2026-02-04 |

| Keybanc | Maintain | Overweight | 2026-02-04 |

| Piper Sandler | Maintain | Overweight | 2026-02-04 |

The consensus remains positive with a majority rating Chipotle as a Buy or Overweight. Most firms held their prior grades steady, showing confidence but no recent upgrades or downgrades.

Consumer Opinions

Chipotle Mexican Grill garners passionate feedback from its customers, reflecting a mix of strong brand loyalty and areas needing improvement.

| Positive Reviews | Negative Reviews |

|---|---|

| Consistently fresh ingredients and bold flavors excite loyal customers. | Long wait times during peak hours frustrate diners. |

| Friendly and attentive staff enhance the dining experience. | Price increases have made some menu items less accessible. |

| Customizable meals cater well to diverse dietary preferences. | Occasional inconsistency in food preparation affects quality. |

Overall, consumers praise Chipotle’s commitment to fresh, customizable meals and strong service. However, wait times and pricing remain common concerns that could impact repeat visits.

Risk Analysis

Below is a summary table highlighting key risks for Chipotle Mexican Grill, Inc. (CMG):

| Category | Description | Probability | Impact |

|---|---|---|---|

| Leverage Risk | Debt-to-assets ratio exceeds 100%, signaling high leverage. | High | High |

| Valuation Risk | Elevated P/E (32.2) and P/B (17.5) ratios imply overvaluation. | Moderate | Moderate |

| Liquidity Risk | Current ratio at 1.23 is borderline for short-term coverage. | Moderate | Moderate |

| Market Volatility | Beta near 1 indicates sensitivity to market swings. | Moderate | Moderate |

| Dividend Risk | No dividend yield, limiting income for investors. | Low | Low |

Leverage stands out as the most concerning risk. Chipotle’s debt-to-assets ratio above 100% signals aggressive borrowing, raising solvency concerns despite solid interest coverage. Elevated valuation multiples pose additional caution amid market volatility.

Should You Buy Chipotle Mexican Grill, Inc.?

Chipotle appears to be a profitable company with growing operational efficiency and a durable competitive moat, supported by strong ROIC versus WACC. Despite a challenging leverage profile, its overall B rating suggests a very favorable but cautious investment profile.

Strength & Efficiency Pillars

Chipotle Mexican Grill, Inc. exhibits robust profitability with a net margin of 12.88% and an impressive return on equity of 54.26%. Its return on invested capital (18.93%) significantly exceeds the weighted average cost of capital (7.64%), confirming the company as a clear value creator. Financial health remains solid, supported by a strong Altman Z-Score of 7.41, indicating low bankruptcy risk, and an average Piotroski Score of 6, reflecting moderate financial strength. These metrics underscore efficient capital allocation and sustainable competitive advantage.

Weaknesses and Drawbacks

Despite operational strengths, Chipotle faces valuation challenges. The price-to-earnings ratio stands at 32.22, signaling a premium valuation that may pressure returns. The price-to-book ratio is notably high at 17.48, raising concerns about potential overvaluation. Leverage is a significant red flag, with a debt-to-equity ratio of 3.48 and debt to assets exceeding 100%, elevating financial risk. Additionally, the absence of dividends may deter income-focused investors. These factors introduce caution amid the company’s growth narrative.

Our Verdict about Chipotle Mexican Grill, Inc.

The company’s long-term fundamentals appear favorable, driven by strong profitability and value creation. Despite a bearish overall stock trend with a -29.22% decline, recent periods show strong buyer dominance (72.3%), suggesting potential recovery. This profile may appear attractive for long-term exposure, but investors could consider a cautious stance given current elevated leverage and premium valuation.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- Chipotle stock sinks after company reports Q4 same-store sales drop 2.5%, forecasts no sales growth in 2026 – Yahoo Finance (Feb 04, 2026)

- Chipotle is defended by analysts after lackluster guidance (CMG:NYSE) – Seeking Alpha (Feb 04, 2026)

- Chipotle Shares Volatile After Q4 Results, Price Target Cuts – Benzinga (Feb 04, 2026)

- Chipotle Mexican Grill, Inc. (CMG): A Bull Case Theory – Yahoo Finance UK (Feb 05, 2026)

- CHIPOTLE ANNOUNCES FOURTH QUARTER AND FULL YEAR 2025 RESULTS – PR Newswire (Feb 03, 2026)

For more information about Chipotle Mexican Grill, Inc., please visit the official website: chipotle.com