Home > Analyses > Healthcare > AstraZeneca PLC

AstraZeneca transforms lives by pioneering medicines that tackle cancer, cardiovascular, and rare diseases worldwide. Its flagship drugs, like Tagrisso and Imfinzi, set industry standards for innovation and efficacy. The company’s global reach and cutting-edge collaborations fuel its reputation as a biopharmaceutical powerhouse. As 2026 unfolds, investors must ask: do AstraZeneca’s strong fundamentals still support its lofty valuation and future growth prospects?

Table of contents

Business Model & Company Overview

AstraZeneca PLC, founded in 1992 and headquartered in Cambridge, UK, stands as a global leader in the pharmaceutical industry. It operates a robust ecosystem centered on discovering, developing, and commercializing prescription medicines across cardiovascular, oncology, metabolism, and rare diseases. This integrated approach fuels its status as one of the most influential drug manufacturers worldwide.

The company’s revenue engine drives value through a balanced portfolio of innovative drugs and vaccines, supported by strategic collaborations and AI-driven research. AstraZeneca serves physicians globally across the Americas, Europe, Asia, and beyond. Its expansive geographic footprint and focus on specialty and primary care solidify a durable competitive advantage shaping the future of medicine.

Financial Performance & Fundamental Metrics

I analyze AstraZeneca PLC’s income statement, key financial ratios, and dividend payout policy to reveal its core strengths and potential risks.

Income Statement

This table summarizes AstraZeneca PLC’s key income statement figures for fiscal years 2021 through 2025, showing revenue trends and profitability metrics.

| 2021 | 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|---|

| Revenue | 37.4B | 44.4B | 45.8B | 54.1B | 58.7B |

| Cost of Revenue | 12.4B | 12.4B | 8.3B | 10.2B | 10.6B |

| Operating Expenses | 23.9B | 28.2B | 29.4B | 33.9B | 34.4B |

| Gross Profit | 25.0B | 32.0B | 37.5B | 43.9B | 48.1B |

| EBITDA | 5.1B | 9.1B | 13.4B | 15.4B | 19.8B |

| EBIT | 1.0B | 3.8B | 8.5B | 10.4B | 14.1B |

| Interest Expense | 1.3B | 1.3B | 1.6B | 1.7B | 1.7B |

| Net Income | 112M | 3.3B | 6.0B | 7.0B | 10.3B |

| EPS | 0.04 | 1.06 | 1.91 | 1.14 | 3.30 |

| Filing Date | 2021-12-31 | 2022-12-31 | 2023-12-31 | 2025-02-18 | 2026-02-24 |

Income Statement Evolution

AstraZeneca’s revenue rose steadily from $37.4B in 2021 to $58.7B in 2025, reflecting a 57% increase. Net income surged dramatically, from $112M to $10.3B, driven by expanding margins. Gross margin improved to 81.9%, while net margin climbed to 17.5%, signaling efficient cost control and robust profitability over the period.

Is the Income Statement Favorable?

In 2025, AstraZeneca posted $58.7B revenue and $10.3B net income, yielding an 81.9% gross margin and a 24% EBIT margin. Interest expenses remained manageable at 2.88% of revenue. Net margin growth of 34% and EPS growth of 189% year-over-year confirm strong earnings momentum. Overall, the income statement fundamentals appear favorable and consistent with solid operational execution.

Financial Ratios

The table below summarizes key financial ratios for AstraZeneca PLC over recent years, providing an overview of profitability, valuation, liquidity, leverage, efficiency, and dividend metrics:

| Ratios | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Net Margin | 0.3% | 7.4% | 13.0% | 13.0% | 17.5% |

| ROE | 0.3% | 8.9% | 15.2% | 17.2% | 21.1% |

| ROIC | -0.5% | 5.0% | 9.3% | 10.3% | 13.0% |

| P/E | 2933.5 | 128.3 | 70.5 | 57.3 | 53.1 |

| P/B | 8.4 | 11.4 | 10.7 | 9.9 | 11.2 |

| Current Ratio | 1.16 | 0.86 | 0.82 | 0.93 | 0.94 |

| Quick Ratio | 0.76 | 0.68 | 0.64 | 0.74 | 0.72 |

| D/E | 0.78 | 0.79 | 0.73 | 0.74 | 0.61 |

| Debt-to-Assets | 29.1% | 30.2% | 28.3% | 28.9% | 26.0% |

| Interest Coverage | 0.8x | 2.8x | 5.2x | 5.9x | 8.1x |

| Asset Turnover | 0.36 | 0.46 | 0.45 | 0.52 | 0.51 |

| Fixed Asset Turnover | 3.68 | 4.69 | 4.36 | 4.64 | 4.00 |

| Dividend Yield | 1.17% | 1.03% | 1.07% | 1.15% | 0.93% |

Evolution of Financial Ratios

Return on Equity (ROE) improved steadily from near zero in 2021 to 21.1% in 2025, signaling stronger profitability. The Current Ratio declined from 1.16 to 0.94, reflecting decreased short-term liquidity. Debt-to-Equity Ratio eased from 0.78 to 0.61, indicating modest deleveraging and more balanced capital structure over the period.

Are the Financial Ratios Fovorable?

Profitability ratios like ROE (21.1%) and net margin (17.5%) are favorable, supported by a strong ROIC of 13.0% exceeding WACC at 4.5%. Liquidity ratios remain unfavorable with current and quick ratios below 1. Debt ratios are neutral to favorable, with debt-to-assets at 26.0% and interest coverage robust at 8.3x. Valuation multiples (P/E 53.1, P/B 11.2) and dividend yield (0.93%) appear unfavorable. Overall, ratios are slightly favorable.

Shareholder Return Policy

AstraZeneca maintains a dividend payout ratio near 50%, with dividend per share steadily rising to $1.64 in 2025. Its modest 0.93% yield combined with share buybacks indicates balanced capital return, supported by free cash flow coverage above 80%.

This policy reflects a prudent approach, avoiding excessive distributions or repurchases. Given consistent profitability and cash flow, the current strategy appears sustainable and aligned with long-term shareholder value creation.

Score analysis

Here is a radar chart summarizing AstraZeneca PLC’s key financial scores across valuation, profitability, and leverage metrics:

AstraZeneca shows strong profitability with very favorable ROE and ROA scores of 5 each. The discounted cash flow score is favorable at 4. However, leverage and valuation scores lag significantly, with debt-to-equity at 2 and both P/E and P/B scoring very unfavorable at 1.

Analysis of the company’s bankruptcy risk

The Altman Z-Score places AstraZeneca well within the safe zone, indicating a very low risk of bankruptcy and strong financial stability:

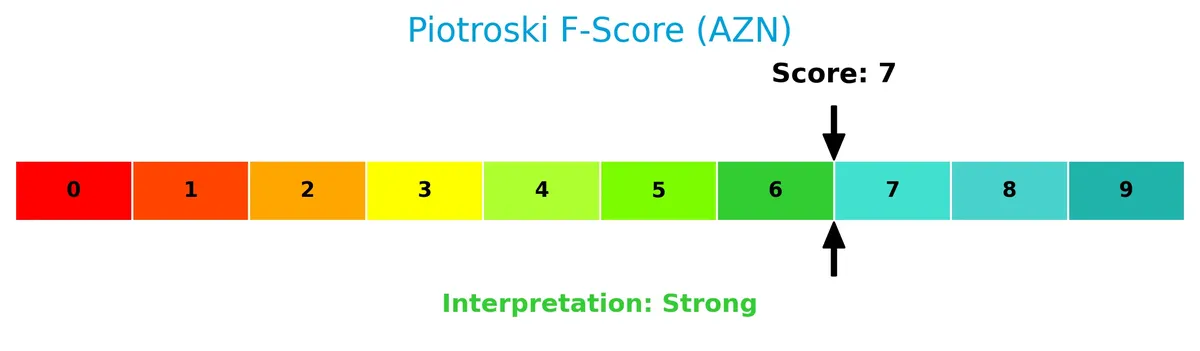

Is the company in good financial health?

The Piotroski Score chart below illustrates AstraZeneca’s strong financial health status based on nine key accounting criteria:

With a Piotroski Score of 7 categorized as strong, the company demonstrates solid profitability, efficiency, and leverage metrics, supporting its position as financially healthy.

Competitive Landscape & Sector Positioning

This section analyzes AstraZeneca PLC’s strategic position, revenue segmentation, key products, and main competitors. I will assess whether AstraZeneca holds a competitive advantage in the pharmaceutical industry.

Strategic Positioning

AstraZeneca concentrates heavily on oncology (23.7B in 2025) and rare diseases (9.1B), complemented by cardiovascular, renal, and metabolic products (12.8B). Geographically, it maintains a balanced global presence, with significant revenue from the Americas (27.6B) and Europe ex-UK (13.5B), showing diversified regional exposure.

Revenue by Segment

The pie chart illustrates AstraZeneca PLC’s revenue breakdown by product segment for the fiscal year 2025, highlighting key contributors to the firm’s top line.

In 2025, Oncology dominates AstraZeneca’s revenue with $23.7B, driven strongly by Tagrisso ($7.3B) and Imfinzi ($6.1B). Rare Disease also stands out at $9.1B, underscoring its strategic importance. CVRM remains substantial at $12.8B, fueling diversification. Notably, newer products like Enhertu ($1.8B) and Calquence ($3.5B) show robust growth, signaling successful innovation. The mix reflects a concentration in Oncology and Rare Diseases, which investors should monitor for risk exposure.

Key Products & Brands

The table below lists AstraZeneca’s key products and brands along with their descriptions:

| Product | Description |

|---|---|

| Tagrisso | Prescription medicine for oncology treatment, generating $7.25B in 2025 revenue. |

| Imfinzi | Oncology drug with $6.06B revenue in 2025, part of AstraZeneca’s cancer portfolio. |

| Lynparza | Oncology therapy with $3.28B revenue in 2025, focused on targeted cancer treatment. |

| Calquence | Oncology treatment product, delivering $3.52B in 2025 sales. |

| Farxiga | Cardiovascular, renal, and metabolism drug, with $8.4B revenue in 2025. |

| Fasenra | Respiratory and immunology medicine generating $1.98B in 2025 revenue. |

| Breztri | Respiratory product with $1.2B revenue in 2025. |

| Brilinta | Cardiovascular drug, $823M revenue in 2025. |

| Ultomiris | Rare disease treatment with $4.72B revenue in 2025. |

| Soliris | Rare disease medication generating $1.84B in 2025 revenue. |

| Zoladex | Oncology and other indications, $1.11B revenue in 2025. |

| Symbicort | Respiratory medicine with $2.89B revenue in 2025. |

| Synagis | Rare disease and respiratory product, $292M revenue in 2025. |

| Saphnelo | Rare disease drug with $686M revenue in 2025. |

| Koselugo | Rare disease treatment, $662M revenue in 2025. |

| Lokelma | Cardiovascular product with $698M revenue in 2025. |

| Enhertu | Oncology medicine generating $1.8B revenue in 2025. |

| Other Medicines | Various other prescription drugs totaling $972M in revenue in 2025. |

AstraZeneca’s portfolio spans oncology, cardiovascular, respiratory, renal, metabolism, and rare diseases. Oncology and cardiovascular products dominate revenue, reflecting the company’s strategic focus in specialty care.

Main Competitors

There are 10 competitors in total, with the table below listing the top 10 leaders by market capitalization:

| Competitor | Market Cap. |

|---|---|

| Eli Lilly and Company | 970B |

| Johnson & Johnson | 500B |

| AbbVie Inc. | 405B |

| AstraZeneca PLC | 285B |

| Merck & Co., Inc. | 268B |

| Amgen Inc. | 176B |

| Gilead Sciences, Inc. | 151B |

| Pfizer Inc. | 143B |

| Bristol-Myers Squibb Company | 109B |

| Biogen Inc. | 26B |

AstraZeneca ranks 4th among these top competitors. Its market cap is about 65% of the leader, Eli Lilly. The company stands above both the average market cap of the top 10 (303B) and the sector median (222B). It maintains a significant 36% gap from its closest rival above, AbbVie, highlighting a distinct scale advantage in this competitive landscape.

Comparisons with competitors

Check out how we compare the company to its competitors:

Does AstraZeneca have a competitive advantage?

AstraZeneca exhibits a very favorable competitive advantage, consistently generating returns on invested capital well above its cost of capital. Its strong ROIC growth signals efficient capital allocation and sustainable value creation.

Looking ahead, AstraZeneca’s pipeline includes collaborations in AI-driven drug discovery and oncology, supporting expansion in specialty care and rare diseases. These efforts open new market opportunities across multiple geographies.

SWOT Analysis

This analysis highlights AstraZeneca PLC’s core strategic factors to guide investment decisions.

Strengths

- strong global brand

- robust 81.9% gross margin

- growing ROIC at 13.03%

- diversified product portfolio

- solid net margin of 17.46%

Weaknesses

- high P/E of 53.05 signals overvaluation

- low current ratio at 0.94 risks liquidity

- high price-to-book ratio at 11.18

- dividend yield below 1%

- moderate debt-to-equity ratio

Opportunities

- expansion in emerging markets

- AI-driven drug discovery partnerships

- growth in oncology and rare diseases

- increased revenue growth at 8.63%

- rising demand for specialty medicines

Threats

- regulatory hurdles and patent expirations

- pricing pressures in healthcare sector

- competitive biotech innovation

- global economic uncertainties impacting R&D funding

AstraZeneca’s strengths in profitability and innovation create a solid moat. However, valuation and liquidity risks demand caution. The company must leverage growth opportunities while navigating regulatory and competitive threats to sustain its market position.

Stock Price Action Analysis

The weekly stock chart of AstraZeneca PLC (AZN) highlights significant price movement over the last 12 months:

Trend Analysis

Over the past 12 months, AZN’s price rose by 53.12%, indicating a strong bullish trend. The stock shows acceleration, with high volatility reflected by an 18.24 standard deviation. It reached a peak of 205.55 and a low of 127.74, underscoring wide price swings during this period.

Volume Analysis

Trading volume is increasing, driven predominantly by buyers who represent 74.84% of total volume. In the recent three months, buyer dominance strengthened to 75.1%, signaling robust investor interest and positive market participation around AZN shares.

Target Prices

Analysts set a clear target consensus for AstraZeneca PLC.

| Target Low | Target High | Consensus |

|---|---|---|

| 103 | 108 | 105.5 |

The target prices indicate moderate upside potential, reflecting steady confidence in AstraZeneca’s growth prospects.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Analyst & Consumer Opinions

This section examines AstraZeneca PLC’s recent analyst grades alongside consumer feedback to provide balanced insights.

Stock Grades

Here is a summary of recent verified analyst grades for AstraZeneca PLC, highlighting key rating changes and trends:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| UBS | Upgrade | Buy | 2025-02-13 |

| UBS | Upgrade | Neutral | 2024-11-20 |

| Erste Group | Upgrade | Buy | 2024-09-11 |

| TD Cowen | Maintain | Buy | 2024-08-12 |

| Argus Research | Maintain | Buy | 2024-05-30 |

| BMO Capital | Maintain | Outperform | 2024-04-26 |

| Deutsche Bank | Upgrade | Hold | 2024-04-16 |

| BMO Capital | Maintain | Outperform | 2024-02-12 |

| Deutsche Bank | Downgrade | Hold | 2024-02-08 |

| Jefferies | Downgrade | Hold | 2024-01-03 |

The overall trend shows a gradual shift from Hold and Sell ratings toward Buy and Outperform, indicating growing analyst confidence since early 2024. UBS notably upgraded its rating twice, culminating in a Buy in early 2025.

Consumer Opinions

AstraZeneca’s consumer sentiment reveals a mix of respect for innovation and concerns about accessibility.

| Positive Reviews | Negative Reviews |

|---|---|

| “Effective treatments with noticeable health improvements.” | “High medication costs limit access for many.” |

| “Strong commitment to research and new therapies.” | “Customer service response times can be slow.” |

| “Reliable supply chain ensures medication availability.” | “Side effects reported more frequently than expected.” |

Overall, consumers praise AstraZeneca’s innovation and dependable drug supply. However, cost and customer support remain notable pain points, potentially impacting patient loyalty.

Risk Analysis

The table below summarizes key risks AstraZeneca faces, including likelihood and potential impact:

| Category | Description | Probability | Impact |

|---|---|---|---|

| Valuation Risk | High P/E (53.05) and P/B (11.18) ratios indicate possible overvaluation. | High | High |

| Liquidity Risk | Current ratio (0.94) and quick ratio (0.72) below 1 signal tight short-term liquidity. | Medium | Medium |

| Debt Risk | Moderate debt-to-equity (0.61) and favorable interest coverage (8.32x) reduce default risk. | Low | Medium |

| Regulatory Risk | Drug approval delays or patent expirations could disrupt revenue streams. | Medium | High |

| Market Risk | Low beta (0.19) suggests limited market volatility sensitivity, but global economic shifts remain a risk. | Medium | Medium |

Valuation risks stand out as the most pressing. AstraZeneca trades at premiums well above healthcare sector norms, signaling caution. Liquidity constraints could challenge operations during unforeseen shocks. Despite a strong Altman Z-Score (6.84, safe zone) and Piotroski score (7, strong), regulatory hurdles and patent cliffs remain material threats to growth.

Should You Buy AstraZeneca PLC?

AstraZeneca PLC appears to be a robust value creator with a durable competitive moat, evidenced by a growing ROIC well above WACC. Despite a manageable but notable leverage profile, its overall B+ rating suggests a very favorable financial health profile.

Strength & Efficiency Pillars

AstraZeneca PLC demonstrates solid profitability with a net margin of 17.46%, ROE at 21.07%, and ROIC of 13.03%. Importantly, its ROIC surpasses the WACC of 4.49%, confirming the company as a clear value creator. Operational efficiency is robust, supported by a favorable gross margin of 81.9% and an EBIT margin of 24.0%. These metrics reflect AstraZeneca’s sustainable competitive advantage and effective capital allocation within the pharmaceutical sector.

Weaknesses and Drawbacks

The company’s valuation metrics raise caution, with a high P/E ratio of 53.05 and a P/B ratio of 11.18, signaling an expensive premium relative to industry norms. Liquidity ratios are weak, as the current ratio stands at 0.94 and the quick ratio at 0.72, below the safety threshold of 1.0, posing potential short-term liquidity concerns. While debt-to-equity is moderate at 0.61, investors should watch valuation and liquidity risks carefully amid evolving market conditions.

Our Final Verdict about AstraZeneca PLC

AstraZeneca’s financial health is fundamentally strong, supported by a safe Altman Z-Score of 6.84 and a robust Piotroski score of 7. The bullish long-term trend and strong buyer dominance (75.1%) suggest positive momentum. This profile may appear attractive for long-term exposure, though the premium valuation and liquidity weaknesses counsel cautious position sizing and timing.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- Thornburg Investment Management Inc. Sells 24,703 Shares of AstraZeneca PLC $AZN – MarketBeat (Feb 26, 2026)

- AstraZeneca to complete direct listing of ordinary shares and all US debt securities on the New York Stock Exchange – AstraZeneca (Jan 20, 2026)

- Here’s What Lifted AstraZeneca PLC (AZN) in Q4 – Yahoo Finance (Feb 12, 2026)

- Why AstraZeneca PLC (AZN) is One of the Best Immunotherapy Stocks to Buy According to Hedge Funds – Finviz (Feb 19, 2026)

- REG – AstraZeneca PLC – AstraZeneca prices a $2bn bond offering – TradingView (Feb 26, 2026)

For more information about AstraZeneca PLC, please visit the official website: astrazeneca.com